Discl: Not Held

Seeing some trades go through SM on SPZ, had a quick peek at the chart.

The price looks to be at attractive levels since 30 Sep 2025, when I last contemplated opening a position, where it was at $0.96

- The price is now very much in the 82.5% retracement level zone of $0.825

- If $0.825 does not hold, there should be good support at $0.75 going back to March 2025, failing which $0.655 which goes back to Nov 2024

- Downside from here are now not as severe vs back in Sep 2025 ...

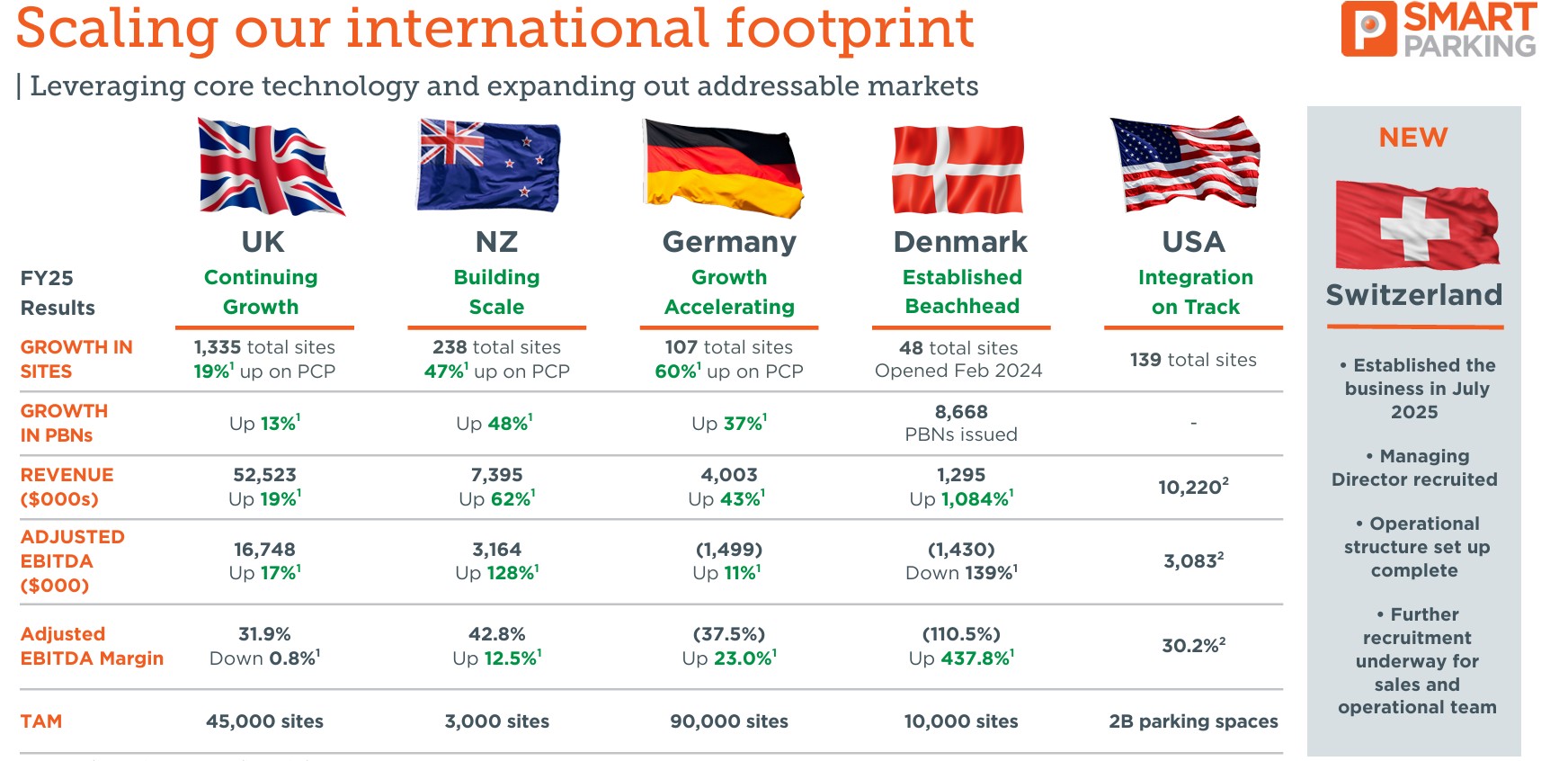

Nice update from SPZ, condinuting to deliver and seems to be integrating the USA acquisition, as well as adding new sites there. UK, Germany and NZ going well. Pivoting in Denmark with regulation changes. Switzerland just started.

