Consensus community valuation

Discl: Not Held

Seeing some trades go through SM on SPZ, had a quick peek at the chart.

The price looks to be at attractive levels since 30 Sep 2025, when I last contemplated opening a position, where it was at $0.96

- The price is now very much in the 82.5% retracement level zone of $0.825

- If $0.825 does not hold, there should be good support at $0.75 going back to March 2025, failing which $0.655 which goes back to Nov 2024

- Downside from here are now not as severe vs back in Sep 2025 ...

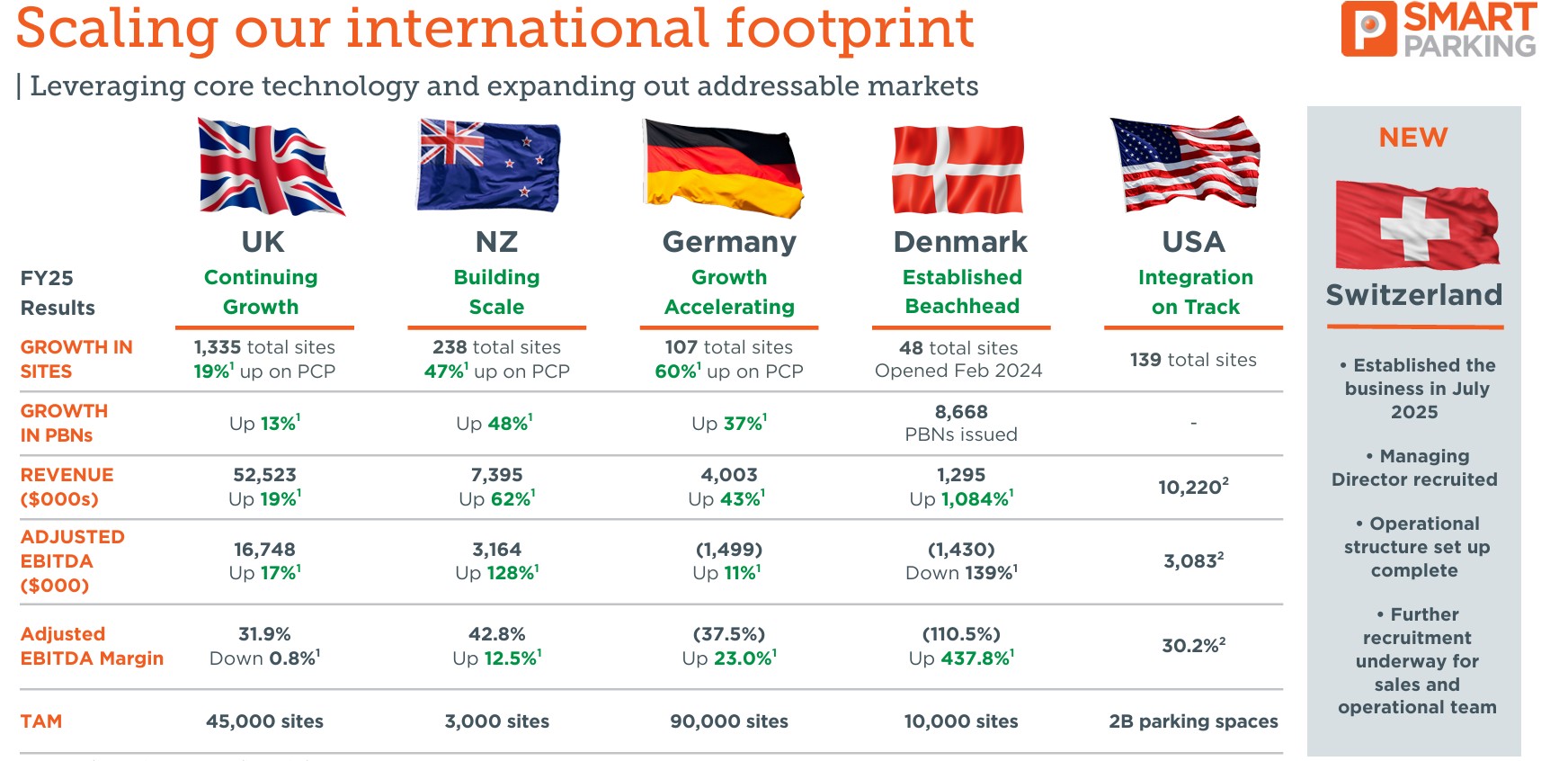

Nice update from SPZ, condinuting to deliver and seems to be integrating the USA acquisition, as well as adding new sites there. UK, Germany and NZ going well. Pivoting in Denmark with regulation changes. Switzerland just started.

Another LinkedIn post announcing Smart Parking have opened for business in Switzerland.

I don’t recall hearing this being discussed in any investor presentation? (Or did I miss or forget something?)

Disc: Held in RL and SM

Just came across the post below on LinkedIn. $SPZ appears to be expanding via Peak Parking into the State of Indiana, US.

If this were Europe, it would be like adding a Denmark or a Finland.

Nice to see the business expanding its US footprint…. This is exactly what I expected to see and this is the first mention I think I’ve seen made to IN anywhere.

Disc: Held

There’s director buying and then there’s DIRECTOR BUYING!

just shy of a million dollars on market picked up here

I've had SPZ on my watchlist for a while but have only had time to work on it today. The stock is pretty close to fairly valued at the moment. Based on the cash flows, margin expansion, and international rollout, my model puts the intrinsic value at around $0.76 per share, compared to the current market price of $0.77. So, it’s trading right on the money, maybe just a touch overvalued, depending on how you look at it (DCF margin of safety is –1.78%).

