Consensus community valuation

As I exit this morning's investor call, today I have exited my holding in $CSL.

Last year, following the SP plunge and the announcement of the transformation, I took an initial position in $CSL fully believing it to be undervalued, intending to add to my position as I gained confidence (or if the market continued to improve the opportunity from a value perspective!)

Today, I have reversed that decision, and exited completely.

First, let's be clear that this is still a strong company, throwing off US$1.3bn in operating cashflow, which was +3% on a CC basis.

And let's further be clear, that management are sticking to the guidance announced at the AGM, as below.

Others will no doubt give a more detailed assessment of the result, so I'll spare the details and get to the arguments that tipped me over the edge.

US Recovery - Not a Hope for Me to Invest In

The situation in the US is not good. The Trump-RFK regime are materially unwinding vaccination programs to the great detriment of health - young and old - in the US, particularly in vulnerable populations. Management spoke of their belief that stakeholder support to reverse policies is growing. While that's good, the current US Administration is proving itself resistent to influence and arguments based on fact and science, and if ever, when things are going badly create false realities, new scapegoats and double-down. My fear, is that US policy change is a FY29 improvement as a base case potentially not materially impacting results until FY30. While this was a definite risk on my radar screen at the time of the AGM, I have been aghast at what the US Administration are prepared to do to their own people, and their responses when things go wrong. I cannot see the "MAHA" agenda succeeding, and it will only be reformed when the leadership changes.

One Strategic Reset is Doable - But How Many Will We See?

My investment thesis was predicated on an aligned board and mangement team, a pre-requisite for a transformation to be successful.

Now we face a transformation program already in flight crafted by one CEO, now to be stewarded for one year by another CEO, before being handed off hopefully in FY27 to a third CEO. No matter how safe a pair of hands trusted lieutenant Naylor is, from my perspective that's 2 hand-offs too many. With each leadership change comes the likelihood of next level disruption, restatements of what can be achieved, and internal instability.

Not for me thanks.

$CSL is clearly not on the right track in the view of the Board. OK, they signed off the strategy, so all they could do next was agree to "retire" the CEO because they have formed the belief that he isn't capable. Which means that they failed first in their decision to appoint him as CEO in the first place, and then secondly, to endorse his transformation strategy. That now surely means that the entire Board is on notice. And so investors have to face the real risk that there is a revolt against the Board, and within the next 1-3 years there is further turmoil.

I'm not in a position to comment on whether McNamee and the Board made the right deicsion to "Retire" the CEO. But what I can say is that the leadership dynamics around this business are not setting up the company for success. It would be one thing if $CSL was firing on all cylinders and performing. It is not. There are political and regulatory challenges, there are problems with the strength of the new product portfolio, there is a major restructuring in train, and there are competitive challenges with existing products.

This is a business facing multiple challenges, with the real prospect of leadership instability for the next year or two, at least.

Not for me.

In restrospect, my decision to enter last year was not a sound one. At least it was only a tentative first step.

Today, I am reversing that tentative step and move back to the sidelines. I made a mistake. But it would be an even bigger mistake not to admit it.

In terms of valuation, it is entirely plausible to believe $CSL is now materially undervalued. I believe it probably is, although, as shown by @Strawman, the business is not cheap for one with questionmarks over its growth prospects in the medium term, as well as questions about the productivity of its R&D portfolio and spend. For me, the question is as much what is the pathway for that value to be realised and recognised by the market. And I just see too many risks around that to have any conviction. It is better to rip the bandaid off.

I'll further remark that the decision to sell (even at a sizeable loss) is a relatively easy one. Across my portfolio and watch list is a long list of other comanies whose share prices are beaten down way below my valuations. I've exhausted my cash resources buying into these ideas on the way down, and I can now look forward to putting my $CSL proceeds to work in places where I have a higher conviction.