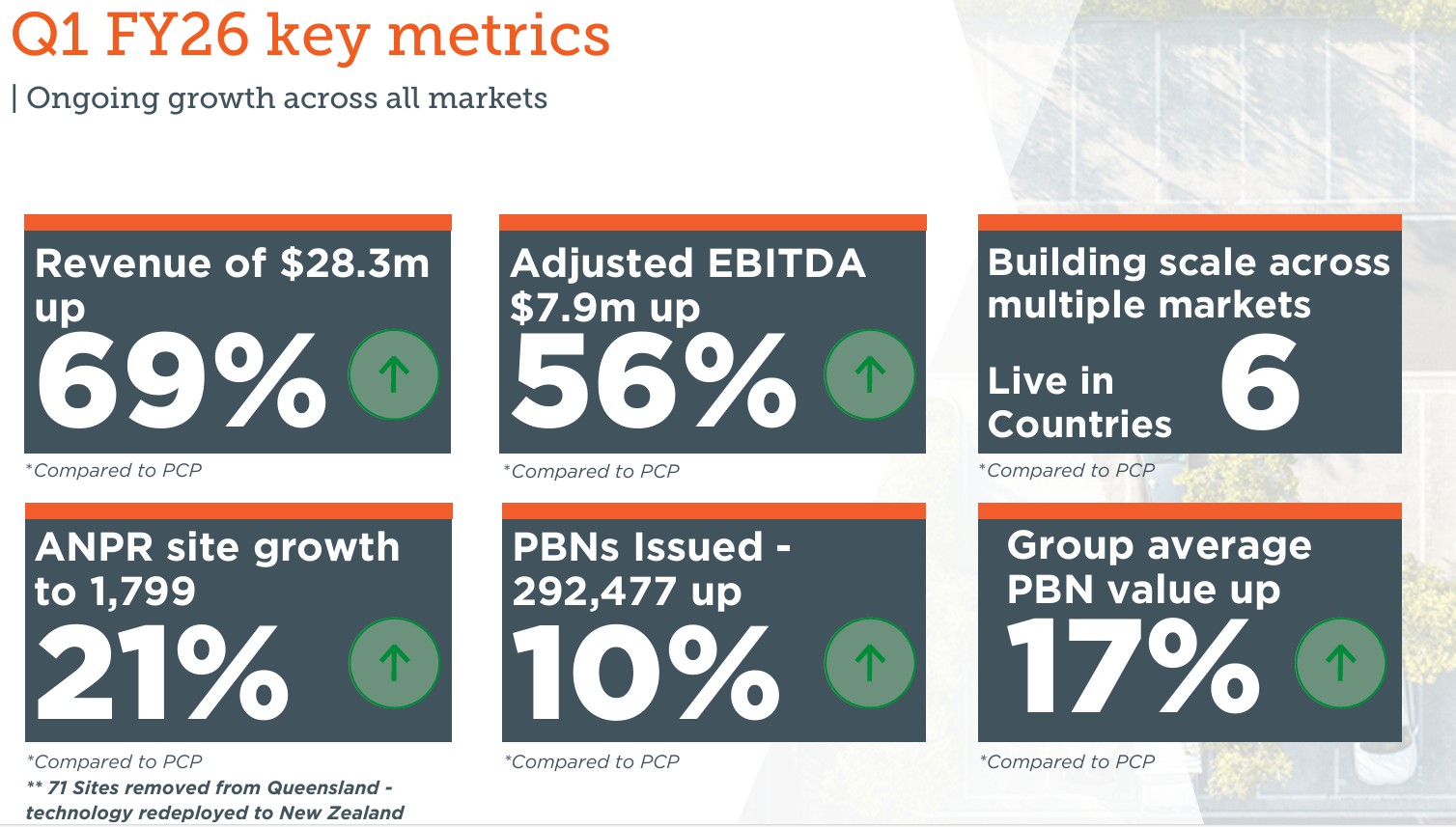

Another great quarter from Smart Parking

200k on market trade - like this as a holder

There’s director buying and then there’s DIRECTOR BUYING!

just shy of a million dollars on market picked up here

This morning $SPZ announced their 1H Results as well as the proposed acquisition of US-based Peak Parking LP for US$36.0m with an associated capital raising via an entitlement offer and a fully underwritten institutional placement.

It would be easy to focus on the acquisition – exciting that it is – however, in this straw I will focus on the operational performance for the half, leaving the proposed acquisition as a separate matter.

1H FY25 Highlights

Financial Highlights

- Revenue of $31.9m up 20.0% to pcp

- Adjusted EBITDA of $9.5m up 26% to PCP and Adjusted EBITDA Margin of 29.8% up 139 bps

- EBITDA of $9.19m up 34.6% to PCP

- "Adjusted free cash flow" (excluding growth capex) of $6.4m up 60% to PCP

- Cash of $8.5m up 17%

- EPS of $1.12 ($1.11 diluted) up 70%

Operational Highlights

Good growth in all markets, with accelerating PBN growth in the UK +18% (vs +13% in pcp) and strong growth in the profit contribution in NZ.