The median result in my simulation came in at $0.755, and the range between the 10th and 90th percentiles was $0.61 to $0.90. So there’s upside potential, but the odds are slightly tilted toward the stock being priced for perfection—about a 55% chance it’s overvalued, 23% fair, and 21% undervalued (with a 10% buffer)

That said, I like the business. It has solid cash flows and a decent moat around its compliance tech, data-driven enforcement model, and the network effect it’s building across cities. It’s both a hardware and software play, and the recurring revenue model makes it capital-light once the infrastructure is in place. They’ve scaled well in the UK and Europe and are now entering the US, which adds some asymmetry if they can execute.

Free cash flow is projected to grow over 20% annually, they're reinvesting efficiently, and it’s a 9.5% ROIC business with no debt.

I don’t own it — yet — but I’ll be watching closely. It’s not screamingly cheap at current levels, but it’s not expensive either. If it pulls back below $0.70, I’d be much more comfortable initiating a position. For now, I’d say it’s a high-quality business at a fair price — and worth keeping an eye on.

Some data and other valuation results

Market Cap: AUD $305 million

Shares Outstanding: 340 million

Debt: $0.0 million

Cash: $8.5 million

Tax Rate: 30%

Initial Revenue: AUD $54.7 million

Initial EBIT: AUD $6.88 million

Initial EBIT Margin: 12.6%

High Growth Rate: 15.5%

Stable Growth Rate: 3.0%

Average FCF Growth: 20.7%

Reinvestment Rate (avg): 51.9%

Return on Invested Capital (ROIC): 9.48%

Risk-Free Rate: 4.15%

Equity Risk Premium: 4.33%

Raw Beta / Adjusted Beta: 1.03 / 1.02

Cost of Equity: 8.55%

After-Tax Cost of Debt: 4.97%

WACC (High Growth / Stable): 8.55% / 7.78%

Enterprise Value: AUD $248.63 million

Equity Value: AUD $257.13 million

Intrinsic Value per Share: $0.7563

Current Market Price: $0.7700

DCF Margin of Safety: –1.78%

Smart Parking’s H1 results get a tick from me – a reasonably strong half. Acquisition excluded, we saw revenue increase 20% (vs pcp) and total sites increase from 1424 to 1561 (vs FY24), with modest growth seen in the UK, NZ and Denmark.