Disc: Not held

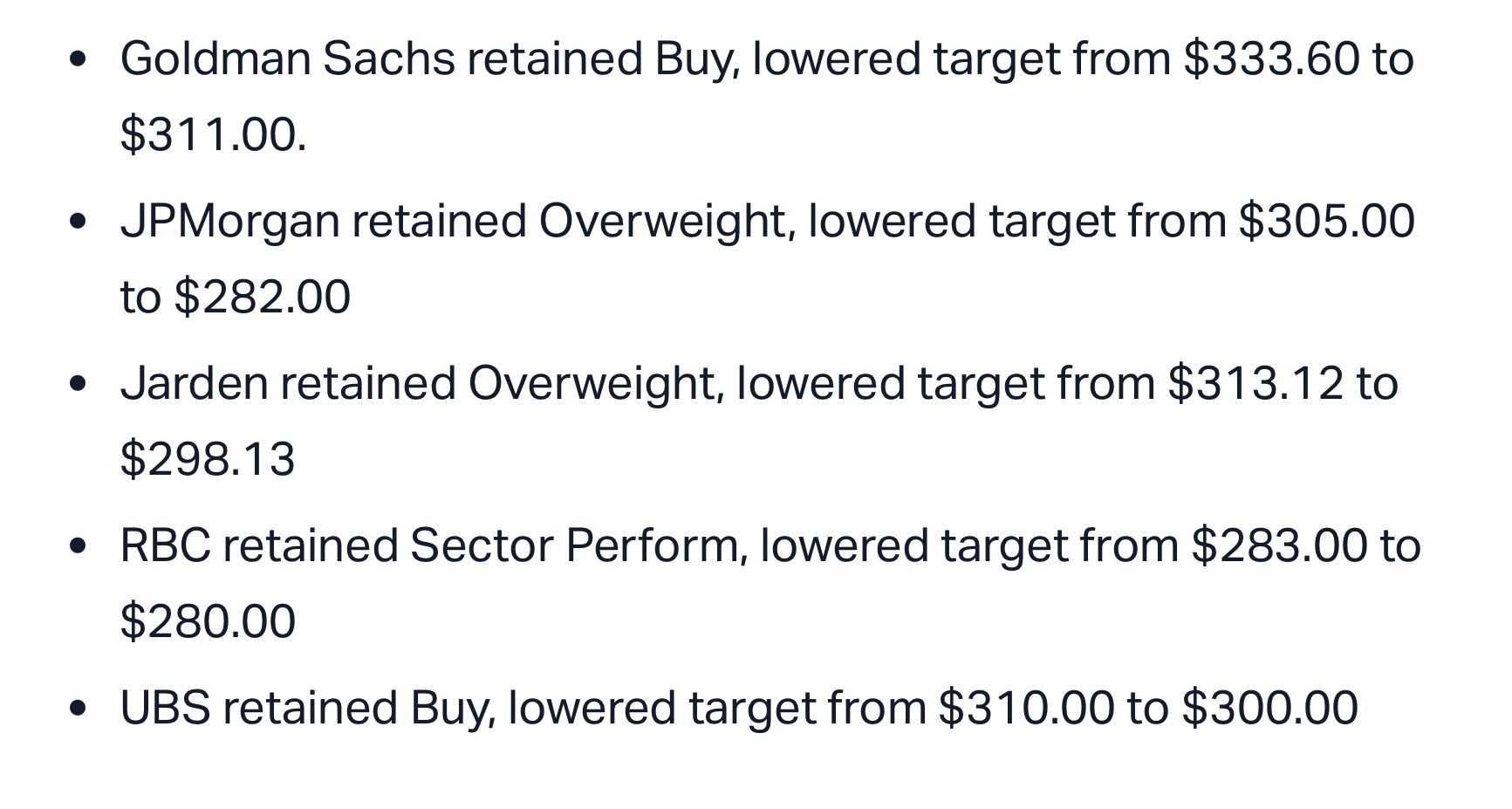

Revised broker targets off the back of the AGM downgrade today -

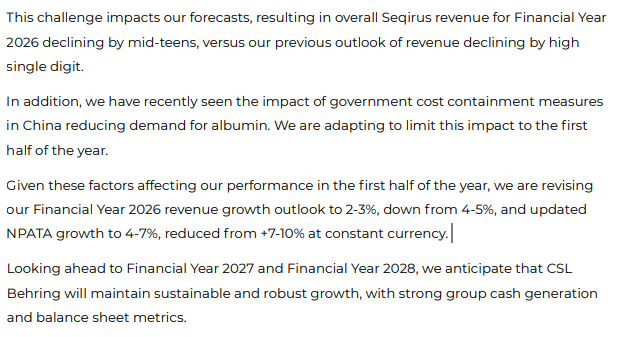

Downgraded earnings for FY26 and future to high single digit from double digit. Postponed Seqirus.