Losses in Germany continue to narrow, and a good start in Denmark.

My Observations

This is a good operating result. $SPZ have delivered another year of +20% revenue growth, with operating leverage driving strong EPS growth of +70%,

The UK continues to be the engine room driving almost 80% of revenue and 88% of adjusted EBITDA.

It is pleasing to see a meaningful contribution coming through from NZ, and it is still early days in Germany and Denmark, although German with sites up to 72 from 43 in the PCP, only added +5 from the EOFY 2024.

On the other hand, Denmark has gone from 11 contracts and no reported operating sites at EOFY24, to now have 21 up and running.

The new growth markets of NZ/Ger/Den are starting to make a more material contribution with aggregate PBNs growing +43% in the half vs. the PCP, compared with the more mature UK growing at a still decent (and in fact accelerating) +18%.

On cash generation, $SPZ’s curious “Free Cash Flow” of $6.4m (defined on slide 32), compares with the FY value of $12.2m – so it seems only a modest increase on a pro rate basis. The historical 1H/2H split for 1H FY24 was 49.3% of cash receipts, so their doesn’t seem to be a strong seasonal effect.

The seemingly impressive operating leverage and strong NPAT growth hides two factors. First, a currency tailwind giving a windfall of $0.74m, offsetting significant expenses growth: raw materials and consumables (+20% - in line with revenue growth), employee benefits expense (+28%), D&A (+35%), rent and leases (+52%) and other expenses (+18%).

In isolation, these cost increases might appear to be a cause for concern. However, it is important to understand that these expense lines include the impact of the expansions into Germany and Denmark, and doubtless too, the costs for a year of prospecting for acquisitions in the US.

Overall, then, the net cash generation of +$1.3m is a good result. Cash contributions from UK and NZ, more than covering the net costs of getting started in Germany and Denmark and the hunt for acquisitions.

My Key Takeaways

The business continues to allocate capital from profitable core operations into expanding the business. All markets are growing – UK and NZ strongly, Denmark is off to the races, and Germany is making slower progress.

CEO Paul Gillespie reiterated the strategic goal of achieving organic growth of doubling the business to 3,000 ANPR sites by December 2028. Achieving that from today’s total of 1561 (including the suspended 71 in QLD), represents a CAGR from end of 1H FY25 to 31 December 2028 of 18%. This can be considered in the context of the latest growth rate of 28% (to pcp) and with the US soon to provide a new beachhead for growth.

Tomorrow, I’ll write up my appraisal of the proposed US acquisition deal. But, operationally, the meter at $SPZ is ticking along nicely.

Disc: Held in RL and SM

18-Nov-2024: Canaccord Genuity: Raising SPZ Target Price to $1.10/share (prev. $0.75/share)

Source: https://canaccordgenuity.bluematrix.com/sellside/EmailDocViewer?encrypt=f277778a-b556-4617-9adc-dcf160310b70&mime=pdf&co=Canaccordgenuity&[email protected]&source=mail

That was page 1 of that CG broker report - click on the link at the top (or copy and paste that plain text link above) to access the full report.

[not held]

As already mentioned, we got a glimpse into Q1 FY25 and not surprisingly Smart Parking continues to kick goals. My thesis is that Smart Parking will be able to increase revenue YoY (like it has done since 2021), with a target of more than 15-20%, while getting an attractive return on capital employed. How? They invest their cash well and their business model is bloody attractive. In terms of a thesis check, things are going well here.

Historical data

I have been monitoring their progress over several years and I figured this was worth sharing. Since 2021, growth has been steady (arguably the best way to grow). I think this business will continue to flourish into the future with the exception of any major hiccups, mainly regulatory ones, along the way. Management's new target (3000 sites) in four years speaks to their confidence also. Should they continue on this current growth trajectory, they should achieve market-beating returns and then some.

What I am looking to see over the next few years is UK sites, as a % of total sites under management, decreasing -- suggesting they are growing in other jurisdictions but also helping to reduce key market risk in the UK.

Another risk worth highlighting relates to the current management team, specifically the CEO/MD and CFO. The current CEO and MD, Paul Gillespie, has been employed since 2013, while the current CFO, Richard Ludbrook, has been there nearly 14 years. Further, the current Chair, Christopher Morris, has been in his position since 2009. Under their direction, more recently in particular, Smart Parking has thrived. That said, there is no guarantee the business performs continues to perform this well under new management. Something to monitor.

Disc. held

$SPZ held their AGM this morning.