Germany continues to present problems, minimal improvement since H2 FY24 off a low base. I think this market in particular was a major learning curve for management that likely contributed in a big way to their approach in the US, making a significant acquisition to assist with entering the market.

In short, I think this result was more of the same for Smart Parking. No surprise that we are seeing increases in growth capex (almost double pcp) – but well and truly expected noting their trajectory/growth. Every half year and FY report that passes, concentration risk decreases (at least I hope so -- key to my thesis). In FY24, UK sites were 79% of total sites. This decreased to 76% post H1, or 70% including the US. That is positive.

The big talking point was the acquisition of Peak Parking. Plenty of great discussion already on here, so I wont repeat any of that – only to emphasise @Wini's point that this is out of character for the business. Valuation is on the exxy side, but it does sound like they are acquiring a high-quality business and management team. If this team stick around, this could be a real winner for Smart Parking and allow them to hit the ground running noting they are a developed, mature business that already manage 134 sites across various US states.

@Wini, agree with your point also that Smart Parking could shape up to be a fundie favourite in time. Ongoing diversification (i.e. the move into the US) as pointed out by @mikebrisy, will only help in this regard too. This acquisition might also allow them to position themselves as a key global player over time. I still maintain Smart Parking has the potential to be a business worth 1billion (plus) and this acquisition probably edges them forward slightly in achieving that.

As usual, time will be critical in determining if this acquisition is a winner, but I am left encouraged. Things to watch (I will revisit in 12 months):

1. The existing management team in the US (will they all remain?). Founder has been there since 2019, while Director and Controller have been there since 2021.

2. How Smart Parking incorporate their IP into what is a different business model and what changes they make, if any

3. If Smart Parking can maintain (or improve?) Peak Parking revenue/EBITDA growth, as seen over the past 24 months.

4. How they tackle growing into other states, noting Texas has 80% of total US sites.

Valuation update to follow.

This morning $SPZ announced their 1H Results as well as the proposed acquisition of US-based Peak Parking LP for US$36.0m with an associated capital raising via an entitlement offer and a fully underwritten institutional placement.

It would be easy to focus on the acquisition – exciting that it is – however, in this straw I will focus on the operational performance for the half, leaving the proposed acquisition as a separate matter.

1H FY25 Highlights

Financial Highlights

- Revenue of $31.9m up 20.0% to pcp

- Adjusted EBITDA of $9.5m up 26% to PCP and Adjusted EBITDA Margin of 29.8% up 139 bps

- EBITDA of $9.19m up 34.6% to PCP

- "Adjusted free cash flow" (excluding growth capex) of $6.4m up 60% to PCP

- Cash of $8.5m up 17%

- EPS of $1.12 ($1.11 diluted) up 70%

Operational Highlights

Good growth in all markets, with accelerating PBN growth in the UK +18% (vs +13% in pcp) and strong growth in the profit contribution in NZ.

Losses in Germany continue to narrow, and a good start in Denmark.

My Observations

This is a good operating result. $SPZ have delivered another year of +20% revenue growth, with operating leverage driving strong EPS growth of +70%,

The UK continues to be the engine room driving almost 80% of revenue and 88% of adjusted EBITDA.

It is pleasing to see a meaningful contribution coming through from NZ, and it is still early days in Germany and Denmark, although German with sites up to 72 from 43 in the PCP, only added +5 from the EOFY 2024.

On the other hand, Denmark has gone from 11 contracts and no reported operating sites at EOFY24, to now have 21 up and running.

The new growth markets of NZ/Ger/Den are starting to make a more material contribution with aggregate PBNs growing +43% in the half vs. the PCP, compared with the more mature UK growing at a still decent (and in fact accelerating) +18%.

On cash generation, $SPZ’s curious “Free Cash Flow” of $6.4m (defined on slide 32), compares with the FY value of $12.2m – so it seems only a modest increase on a pro rate basis. The historical 1H/2H split for 1H FY24 was 49.3% of cash receipts, so their doesn’t seem to be a strong seasonal effect.

