Alcidion out with a short and sweet announcement today (see below).

With the addition of the $5.5 - $6.5m revenue being recognised in FY26 - this should nudge them over the magic number of $40m in revenue which is what they have needed to hit FCF. Still circa 7+ months in the FY, so barring any cancellations they should now be at the FCF inflection point...

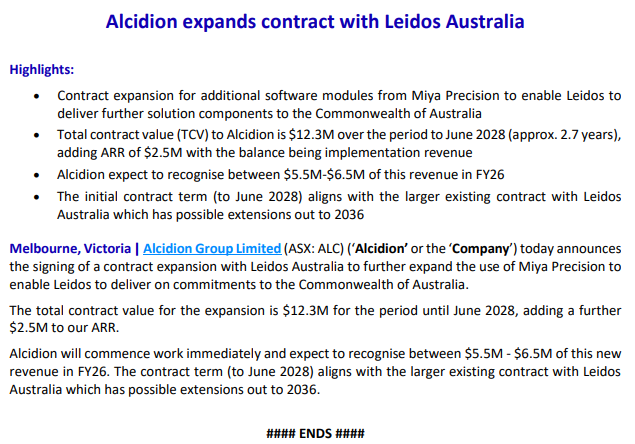

Disc: Held IRL and SM.

Short and sweet guidance upgrade from ALC this morning.

- Fairly decent increase in EBITDA guidance of circa 50%

- Smaller contract upgrades always nice - but will take it with a grain of salt

- Interested to see what costs continue to be cut - there is a happy medium here.

Disc: HELD SM IRL

Decent quarterly update from Alcidion today.

Highlights:

- Upgraded guidance for FY25 EBITDA expected to be >$3m and deliver positive cashflow

- Q3 cash receipts of $13.1M with a positive operating cashflow of $2.5M (compared to a cash outflow of $1.4M in Q3 FY24) and includes no receipts from North Cumbria Integrated Care (NCIC) NHS Trust

- Q3 new TCV sales of $48.8M with $11.5M expected to be recognised in FY25 o Signed new $37.5M, 10-year milestone contract with NCIC NHS Trust to deliver new Electronic Patient Record (EPR) platform o Signed new 5 year, $5.5M contract with Hywel Dda University Health Board, our first customer in Wales o Renewed several PCS (PAS) customers

- FY25 contracted (sold and renewal) revenue stands at $40.2M at end of Q3

- Cash balance of $10.2M and no debt as of 31 March 2025 o Expecting a strong Q4 of receipts with a debtor ledger of $17.7M at the end of Q3

As illustrated by the graph of cash receipts (refer above), Q4 is historically the strongest period for customer receipts, a trend that we expect will continue in Q4 FY25, underpinned by a debtor ledger of $17.7M at the end of Q3.

Overall a pretty rosy update, are they rebuilding our confidence and trust?

Disc: Held IRL and SM.