Wonder if something caused this...

"AMERICA IS IN the throes of its worst flu season in at least seven years. The Centres for Disease Control and Prevention estimates that some 29m Americans have been infected since October—20% more than at the same point last year. For the first time since 2020, the flu is leading to more hospitalisations and deaths than covid-19."

Good results from CSL with the unit that made CSL great - Behring - continuing to do all the heavy lifting - Vifor was definitely diworsefication...

I'm just out of $CSL's capital markets day and, as ever, the deep dive into each of the three businesses and the R&D portfolio always leaves me in awe of what a tremendous business this is and the breadth and depth of talent on the management team. There are too many moving parts to summarise the day effectively and, I work on the basis that anyone who was so motivated would have been there anyway. So, instead, I'll pull a few selected slides from the deck with a brief explanation of what they said to me.

My Key Take Aways from the Day

- $CSL will sustainably grow earnings at double digits annually for the foreseeable future. FY24 guidance was re-affirmed.

- It continues to sustain its R&D pipeline with new discoveries, with several exciting near-term, late-stage milestones for FY24

- Gross margin and ROIC will progressively improve year on year over the coming 3-5 years or so, driven by a program of efficiency improvements to drive plasma recovery, a period of 3-years of reduced capex and debt moving back to 2 x EBITDA by EOFY24.

- Overall, revenue will be driven by the tailwind of ageing populations in developed markets; label expansions of the existing portfolio; growth of recently launched products; and new approvals expected.

- The company has a framework for disciplined capital allocation, focused on sustaining growth while increasing shareholder returns over time

Today was Paul McKenzie's first outing as CEO for Capital Market's Day. He did a good job topping and tailing the day, supporting his team in the Q&A, and letting the team do the heavy lifting as you'd expect. As far as I am concerned, he did a good job and the first test will be meeting or beating FY24 guidance.

Capital Discipline

I start with Fig.1 the framework for capital discipline presented by CFO Joy Linton.

Figure 1

$CSL continues to invest strongly for growth. The next several years will be some transitionary points:

- A progressive return to pre-COVID %GM in the plasma business, with a promise to grow margins beyond these levels as a result of a range of investment in IT and manufacturing technology to reduce CPL (costs per litre) at the collection stage and increase plasma yield through manufactuing. This isn't something that just happens, and the team outlined some of the details of improvements being made in the collection centres and in the plasma extraction processes.

- A reduction in capex of c. 30% over the next three years. This follows the completion of a major program of new facility investments over recent years

- NPATA growth allowing the debit required for the Vifor acquisition to be reduced back to the target level of < 2 x EBITDA - a conservative position that should retain investment grade credit rating.

Revenue Growth

$CSL expects to grow strongly across all its businesses. The positioning of each of the three businesses and the market opportunities are summarised in Fig. 2.

Importantly, many of the conditions for $CSLs treatments are related to ageing, so there remains a long-term trend of ageing over the coming decades in developed markets, then to be followed in the future in the middle income countries. Even in developed markets, there is a significant variation in uptake of $CSL products, so there is significant opportunity in driving product use to a more uniform adoption of the standard of care in the most advanced markets. New indications for existing products come on top of that.

In summary, there are many levers for growth offset of course by competition and new tharapies, of which GLP-1s are just one of many.

Figure 2

Although the story for Iron (i.e. Vifor) was perhaps less confident (from my perspective) with indications that progress may be lumpy, this is more down to the uncertainty of how rapidly the growth of Injectafer will take off following approval for Heart Failure in the US and the approval of Ferinject in China, offset by the launch of generic competition from Sandoz (CEO Paul McKenzie emphasised that generic competition was in the acquisition case, but I sense that with the manufacturing challenges of the drug, Sandoz has perhaps been a bit faster out of the blocks than expected).