The seemingly impressive operating leverage and strong NPAT growth hides two factors. First, a currency tailwind giving a windfall of $0.74m, offsetting significant expenses growth: raw materials and consumables (+20% - in line with revenue growth), employee benefits expense (+28%), D&A (+35%), rent and leases (+52%) and other expenses (+18%).

In isolation, these cost increases might appear to be a cause for concern. However, it is important to understand that these expense lines include the impact of the expansions into Germany and Denmark, and doubtless too, the costs for a year of prospecting for acquisitions in the US.

Overall, then, the net cash generation of +$1.3m is a good result. Cash contributions from UK and NZ, more than covering the net costs of getting started in Germany and Denmark and the hunt for acquisitions.

My Key Takeaways

The business continues to allocate capital from profitable core operations into expanding the business. All markets are growing – UK and NZ strongly, Denmark is off to the races, and Germany is making slower progress.

CEO Paul Gillespie reiterated the strategic goal of achieving organic growth of doubling the business to 3,000 ANPR sites by December 2028. Achieving that from today’s total of 1561 (including the suspended 71 in QLD), represents a CAGR from end of 1H FY25 to 31 December 2028 of 18%. This can be considered in the context of the latest growth rate of 28% (to pcp) and with the US soon to provide a new beachhead for growth.

Tomorrow, I’ll write up my appraisal of the proposed US acquisition deal. But, operationally, the meter at $SPZ is ticking along nicely.

Disc: Held in RL and SM

As already mentioned, we got a glimpse into Q1 FY25 and not surprisingly Smart Parking continues to kick goals. My thesis is that Smart Parking will be able to increase revenue YoY (like it has done since 2021), with a target of more than 15-20%, while getting an attractive return on capital employed. How? They invest their cash well and their business model is bloody attractive. In terms of a thesis check, things are going well here.

Historical data

I have been monitoring their progress over several years and I figured this was worth sharing. Since 2021, growth has been steady (arguably the best way to grow). I think this business will continue to flourish into the future with the exception of any major hiccups, mainly regulatory ones, along the way. Management's new target (3000 sites) in four years speaks to their confidence also. Should they continue on this current growth trajectory, they should achieve market-beating returns and then some.

What I am looking to see over the next few years is UK sites, as a % of total sites under management, decreasing -- suggesting they are growing in other jurisdictions but also helping to reduce key market risk in the UK.

Another risk worth highlighting relates to the current management team, specifically the CEO/MD and CFO. The current CEO and MD, Paul Gillespie, has been employed since 2013, while the current CFO, Richard Ludbrook, has been there nearly 14 years. Further, the current Chair, Christopher Morris, has been in his position since 2009. Under their direction, more recently in particular, Smart Parking has thrived. That said, there is no guarantee the business performs continues to perform this well under new management. Something to monitor.

Disc. held

$SPZ held their AGM this morning.

A few positive updates, with the two key slides added below:

- 1Q FY25 is off to a good start: revenue up 24% and Adjusted EBITDA up 30%, both to PCP

- The 1500 site YE target has been achieved ahead of plan (1529 at 15 Nov) - note this targt had been accelerated from EOFY25

- A new long term target to achieve 3000 organic sites, doubling the business, by December 2028

CEO Paul noted that it's taken them 10 years to get to 1500 sites, and they now aim to add the next 1500 in 4 years.

Work on new markets in Scandinavia and the US (Texas, Florida) is progressing. Focus is now on finding the right entry point.

Demark is off to the races with contracts being signed.

UK - single industry code of practice agreed, no issues flagged under the Labour Government - regualtory environment appears stable for now. Paul thinks the Government will now monitor and see how the industry functions under the unified code.

Churn remains low at 30-40 site p.a.: mix of site redevelopments, exits initiated by $SPZ, and some losses to competitors.

Conversations under way with the new QLD LNP Government - warm but non-specific noises. Expecting movement in the New Year. Paul said he is confident they will return.

Overall, this is a company that is continuing to deliver, with a management who appear confident across all markets, with a clear focus on both operational delivery and growth.

