Discl: Held IRL 4.94% and in SM

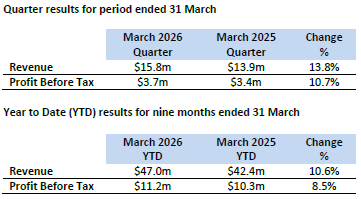

Another steady-as-she-goes 3QFY26 report from XRF. 2 things that stood out:

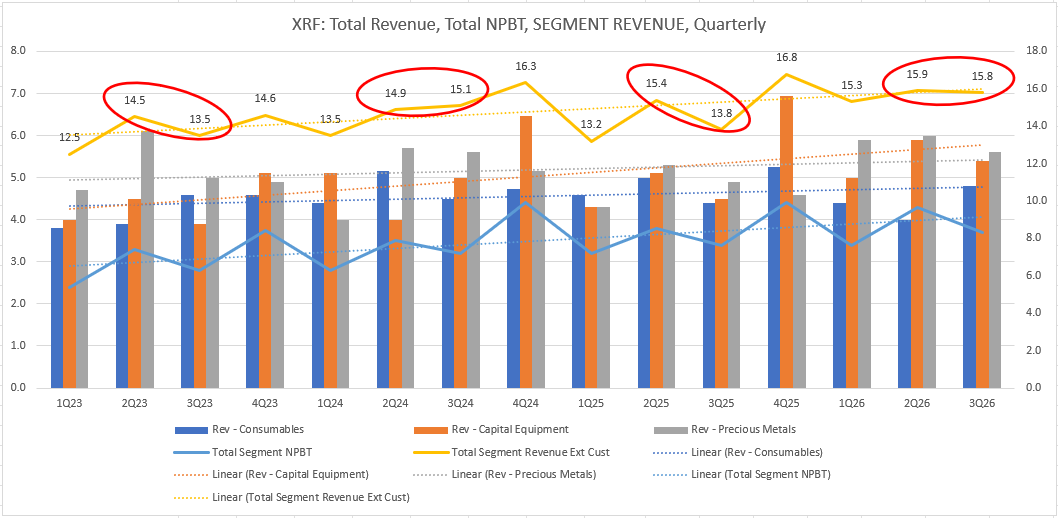

1. The QoQ movement between 2Q and 3Q has always been interesting - in FY23 and FY25, revenue drops were reasonably sharp (red ovals in chart). But in FY24, it was flat. FY25’s flat QoQ result is more or less in the zone of the seasonal 2Q to 3Q movement, hence the steady-as-she-goes summary.

2. The language of each segment update feels quite upbeat, but delivered in typical Vance’s understatement style - it does feel like a setup for aanother seasonal uptick in revenue in 4Q as has been the case for the past 3 years.

International sales flagged as the key quarterly growth driver

Cost of setting up shop and India looks to have been absorbed nicely, first customer orders received in Mar, well received by customers

Consumables - $4.8m vs $4.4m pcp

- Record month in March from both dollars and product volumes

- “Scale, momentum and timing of incoming orders meant these sales will now be recorded in the June quarter” - driven by Asian customer demand - this sets up 4Q to be a good one, consistent with the seasonal pattern

Capital Equipment - $5.4m vs $4.5m pcp

- Increase in Orbis crusher activity, $2.5m sales achieved

- Activity driven by the gold sector, momentum expected to continue through to the June quarter

- 1st Next Gen xrFuse 1 and 2 orders were shipped to customers during the quarter, new production line now operational

- XeTGA revenue continues to grow, order book increasing and repeat sales received

Precious Metals - $5.6m vs $4.9m pcp

- Reduction in platinum prices started to have positive impact of demand towards the end of the quarter

Non-Executive Director David Brown sold 1m shares, 10.84% of his 9.2m share holdings in XRF between 2 and 8 Sept 2025. This reduces his ownership in XRF by 0.71% from 6.56% to 5.85%

- Sale for financial diversification as the vast majority of his investments are in XRF shares

- Does not currently have a plan to conduct any further share sales

No huge concern for me. Caused a dip in the XRF price after the recent post-earnings rise, but these dips are fairly normal for XRF.

Mr David Brown (non-executive director)

David has over 40 years of experience in the research, development and manufacturing of X-ray flux chemicals. He pioneered the commercial development of X-ray fluxes in Australia and was responsible for the commercialisation of current formulae now used by most Australian X-ray flux users. David was previously Chief Chemist for the Swan Brewery Co. Ltd, where he carried out research involving the separation of proteins by gel electrophoresis, a technique that has subsequently progressed to the modern techniques of DNA separation and profiling. David holds B.Sc. and B.Ec degrees from the University of Western Australia and has held the position of Chairman of the Scientific Industries Council of WA.

Discl: Held IRL and in SM

Looks like order has been restored with the XRF price, following the FY25 results 2 days ago!

- XRF made a new all-time high today of $2.28, closing at $2.26

- Following the previous high on 21 Feb 2025, the price retraced to around 60% with the low of $1.44 on 7 Apr 2025 - textbook retracement, really

- It then went sideways around the 50% retracement line at ~$1.54-ish, before forming today's high

The XRF chart is one that tracks its results very nicely ...

As I am, unfortunately, very price anchored from my entry at lower levels, I am now seriously contemplating signing up to the XRF Dividend Reinvestment Plan, which has a 2.5% discount, as the only way I to get over this price anchoring and very slowly increase my exposure ...