Of course it is important to remember that adding treatments for renal failure and CKD complements $CSL's other therapy areas, so Vifor is as much about building capability as it is about buying a portfolio of drugs. CFO Joy Linton summed it up when she pointed out that CSL's prior acquisitions have usually taken several years before their promise has materialised, pointing to the 3 years it took for the value of Sequirus (acquired from Novartis) to show through.

We've recently heard how $CSL has been in the gun sights from analysts and commentators from GLP-1 FLOW clinical trial. Head of R&D Bill Mazzanotte addressed this in his opening remarks. He pointed out that cardi-vascular diseases are of a "multi-dimensional and complex nature". By this, he means that there are many diseases within the category, and for each disease there are many indications according to patient profile, disease type and stage of advancement. Reflecting on the hype around GLP-1s, Bill pointed out that 25 years ago Statins were emerging and commentators were saying that would be the end of cardiovascular disease and the existing drugs that treated them. "It didn't happen," he said. He further added that there are many drivers of renal disease, and that weight is not an independent driver (a bit like we've debated here on OSA). While he accepted there will be an impact he considered it to be a small impact on a small part of the portfolio. He summarised by saying "I am proud of the scientists who have done the work. I am grateful that patients have a new opportunity. But I am confident of our product and R&D portfolio."

From that respect, today was good for my general well-being. Having a day immersed in the CSL portfolio reminded me (as a non-clinician) just how complex and multi-faceted disease is, and how vast the array of treatments and modes of action are. It is highly, highly unlikley that any one mode of therapeutic action is going to be a "silver bullet."

R&D Portfolio

Bill Mazzanotte gave an update on R&D. At the headline level, several new candiates were added to the Phase 1 pipeline from different CSL "platforms" across the therapy areas; several drugs advanced throught the pipeline; and several candidates were dropped. Fig 3 shows the FY23 progress in the R&D portfolio and Fig 4 shows the updated portfolio and fig. 5 shows the key expected milestones for the next three years. (I'll be interested to read some of the broker notes on this, particularly GS, whose global healthcare desk will no doubt do a detailed analysis, considering similar developments across the competition. That's more than I can ever do! Chris Cooper asked several questions during the day, so I am sure there will be an update.)

Figure 3 FY23 Progress

Figure 4

Figure 5 FY24 R&D Milestones

Key milestones are Garadacimab approvals decisions, and Phase III results of CSL112.

Articificial Intelligence and IT Generally

Chief Information and Digital Officer Mark Hill gave a short and interesting presentation of how $CSL is using IT to drive value both in R&D and Operations.

Mark who is a IT veteran of four decades in industry made the following remarks which stood out. First "AI is here to stay, and it is bigger than the internet" and second, it is "difficult to harness because the speed of innovation is faster than anything we have seen."

However, this wasn't a buzzword-hype presentation. On the contrary, Mark gave practical examples of the kind of things that $CSL are applying generative AI to, and they have even built an internal accelerator to innovate, test and then deploy useful applications. ("No one need write meeting minutes again")

I'm calling out this segment because I think across industries, AI - like digital before it and ongoing - will lead to capabilities that the best companies will figure out how to use, and then gain benefits from so doing. Some will succeed, others will be left behind.

And as @Strawman said in the last episode of Baby Giants podcast, if I recall correctly, in quoting Warren Buffet, AI will be like attending a parade, where some stand on a box to get a better view. But eventually, everyone is standing on a box, so no-one has a better view.

From a competitive perspective, however, some get on taller boxes and they get up earlier. From today's presentation it looks like CSL is taking this seriously and is unlikely to be left behind.

Guidance Re-Affirmed

I guess the good news about today is that there was no bad news. Guidance is intact, and the team sounds like they have clear plans in place to drive forward on the margin improvements that are under their control.

Figure 6; Guidance Re-Affirmed

I started my career in industry working in big pharma over 30 years ago, and attended many management updates on the progress of the commercial and R&D portfolios. Today felt strangely familiar. $CSL is a global leader taking stock of where it stands, and laying out its plans to continue to grow more strongly than the industry. I'm pretty confident they will continue to succeed and was impressed by each of the presenters today. This is a business that doesn't depend on single CEO and I've no doubt that anyone of the key executives presenting today could take the ship forward if they needed to. That said, Paul McKenzie did a good job, and came across as a very competent team captain.