On Valuation:

Market likes today's update. With SP at time of writing at $0.82, getting towards the upper end of my valuation. So, at 3.8% in RL, I'm a hold here. Need to update valuation in the light of the 3000-Dec. 2028 growth target.

Disc: Held in Rl and SM

@mikebrisy @Noddy74 @GazD some good thoughts already. My take: FY24 was yet another good year. Money where my mouth is: this company is by far my largest holding in my satellite portfolio (reflected on Strawman too – although my RL weighting is slightly higher). Are you insane, you ask? A weighting of 20%?! Perhaps, but my knowledge and conviction has continued to grow over a number of years, and in that time I have grown to appreciate management and their growth strategy. I have also become more comfortable with a significant weighting. That doesn't mean there aren't risks; there are several. But their journey reminds me somewhat of Codan – management recognised their reliance on the UK market (in Codan’s case, their detector biz) and in response moved to diversify operations to other markets. But they are doing this in a measured way and are choosing markets where the risks (as seen in the UK and AU) are much reduced. This theme continued in FY24 – UK obviously remains a massive part of their business (78% of total sites) but this is a reduction on last year’s 84% – and that’s with the Qld market currently paused! I forecast further reductions to this figure in FY25 as the business continues to grow in other markets.

Main highlights:

- Revenue up 21% YoY

- Total sites increased 28%, a combination of organic and acquisition growth.

- Cash flow from operating activities at 13.5m, up from FY23s 9.2m – a 46% increase.

- 12.9m outlay in investing activities – 7.7m on two acquisitions, 4.2m on investment in organic site expansion and 1m in repayments.

- Cash balance remains healthy at 7.2m despite going backwards due to above investment.

In isolation, H2 saw a small improvement to revenue vs H1, while sites under management was much improved. Net profit after tax wasn’t as strong due to a combination of FX movement, tax adjustments and ongoing investment.

Like @Noddy74 suggests, some might look at this result and think 'WTF'. But this is where we are potentially at an advantage against a good portion of the schmucks on HC but also those in the industry that monitor 745 companies. Lift up the bonnet. Overall, FY24 resulted in a strong improvement in earnings, higher cash flows and continued expansion to international operations. Perhaps most pleasing is the ongoing evidence of scaling -- key business costs represented 38% of revenue in FY23, whereas they dropped to 34% in FY4, despite continued expansion. For those that query the competitive advantage for a small mundane parking business, this is it -- the economics and ROE are fantastic and will continue to be so provided management keep their feet on the ground.

The current market cap is just under 190m, with a revenue multiple of 3.5x. In return I am getting ROCE of around 20% and a growing, profitable business with significant runway ahead of it. With the share price where it is, I don't think we are far away from fair value. I plan to update my DCF/valuation in the next 24 hrs.

Key risks remain regulation, particularly the ongoing discussions in the UK, in addition to poorly executed expansion. I anticipate a decent outcome for Smart Parking in the UK, but an unfavourable decision could result in a very ugly short to medium term impact. I don't think this is likely. Agree with @mikebrisy that Qld isn’t critical to the business but remains a nice to have.

Overall it was a solid update from Smart Parking last week with strong topline growth and decent cash generation being partly offset by unfavourable FX movements and increased overheads.

The key driver of the results is, as always, sites under management and on this measure they continue to deliver. The Group held 984 sites at the reporting date, which was up from 839 sites six months prior. They were keen to highlight that they've since exceeded 1000 sites, although you could argue QLD sites should be backed out of that number. Although the 1000 site target has been replaced by a 1500 site by June 2025 target, longer term holders will remember that 1000 sites by June 2023 was an earlier target and it deserves mention that they have beaten this. On the earnings call they reaffirmed the 1500 site target and I asked them to clarify if that meant ex-QLD, which they confirmed was the case.

Revenue was up 18% vs pcp, but up 25% from a constant currency perspective. UK growth is impressive given its relative maturity but the real driver is APAC, half of which we now know is - at best - on pause. Germany doesn't yet make a material contribution and will be on watch going forwards to ensure it does do so.