A few positive updates, with the two key slides added below:

- 1Q FY25 is off to a good start: revenue up 24% and Adjusted EBITDA up 30%, both to PCP

- The 1500 site YE target has been achieved ahead of plan (1529 at 15 Nov) - note this targt had been accelerated from EOFY25

- A new long term target to achieve 3000 organic sites, doubling the business, by December 2028

CEO Paul noted that it's taken them 10 years to get to 1500 sites, and they now aim to add the next 1500 in 4 years.

Work on new markets in Scandinavia and the US (Texas, Florida) is progressing. Focus is now on finding the right entry point.

Demark is off to the races with contracts being signed.

UK - single industry code of practice agreed, no issues flagged under the Labour Government - regualtory environment appears stable for now. Paul thinks the Government will now monitor and see how the industry functions under the unified code.

Churn remains low at 30-40 site p.a.: mix of site redevelopments, exits initiated by $SPZ, and some losses to competitors.

Conversations under way with the new QLD LNP Government - warm but non-specific noises. Expecting movement in the New Year. Paul said he is confident they will return.

Overall, this is a company that is continuing to deliver, with a management who appear confident across all markets, with a clear focus on both operational delivery and growth.

On Valuation:

Market likes today's update. With SP at time of writing at $0.82, getting towards the upper end of my valuation. So, at 3.8% in RL, I'm a hold here. Need to update valuation in the light of the 3000-Dec. 2028 growth target.

Disc: Held in Rl and SM

Smart Parking yesterday held their AGM and gave a comprehensive trading update (they're also meeting with us on Monday). There was a lot to like. It's a seasonal business and Q1 is usually a good quarter but comps to pcp are relevant and these all looked good. Fines were up 26% versus pcp and up 15% in the mature/not-really-mature UK business. Record revenue. Looks to be gaining operating leverage, although admittedly that is relying on an unaudited adjusted EBITDA number.

Site growth wasn't as rapid as previous quarters but look to have reaccelerated over the past 5-6 weeks to stand at 1193 sites. Even using the quarter end number site growth was 29% higher than pcp and 16% higher in the UK. They brought forward their 1500 site target by 6 months to 31 December 2024 and in so doing continued their happy habit of beating what initially look like aspirational site targets. Importantly the site target is based on organic growth only and so is likely now a conservative target.

When I've spoken to them in the past they think at 1500 sites they're a $70-75 million revenue company, generating $22-25 million EBITDA. That seems about right at the topline, although I'm not modelling quite so much to fall to EBITDA and hoping to get a pleasant surprise. But 1500 sites is just the start. When you consider there are 140,000 sites just in the territories they operate in, you start to get an idea of how long the runway is.

They spoke at length about wanting to move into new territories. I like the way they go about this. They prepare the ground by mentioning it to shareholders without a lot of detail. Six to 12 months later they're getting more specific about where they're focus is (Europe and the US). They talk about not biting off more than they can chew and just moving into one territory at a time. They talk about learning from the Queensland sojourn and focusing on territories that not only allow third party access to licensing information, but also have a code of practice or similar legislation in place. All good things in my view.

The negatives? They're all regulatory. It doesn't sound like there has been much movement on the Queensland side of things. That's not all that surprising given how negatively the government came out against the industry. Their best bet may be a change of government next year, which the polls suggest is likely. In the UK the government is considering submissions to its proposed new legislation and is not expected to give its verdict for at least six months. On the plus side that means a longer period of status quo, but on the downside the dark clouds loom for longer.

There's a good-ish argument that a microcap that has been a microcap for many years will always stay a microcap. I've said similar things in the past, particularly when you have the same people in charge. There's also an argument that change doesn't happen overnight and takes longer and will be harder than you first envisage. Smart Parking is evidence for the latter argument. Current CEO Paul Gillespie took the reigns in FY13 when revenue was $20.6 million. In FY21 revenue was...$20.6 million*. Roll forward two years to FY23 and revenue was $45.2 million and the momentum appears to be continuing. It's not vain growth either - they're increasingly profitable and cash generating. Sometimes it just takes time to get things humming.

[Held]

*admittedly COVID impacted but let's not the truth get in the way of a good story

Another excellent year for Smart Parking with all key metrics moving in the direction we want to see. Revenue came in slightly ahead of my forecast, but perhaps most impressively net income was double what I forecasted, primarily due to gross margin increasing.

Highlights

- Revenue of 45.1m, an increase of 21%, above my forecast of 43m

- Cash inflow of 9.2m, just below my forecast of 10.5m

- Adjusted EBITDA 11.5m, up 35%

- Adjusted EBITDA margin, up 25.5%

- Net income of 6.7m, around double my forecast of 3.3m

- Sites under management (the estate) grew 33% from 839 to 1112. This is a CAGR of 31% since 2018.

- More than 800k spent on share buybacks during the year – 3m shares – at an average price of 0.22c.

- Cash of 10.7m – bloody impressive considering a recent acquisition, continued investment in Germany and share buy backs throughout the year.