Discl: Held IRL and in SM

@RogueTrader posted this Rask podcast on small caps which talked about XRF.

https://www.youtube.com/watch?v=Kg8RQKG72xQ&ab_channel=Rask

The one point I picked up was that the Seneca boys use the lab mining sample volumes from the big Labs SGS, ALQ, as a leading indicator for XRF consumable volumes and revenue.

Quite an interesting chart from the ALQ FY25 Annual Report of 27 May 2025 in terms of the noticeable sample volume spike in 2025 through to 16 May 2025, implying the flow through to XRF consumables volume.

Another small and sensible XRF acquisition to add to XRF’s portfolio of capital equipment for $1.16m upfront and $0.3m earnout.

With $12.0m of cash at 30 June 24 and $8.1m positive operating cashflow in FY24, this cash + 15% of consideration in XRF shares deal will barely cause any financial dent.

This is more of XRF’s sensible, incremental-step approach to acquisitions. I like how this expands products to XRF’s existing markets as well as expand into newer, non-traditional mining sectors.

Discl: Held IRL and in SM

-----------------

XRF has entered into a binding but conditional to acquire 100% of the shares in Labfit Pty Ltd ("Labfit").

Labfit is a manufacturer of Carbon Sulphur Analysers, pH Analysers and laboratory weighing systems. Carbon Sulphur Analysers perform elemental analysis of Carbon and Sulphur in samples for mining and industrial production applications. pH Analysers are used to determine how acidic, neutral or alkaline samples are. They can be used to test samples such as drinking water or soils for agriculture, for productivity, quality control or safety purposes

For FY23 and FY24 Labfit produced average unaudited revenue of $1.5m and profit before tax of $0.2m. The business currently has a blue‐chip customer base of commercial laboratories, miners and industrial producers.

Combined my notes on the 30 Sep 2023 Quarterly Update and today's meeting with Vince Stazzonelli.

Discl: Held IRL and in SM, looking to top up IRL if the price falls closer to $0.90.

Built this simple revenue xls to get a better perspective of the 1QFY24 results against FY23, will add in subsequent quarters

- Solid result with PBT growing much more than Revenue

- Consumables was up 15.8%, Capital Equipment was up 27.5% but Precious Metals was down 14.9% over the PCP

- Revenue is 5.9% lower than the average FY23 quarterly revenue (average is annual revenue divided by 4)

- Not a concern given the large forward orders held for Precious Metals, but puts the 1Q result in better context, taking cue from concerns previously about the rate of growth from H-to-H

- All segments appear to be firing, with the order book for capital equipment at record levels, and production for some products is now being scheduled for the June 2024 quarter

TAKEAWAYS FROM VINCE MEETING

Industry Tests to test quality of a product which XRF Supports

- XRef Analysis - using X-Ray Fluorescence analytical technique to determine the major components of a sample

- ICP Analysis - ICP (Inductively Coupled Plasma) Spectroscopy is an analytical technique used to measure and identify elements within a sample matrix based on the ionization of the elements within the sample.

- Gold - FireAssay and PhotonAssay (C79’s technology)

- Platinum Labware - this is used in the sampling process. XRF manufactures Platinum Labware for all machines, not only XRF-specific machines

How the XRF Equipment Comes Into Play

- Orbis Mining Crushers - breaks down (crushes) big rocks to provide powder samples, which are then used as inputs to the various tests

- XRTGA Thermogravimetric Analyser - a high-temperature furnace, heats up the sample to run tests at different temperature points

- Market is dominated by key competitor: Leco

- XRF’s benefits over Leco units:

- 30 samples at a time vs 18

- Has heating and cooling cycles to speed up the process

- User friendly Touch Screen vs separate computer console

- Reputation of building reputable products

- Provides complementary data for XRF analysis

- XrTGA opens up access to new markets for XRF - Pharmaceuticals, Food, Agri-Products, Plastics etc

- Capital equipment should have at least 7-8 years of life through to 15 years

- Drives other products - spare parts, labware rework, consumables

Manufacturing Capacity

- Solved factory capacity issue for Capital Equipment this past quarter

- Can ramp up production across all 3 segments by adding more shifts - no further major spend to boost capacity is anticipated

International Expansion

- Already have presence in Europe (Germany and Belgium), North America (Montreal), Australia and parts of Asia

- Direct sales are fulfilled in Australia

- Large network of Distributors which are required to provide on-the-ground customer support

- Not in a position to open offices in many countries - driven by product line and the individual needs of the countries

Cost Pressures

- Cost pressures of the last 12-18M have eased in the last 3-6M - lead time blow outs

- Able to pass on price increases to customers who mostly pay based on the metal spot price at the time of invoice

- Employees were given good pay increases to retain them

Customer Demand

- Exploration activity mostly focused on Rare Earths, Lithium

- Exploration spend did not fall in Australia - Gold spend did fall, but Base Metals, Iron Ore continued to perform well

- Have not seen anything impacted by a slowing of Chinese demand

Capex Management Approach

- Dividend payout ratio is around 60% - this level of dividends is able to provide required capital for R&D, Inventory and Working Capital

- On the lookout for bolt on acquisitions - generally like to issue script to fund these acquisitions to incentivise vendors

- Ideal targets are (1) lab products which have business synergies with XRF’s products (2) used by existing customers (3) are under-developed in market potential

- Not interested in building business scale as XRF is at “about the right size” - focus is on value adding acquisitions

Key Investor Misunderstanding on XRF

- Investors misunderstand where XRF sits in the laboratory process

- High quality products

- Strong IP

- Essential in providing data to mines, industrials

- Critical to customers processes