At the same time operating expenses appear to have jumped significantly and permanently. They strike me as a little sensitive about the investment in Germany relative to the return they're getting and I'm not fully on board with their practice of backing out Germany's costs from Adjusted EBITDA. However, it's all fairly transparent so you can rework it as you see fit. Overall a reasonable level of explanation was given to the cost uplift but going forwards I'd like to see that increasing at a lower rate. I have asked for clarification about what the disclosed monthly exit opex rate of $1.7m includes as it's not entirely clear, but that equates to a six month number of $10.2m - not too much higher than the disclosed half yearly opex cost, suggesting that opex growth may have slowed.

Free cash flow was strong but again it should be noted they are excluding Germany's costs from their definition of this. It's all very transparent though so choose your own adventure on what you do there. It also doesn't include Growth Capex (almost all of their capex isn't ongoing). I'm ok with that, others won't be. The balance sheet continues to look good and they have flagged a continuation of their share buyback (which they announced to the market they had started acting on a few days later). They've also started talking about dividends. I assume they will be unfranked given their overseas operations so I don't much see the point of that unless they've completely run out of ideas, but it is another indication that they do seem to act in alignment with shareholders.

Kudos for them holding an investor briefing. One of the themes I felt this reporting season has delivered is somewhat less of those and credit goes out to management who front up when the news isn't necessarily all good. Based on the attendees they do seem to be getting a little more insto coverage, although some of the questions seem to suggest the analysts hadn't had alot of exposure to the business yet.

In summary

The good:

- Site growth is the key driver and is tracking nicely. I haven't even mentioned the Technology segment of the business here as it's become an increasingly immaterial part of the business.

- As expected Revenue growth is following sites under management. Previously the CFO has said they could deliver $70-75m at the topline with 1500 sites. My model also supports this, albeit at the bottom end of that range. At that kind of number and given their propensity to gush cash, they'll be hard for the market to miss.

The not so good:

- Germany isn't yet shooting the lights out but it's early days. @Wini highlighted an Aldi win they'd had in this market some time back and they disclosed they now manage two Aldi stores, in deals signed off at the northern Germany region head office. According to Wikipedia Aldi Nord is the bigger of the two Aldi regions and has 2298 stores.

- I think the market was a bit disappointed to see the Cost base jump as it did. It's fair to say I was a bit too and this is on watch going forwards.

The ugly

- I think the prudent thing to assume is Queensland is not coming back and be pleasantly surprised if it does. I asked management on the investor call what learnings they took from this and someone asked something similar on the Strawman call. Both times they highlighted the lack of a Code of Practice in Queensland that does exist in other markets they operate in and that this would prevent a recurrence. I think the fact they were blindsided like they were suggests they and the peak body didn't do nearly enough work with the government to advocate/educate/put a code in place etc. and being proactive should be a key learning.

Overall I'm still happy to hold. I took a little profit at higher levels but it's still a larger holding and I think closer to a buy than a sell given it's pulled back a bit and should be supported by the share buyback if that continues.

Coming so soon after a trading update, SPZ's AGM was held this morning without a great deal of fanfare or controversy. A couple of new updates were given though. Smart Parking held 930 sites under management as at 31 Oct. That's up from 839 from 30 Jun and puts them on track to meet and beat their target of 1500 sites by Jun 2025. To add some context to that, according to them there are 150,000 sites available in markets they currently operate in - so their target is to manage 1% of those sites.

It also appeared that cash had rebounded in October and management included a waterfall to show movement of cash in the first four months of this year. They also forecast capex spend to be $4.5-5.5m in FY23. The nice thing about that spend is that it immediately starts paying for itself; it's not building capacity that you then have to go out and try to get someone to pay for.

A couple of other notes from the meeting:

- About 20 sites from the NE Parking acquisition (517 manual sites) have been converted to ANPR. Even they acknowledge it's not going as quickly as they would like but they don't need much more than that to justify the acquisition. I don't think of NE Parking as an acquisition per se - it's more like they paid a nominal sum to add a lot of sites to their pipeline and it may be a couple of years before they exhaust the pipeline.