- New Zealand deserves a special mention – sites increased to 84 (320% pcp) growth in breach notices increased 258%, with revenue just under 3m – noting all are off a low base this is really impressive for what is still a reasonably new market.

- Qld market remains in a holding state pending a review around regulation.

- 1.3m debt – manageable and not a concern.

Re: their expansion into Germany – this remains in capex/investment stage. In the call management indicated they are starting to invest more aggressively in this market due to the opportunities/pipeline and large area they can cover. Will be interesting what lies ahead for Germany in FY24; this has the potential to be a hugely profitable market for Smart Parking.

To elaborate on the increase in gross margin, this is the result of new sites following the initial period of investment – a great example of operating leverage, demonstrating just how attractive this business model is when operating under a regulative-friendly framework.

Outlook

- Unless I misheard, re: new sites under management from the recent German acquisition – they are hoping to convert 2/3 of these to ANPR technology.

- Some interesting discussion around regulation in the UK on the call, specifically the establishment of a code of practice which remains ongoing. They don't expect any decision in FY24. This is by far and away SPZ's key market, and any regulation changes will have a significant impact (positive or negative) on the business. Management did emphasise that this is very different to Qld – UK is more concerned with establishing a code of practice to govern those that already exist; they are far more open to parking regulation and the requirement/reason for operators to function (unlike Qld which removed the ability of parking operators to access data altogether). Both NZ and Germany for instance already have established a code of practice, but this remains one to watch closely and is a key risk for the business. @Noddy74 @Wini @Byrnesty and others -- anything else to add that I missed or any disagreements?

- They will continue to focus on growth in core markets moving into FY24 – UK, Germany and NZ – both through organic growth and attractive acquisition opportunities.

- During the call management mentioned they are looking to enter new markets in FY24 (most likely in northern Europe) – but have lots of work to do and still in the research stage. They note they need to find the right leader, people and market and need to get that right – refreshing to hear but they need to be cautious not to overdo it, particularly with lots of work to do in Germany and plenty of growth ahead of them still in NZ, the UK and to a lesser extent Australia. This is another risk; we don’t want them biting off more than they can chew, particularly with the business currently performing so well.

I will update my valuation in the coming days – @Byrnesty with operating leverage starting to come through and net income coming in much higher than I expected, I am guessing my DCF will reflect an increased company value. I still think a large discount is required until we know more about the regulation risks in the UK.

Just got back from a Mauritian beach yesterday and catching up on a few updates and the like. Smart Parking delivered not the worst update of the pack. For these guys it's all about sites under management - what they call "the estate". Sites are up 13% on the previous quarter to 1043 (up 24% YoY) and they remain on track for their 1500 site target by the end of FY25. I imagine we'll see a new target in the next 12 months for FY27 or FY28.

Currency is a headwind given they make most of their money in the UK, but their cost base is largely overseas too so forms a natural hedge. They present an Adjusted EBITDA number, which excludes Germany's setup costs. I imagine this irits some people but they are transparent about the amount they're excluding and it is useful to know what the German investment is so I'm ok with it on balance. For what it's worth Adjusted EBITDA is $8.5m Q3 YTD ($8.9m in constant currency). This excludes $1.2m of Germany's costs. EBITDA grew slower in Q3 but it's traditionally a quieter period, with the current quarter being the bigger maker of bank.

On a regional front the UK is still the engine room and despite being the most mature region it is still growing at a decent clip organically. APAC (really just NZ) appears to continue to be growing rapidly (and profitably) despite the loss of new sales in Queensland. Germany is growing quickly off a low base but not at the speed they had hoped, resulting in some sales team remediation. It's a slightly mixed message as they have also suggested the rampup has been similar to New Zealand at the same stage. Germany remains on watch with the sales intervention hopefully gaining traction in Q4.

Cash on hand is down a little but Q3 is the quietest quarter and it's difficult to make conclusions without knowing how working capital and debt have moved. Overall the thesis remains intact and a key question will be what they do with what I expect will be a growing cash pile. Any dividends they pay would be unfranked so more aggressive buybacks and/or M&A appear to be the more likely options. Not a bad problem to have.

[Held]

Overall it was a solid update from Smart Parking last week with strong topline growth and decent cash generation being partly offset by unfavourable FX movements and increased overheads.

The key driver of the results is, as always, sites under management and on this measure they continue to deliver. The Group held 984 sites at the reporting date, which was up from 839 sites six months prior. They were keen to highlight that they've since exceeded 1000 sites, although you could argue QLD sites should be backed out of that number. Although the 1000 site target has been replaced by a 1500 site by June 2025 target, longer term holders will remember that 1000 sites by June 2023 was an earlier target and it deserves mention that they have beaten this. On the earnings call they reaffirmed the 1500 site target and I asked them to clarify if that meant ex-QLD, which they confirmed was the case.