- They're not yet seeing more challenging economic conditions being reflected in either traffic volumes or delinquency rates. In fact, October was a record receipts month for the U.K.

[Held]

Snap @Rocket6 you just beat me to it

***

Busy day...start of a busy week...

Smart Parking's result this morning was better than I expected on most measures. Revenue was up 68% on FY21, mainly in the parking services business (i.e. fines) due to a 36% increase in sites under management and considerably higher yield per site. Adjusted EBITDA was $8.8m in FY22, compared to $2.2m in FY21 despite considerable investments and additional headcount for future growth and normalisation of other opex items which benefitted from COVID in the prior year. Adjusted NPAT went from a loss of $1.7m in FY21 to a profit of $2.2m I normally don't like to see an Adjusted NPAT but given the $6.9m one-off VAT win the company had over the HMRC in FY21 I think it does make sense in this case.

The company claims a free cash flow of $8.1m but they do exclude capex from this (but do include lease payments) on the basis that they classify this all of this as growth. Given the nature of their business I think it probably makes sense that they wouldn't incur maintenance capex and I can accept their reasoning (Claude is shaking his fist at the monitor right now) but if you don't just add it back - I think the valuation stacks up even if you do.

Some notes from the call and releases this morning:

- Sites under management (being a key metric) are scaling up nicely and on track for previous target of 1000 by end of FY23 and new target of 1500 by end of FY25

- New markets:

- NZ - 20 sites, EBITDA and cashflow positive. Target of 75 by June 2023. 3000 potential sites.

- QLD - 27 sites. Target of 80 by June 2023. 2000 potential sites.

- Germany - foothold of 4 sites. Target of 70 by June 2023. Dunno how many potential sites, lots - possibly twice that of the UK, which has 45,000 potential sites.

- Share buyback to continue while share price remains depressed

- Overheads grew substantially but management have indicated this was due to some investments for growth (e.g. Germany) and end of furlough schemes etc. and shouldn't grow at the same rate going forwards

- Acquisitions are performing at (NE Parking) or ahead (Enterprise) of targets

- Technology segment was EBITDA positive. This was a bit of a surprise to me. In previous conversations management's commentary wasn't that bullish in relation to that business.

- July and August to date have been record months

- Regulatory overhead of Parking Code of Practice is still on hold and government hasn't provided update (they've understandably been busy giving Boris the arse). Interestingly Paul stated Smart Parking and the majority of the industry would like to see most of the code implemented - just not the bits that cap their fines.

- Are seeking more acquisitions or markets. They are limited to juristictions that allow number plate owner databases to be accessed, which is why QLD is the only state in Australia they have thus far entered.

So overall very positive. I mentioned to someone this morning that there are some things I don't love. In particular I think they could do a better job of presenting the statutory accounts to be somewhat more aligned to the management accounts. I get they serve different purposes but GAAPs aren't completely prescriptive and other companies manage that better than they do.

I also don't love the word Adjusted in front of EBITDA and NPAT but I've always found them pretty transparent about what has been adjusted and you can backwork it if you want to. Those are relatively minor quibbles compared to keeping the business on track and delivering on the promises they've been making, which so far they seem to be doing.

Held here and IRL

We weren't provided with any revenue or profit figures, but still get some insight into SPZ's H2 period.

- Parking breach notices (PBN) are forecast to increase by around 70% vs PCP. While this figure hasn’t moved much since the H1 increase, it marks a strong year for SPZ. Q3 was the slowest quarter of the year for PBNs issued, while Q4 is forecast to be an improved one (second highest).

- Sites under management was recorded at 816 (as at 31 May), an increase of 32% PCP. A total of 99 sites have been added thus far in H2, noting June figures still need to be added. A breakdown based on region (and churn) is recorded below. While total sites under management (99) wasn’t anywhere near as high as H1 (176), churn in H2 has been much more respectable – 20 in H2 vs 58 in H1.

- 42 sites are now up and running in the APAC region, while the sales team was doubled to ‘capitalise on market opportunity’. If my calculations are correct, total sites under management has effectively doubled in H2 (from 21 to 42). PBNs in the region continues to trend upwards nicely (below).