Revenue was up 18% vs pcp, but up 25% from a constant currency perspective. UK growth is impressive given its relative maturity but the real driver is APAC, half of which we now know is - at best - on pause. Germany doesn't yet make a material contribution and will be on watch going forwards to ensure it does do so.

At the same time operating expenses appear to have jumped significantly and permanently. They strike me as a little sensitive about the investment in Germany relative to the return they're getting and I'm not fully on board with their practice of backing out Germany's costs from Adjusted EBITDA. However, it's all fairly transparent so you can rework it as you see fit. Overall a reasonable level of explanation was given to the cost uplift but going forwards I'd like to see that increasing at a lower rate. I have asked for clarification about what the disclosed monthly exit opex rate of $1.7m includes as it's not entirely clear, but that equates to a six month number of $10.2m - not too much higher than the disclosed half yearly opex cost, suggesting that opex growth may have slowed.

Free cash flow was strong but again it should be noted they are excluding Germany's costs from their definition of this. It's all very transparent though so choose your own adventure on what you do there. It also doesn't include Growth Capex (almost all of their capex isn't ongoing). I'm ok with that, others won't be. The balance sheet continues to look good and they have flagged a continuation of their share buyback (which they announced to the market they had started acting on a few days later). They've also started talking about dividends. I assume they will be unfranked given their overseas operations so I don't much see the point of that unless they've completely run out of ideas, but it is another indication that they do seem to act in alignment with shareholders.

Kudos for them holding an investor briefing. One of the themes I felt this reporting season has delivered is somewhat less of those and credit goes out to management who front up when the news isn't necessarily all good. Based on the attendees they do seem to be getting a little more insto coverage, although some of the questions seem to suggest the analysts hadn't had alot of exposure to the business yet.

In summary

The good:

- Site growth is the key driver and is tracking nicely. I haven't even mentioned the Technology segment of the business here as it's become an increasingly immaterial part of the business.

- As expected Revenue growth is following sites under management. Previously the CFO has said they could deliver $70-75m at the topline with 1500 sites. My model also supports this, albeit at the bottom end of that range. At that kind of number and given their propensity to gush cash, they'll be hard for the market to miss.

The not so good:

- Germany isn't yet shooting the lights out but it's early days. @Wini highlighted an Aldi win they'd had in this market some time back and they disclosed they now manage two Aldi stores, in deals signed off at the northern Germany region head office. According to Wikipedia Aldi Nord is the bigger of the two Aldi regions and has 2298 stores.

- I think the market was a bit disappointed to see the Cost base jump as it did. It's fair to say I was a bit too and this is on watch going forwards.

The ugly

- I think the prudent thing to assume is Queensland is not coming back and be pleasantly surprised if it does. I asked management on the investor call what learnings they took from this and someone asked something similar on the Strawman call. Both times they highlighted the lack of a Code of Practice in Queensland that does exist in other markets they operate in and that this would prevent a recurrence. I think the fact they were blindsided like they were suggests they and the peak body didn't do nearly enough work with the government to advocate/educate/put a code in place etc. and being proactive should be a key learning.

Overall I'm still happy to hold. I took a little profit at higher levels but it's still a larger holding and I think closer to a buy than a sell given it's pulled back a bit and should be supported by the share buyback if that continues.

Smart Parking released a presentation this morning prior to going on Coffee Microcaps. I don't think Mark has posted the videos yet but when he does it will be worth a watch as it includes a roll call of Strawman member favourites, including Alcidion (ALC), Spectur (SP3), Symbio (SYM) and AVA Risk (AVA). Anyway, the SPZ presentation included site and financial updates.

The good

- They continue to gain sites and were managing 900 as at 30 Sep (vs 839 at 30 Jun)

- Revenue for the quarter of $10.8m, up 21% vs pcp

- Substantial new record of breach notices issued

- APAC growth appears to be strong, at least in terms of breach notices, with PBNs in Q1 only slightly less than the first 3 quarters of last year combined

Not so good

- Cash is not so good. Cash is down from $11.4m at year end to $9.3m at 30 Sep. In part this can be explained by $1.8m of capex and $0.4m of share buy backs, but they also reported $2.7m of 'adjusted' EBITDA - where's that? Hopefully just some temporary working capital movements that will resolve by 30 Dec.

- Technology segment didn't really get a look in but the combined revenue numbers suggest it didn't contribute much to the total

- Also, despite the growth in revenue, the PBN number growth suggests they're not recovering as much per breach. FX will be playing a role here.

On Watch

- Definitely cash. I'd want to see a decent turn around in Q2.

- The UK macro and FX

On balance I think the message is still the same; they're delivering profitable growth. I expect them to be able to scale pretty efficiently too, with top line growth falling pretty efficiently to the bottom line. That last bit isn't as apparent yet as I might of originally hoped but I think you can give them a bit of a leave pass considering how early they are rolling out in Germany, QLD and NZ and the investment that will require.