- As for their push into Germany, four customer contracts were signed, with two locations live and generating revenue. 0.5m OPEX costs for the half suggests they aren’t throwing lots of money down the drain as they try and shift into a new market. This is obviously pleasing in this current environment.

Smart Parking continues to be one of my higher conviction holdings. Pending the release of the FY result (where I will have a proper dig into the financials) SPZ is high on my 'top up' list at the moment. They continue to grow at impressive levels, they are profitable (based on H1 reporting) and have a solid balance sheet -- the latter provides them with stability and an ability to fund their growth strategy inhouse. They aren't impacted by supply shortages and are in a good position to make strategic acquisitions when the opportunity arises. Provided the FY report reflects more of the same, management continue to demonstrate that they are solid capital managers.

@Noddy74, any differing thoughts?

Just doing some due diligence post-half year reporting and came across this disclosure about an acquisition SPZ had then recently bought (the disclosure was in 2012 for an acquisition made in 2011). I'm not sure I've seen a more brutally honest summary of some of the issues facing the business - if you've seen a better one let me know! They couldn't even fit it all on one slide (the third dot point on the second page is particularly funny/scary):

Fortunately SPZ has come a long way in the past couple of years under new management. There are risks that I want to look into and write up over the next few weeks but overall I see this as a business that finally has clear short and medium term targets, is on target to deliver on those and will eventually get rewarded for that with a re-rate.

[Held]

Smart Parking released half year results this morning above guidance for both revenue and EBITDA.

This is now a consistently profitable company and cashflow positive company with increasingly bright prospects as it moves into new markets (Australia, NZ and Germany) and continues to broaden its offering. About the only thing that could be seen as a negative was the fact net operating sites (a key metric for them) fell by one in the quarter to 737. However, this was explained on the call as a combination of their decision to rationalise underperforming sites as well as the loss of one customer with multiple sites and was further allayed by the fact they disclosed sites under management had grown to 772 as at 18 Feb.

Some other highlights and thoughts from the call:

- margins have expanded to over 90% and they see the prospect for this to grow further (doesn't quite square with the fact they have flagged an influx of lower margin technology revenue in the second half)

- Starting to get traction in NZ and Australia with NZ EBITDA positive in 1H and Aust expected to be EBITDA positive in 2H

- Flagged confirmed order book of $4.8m for technology sales, most of which will be delivered in 2H (compared to only $0.3m in 1H). Gatwick Airport represents $1.3m of this number and the timing of recognition of this is currently uncertain.

- Expecting an increase in opex in 2H to support rollout into new markets.

- Long discussed new U.K. parking legislation has finally been tabled. Among other things this legislation will cap/standardise the parking fine amounts that can be charged in different locations and situations. This is a major and high-margin revenue source for the company. Overall the company mostly views the changes as positive, although they're still need to get some clarification of the interpretation of some of the legislation. I tried to get some more clarity around the financial impact of these changes but they weren't giving up their modelling at least until they got more clarity around those interpretations.

- The legislation increase compliance costs across the industry. By itself that's not great news but management believes it's a net positive as it will impact smaller operators most and will drive consolidation in the industry.

- Targeting 200 new organic sites annually (already had targets of 1000 sites by Jun 2023 and 1500 by Jun 2025).

- SPZ acquisition was completed in Aug 2021 for $1.5m and contributed $850k of revenue in its first 4 months of ownership.

- Q2 revenue actually exceeded Q1, despite being a traditionally quieter quarter. I wouldn't be surprised to see this slow somewhat in Q3 before beginning to grow again in Q4.

So overall a very good result. This is a business which is much de-risked from when @Rocket6 first starting writing about them but hasn't caught any love from Mr Market just yet, who may want to see what the impact of the new UK legislation (to be implemented on 31 Dec 2023) is going to be. With the already booked tech sales I think they could deliver revenue of $38-40m this year and earnings of $5-6m. I'm a big fan.

[Held]