[Held]

Snap @Rocket6 you just beat me to it

***

Busy day...start of a busy week...

Smart Parking's result this morning was better than I expected on most measures. Revenue was up 68% on FY21, mainly in the parking services business (i.e. fines) due to a 36% increase in sites under management and considerably higher yield per site. Adjusted EBITDA was $8.8m in FY22, compared to $2.2m in FY21 despite considerable investments and additional headcount for future growth and normalisation of other opex items which benefitted from COVID in the prior year. Adjusted NPAT went from a loss of $1.7m in FY21 to a profit of $2.2m I normally don't like to see an Adjusted NPAT but given the $6.9m one-off VAT win the company had over the HMRC in FY21 I think it does make sense in this case.

The company claims a free cash flow of $8.1m but they do exclude capex from this (but do include lease payments) on the basis that they classify this all of this as growth. Given the nature of their business I think it probably makes sense that they wouldn't incur maintenance capex and I can accept their reasoning (Claude is shaking his fist at the monitor right now) but if you don't just add it back - I think the valuation stacks up even if you do.

Some notes from the call and releases this morning:

- Sites under management (being a key metric) are scaling up nicely and on track for previous target of 1000 by end of FY23 and new target of 1500 by end of FY25

- New markets:

- NZ - 20 sites, EBITDA and cashflow positive. Target of 75 by June 2023. 3000 potential sites.

- QLD - 27 sites. Target of 80 by June 2023. 2000 potential sites.

- Germany - foothold of 4 sites. Target of 70 by June 2023. Dunno how many potential sites, lots - possibly twice that of the UK, which has 45,000 potential sites.

- Share buyback to continue while share price remains depressed

- Overheads grew substantially but management have indicated this was due to some investments for growth (e.g. Germany) and end of furlough schemes etc. and shouldn't grow at the same rate going forwards

- Acquisitions are performing at (NE Parking) or ahead (Enterprise) of targets

- Technology segment was EBITDA positive. This was a bit of a surprise to me. In previous conversations management's commentary wasn't that bullish in relation to that business.

- July and August to date have been record months

- Regulatory overhead of Parking Code of Practice is still on hold and government hasn't provided update (they've understandably been busy giving Boris the arse). Interestingly Paul stated Smart Parking and the majority of the industry would like to see most of the code implemented - just not the bits that cap their fines.

- Are seeking more acquisitions or markets. They are limited to juristictions that allow number plate owner databases to be accessed, which is why QLD is the only state in Australia they have thus far entered.

So overall very positive. I mentioned to someone this morning that there are some things I don't love. In particular I think they could do a better job of presenting the statutory accounts to be somewhat more aligned to the management accounts. I get they serve different purposes but GAAPs aren't completely prescriptive and other companies manage that better than they do.

I also don't love the word Adjusted in front of EBITDA and NPAT but I've always found them pretty transparent about what has been adjusted and you can backwork it if you want to. Those are relatively minor quibbles compared to keeping the business on track and delivering on the promises they've been making, which so far they seem to be doing.

Held here and IRL

Highlights

- Revenue 38.1m, an increase of 68%

- Total sites under management: 839 – an increase of 36%

- Parking breach notices increased by 81%, largely due to increased sites under management and recovery from Covid restrictions.

- Cash holdings 10.8m

- Inflow from operating activities – 10.1m, an increase on last year’s 7m.

- Free cash flow of 8.1m, an increase of 624%

- FY22 was profitable for the business, with NPAT coming in just under 1m. This is a decrease on last year due to a one-off VAT payment, which bolstered FY21 earnings.

I still need to do a more thorough deep dive on this one, but it looks to have been another impressive year for one my highest conviction holdings. Management has done remarkably well in managing the business during a tough period. While many parking operators struggle, Smart Parking is now a stronger, more resilient business than it was 24 months ago.

We are also starting to see some scaling take place. Essentially we have seen revenue increase by around 16m, while other costs (excluding D&A) increased by around 3.5m:

- Materials/consumables: increase of 500k

- Employee expense: increase of 2.7m

- Depreciation/amortisation: increase of 900k

- Rental/lease costs: Increase of 170k

The business doesn’t shy away from increasing overheads either, noting a ‘51% increase’ in their investor presentation. But with a gross margin of 60%> and the business seemingly using its cash well, I worry very little about an increase in costs when revenue is outpacing that increase by more than 4x.

When you consider they are trying to break into new markets in Germany, Australia, and New Zealand, the costs look even more impressive. And pleasingly, they are funding this growth themselves without having to tap shareholders on the shoulder. And for an added bonus, New Zealand is already operating cash flow positive despite only recently entering this market.

In short, this is a capital light business that requires minimal maintenance CapEx to fund operating activities. This is starting to reflect in their financials. My confidence continues to grow as a result. I will update my valuation in the coming weeks.

FY23 outlook

- The business provided an update re: early FY23 activity, with 878 sites as of 22 August.

- They have also set some targets: 80 Australian sites, 75 NZ sites and 70 German sites by June 2023.

- They believe the current market in Germany is very manual/employee orientated. SPZ's tech-led solutions should provide them with a competitive advantage in this market, and result in additional client wins.

- Scope for further accretive acquisitions -- which seems pragmatic given their strong balance sheet and history of sensible acquisitions.

- They expect further profitable growth in the coming FY.

We weren't provided with any revenue or profit figures, but still get some insight into SPZ's H2 period.

- Parking breach notices (PBN) are forecast to increase by around 70% vs PCP. While this figure hasn’t moved much since the H1 increase, it marks a strong year for SPZ. Q3 was the slowest quarter of the year for PBNs issued, while Q4 is forecast to be an improved one (second highest).

- Sites under management was recorded at 816 (as at 31 May), an increase of 32% PCP. A total of 99 sites have been added thus far in H2, noting June figures still need to be added. A breakdown based on region (and churn) is recorded below. While total sites under management (99) wasn’t anywhere near as high as H1 (176), churn in H2 has been much more respectable – 20 in H2 vs 58 in H1.

- 42 sites are now up and running in the APAC region, while the sales team was doubled to ‘capitalise on market opportunity’. If my calculations are correct, total sites under management has effectively doubled in H2 (from 21 to 42). PBNs in the region continues to trend upwards nicely (below).

- As for their push into Germany, four customer contracts were signed, with two locations live and generating revenue. 0.5m OPEX costs for the half suggests they aren’t throwing lots of money down the drain as they try and shift into a new market. This is obviously pleasing in this current environment.

Smart Parking continues to be one of my higher conviction holdings. Pending the release of the FY result (where I will have a proper dig into the financials) SPZ is high on my 'top up' list at the moment. They continue to grow at impressive levels, they are profitable (based on H1 reporting) and have a solid balance sheet -- the latter provides them with stability and an ability to fund their growth strategy inhouse. They aren't impacted by supply shortages and are in a good position to make strategic acquisitions when the opportunity arises. Provided the FY report reflects more of the same, management continue to demonstrate that they are solid capital managers.

@Noddy74, any differing thoughts?

UK retail foot traffic is a metric I keep a close eye as an owner of Smart Parking and since 'Freedom Day' UK shoppers have shown a propensity to want to get back to the shops. Foot traffic has comfortably sat at 80+% of 2019 levels since Aug/Sep, with the most recent survey recording 83%.

Having said that I am wary of the risk any further COVID lockdowns would have on this company, notwithstanding the reluctance the government would have on imposing them. I do note cases remain high at 40-50k cases a day.

However, crucially severe symptoms and deaths remain nowhere near the levels of previous outbreaks giving me confidence the risk of further lockdowns remain muted, Omicron impacts aside.

In their most recent update management provided a 1H outlook, which although buoyant appeared to indicate not just a quieter 2Q at the top line (expected due to seasonality) but also a lower EBITDA conversion percentage. I wrote to the CFO to ask him about this and to his credit I got an answer back within a couple of hours that it reflected lower contribution from breach notices, which is a higher margin revenue source. Q1 and Q4 are historically strong in terms of seasonality.

[Held]

Credit goes to Rocket6 for posting about this one. After looking into it I took a position in RL and SM some months back and looking at today's update am glad I did. I think the market is underestimating how much that top line can grow as they get back to the sort of revenue/site they were doing pre-pandemic. On top of which they are rapidly expanding the number of sites under management with a target of 1000 by Jun-23, which they are tracking well to achieve.

I always try to find something to criticise but there's a hell of a lot to like. They seem to be responsible capital managers as evidenced by the price they paid for their recent acquisition (EV/EBITDA multiple of 1.0 to 1.3x) plus the way they're converting top line growth to bottom line growth. They seem quite transparent as evidenced by their disclosure of churn (sites lost) and the fact they're disclosing similar metrics now to what they were 12 months ago when things weren't looking nearly as rosy. Plus to my eye the valuation looks really approachable considering the speed of their growth and the fact they're profitable and churning out cash.

I would have no hesitation in recommending others to have a look.

SPZ - pre-release comms on new Tessera app / platform

2021-03-23

SPZ have circulated an early heads up of their new platform named Tessera, aimed at not just streamlining the back end processes of Car Park management for local Councils, but also the new platform lays the foundations to be expanded into other services offerred by the municipality

The overview video is here

It does seem like a sensible idea to leverage the already in place relationships with respects to Car Parking and simulate those efficiences and processes over into the other services of the already customer base.