Disc: Held in RL and SM

Let me start by saying that I think CSL is easily one of the best companies on the ASX. I think the business will survive, and thrive, for many more years to come.

And, as with Resmed, I think any impact from Ozempic and related drugs is likely overstated.

But I do think this is (potentially) a lesson in how you can get fairly ordinary results as an investor even if you buy into a great company. In fact, over the last three years, "ordinary" is putting it mildly when you compare CSL to the wider market:

Everything is easy in hindsight, but this is what happens when a company priced for strong growth doesn't deliver. Per share earnings growth and Return on Equity in recent times haven't been great:

The reasons behind this are far from existential, of course. And it's worth noting that the consensus forecast for FY25 EPS is $11.08 -- 62% higher than FY23! But at the start of 2020 the forward PE was 43x

This was rationalised at the time by:

- Low interest rates

- Strong growth expectations

- High quality

Remember, interest rates (as defined by US 10year treasuries) were 2% and heading lower in early 2020. Things, as we now know, turned out differently. Lower for longer just didn't turn out to be the case...

Likewise, COVID impacted collections and margins, so the growth wasn't as strong as was initially expected.

My point is that at a PE of 42x, there was very little room for error. No one could have predicted covid or what global interest rates were going to do, but the company itself was telling investors in 2020 that they expected 2-7% EPS growth -- which is nothing to sneeze at for $120b company (and they actually beat that guidance!). But a PE of 42x?

This was always my issue. Yes, i'll hasten to add that high quality companies deserve a premium. It's not sensible to expect CSL to trade at a PE of (say) 15. But you are always going to sail into the wind at those kind of multiples -- unless you can realistically expect super strong growth.

Put it this way, to overcome a PE compression of 43 to 35 (and remembering that a PE of 35x aint exactly low!), EPS needs to grow at about 19% just to keep the share price steady.

Anyway, that was then and this is now. And now we (still) have a super high quality company, whose earnings are expected to grow strongly but the PE is now on a forward PE of 25

NOW things are getting interesting!

Thank god the market is anything but rational.

Top sellers on the register including State Street who lends out shares for shorts and has massive holding.

At 258, CSL is now below the capital raise price for the Vifor takeover. Falling DXY doesn't help.

On the other hand, brokers still putting in high price targets of $300+.

Recently we built up a large sum of cash in our IRL portfolios due to the Blundy-Itaoui acquisition of Best & Less (which has almost reached compulsory acquisition stage now, 90% of ownership).

Looking for somewhere to park the cash, I chose to invest in CSL shares. CSL is now in the Blue Chip dog house, closing at a 12 month low of $266.90. The share price has been going sideways for 3 1/2 years. I thought this might be a reasonably safe place to park a lot of cash with a 12 month horizon in mind. Hopefully I can still extract a bit of cash along the way (if needed) by selling a few shares.

Macquarie thinks CSL is a safe haven according to this article in the AFR from the 19th June - Macquarie’s seven stock picks to ride out weaker earnings - see excerpt below:

Safe havens

“Its advice is to stay defensive, even in the face of the recent downgrades from safe havens such as CSL, Amcor and ASX.

Macquarie’s analysis suggests (perhaps unsurprisingly) that cyclical stocks deliver the most earnings downgrades when forward orders fall and the economy slows. Media, discretionary retail, financial services, insurance and banks all typically experience double-digit falls in EPS when the economy enters a downturn phase.

On the other hand, sectors such as health, telecommunications, consumer staples and utilities experience either earnings upgrades or below-average downgrades.”

Since this article was published on the 19 June, CSL has fallen a further 6 per cent, from $284.44 to $266.90. So NOT so safe in the short term. It might fall further yet! The chartists might be suggesting you to get out of CSL now and buy back in when the share price goes above $320? (That never makes much sense to me).

I am reasonably happy with the guidance for 2024 (NAPTA up 13% to 18% on the market update on 14th June) and they haven’t hit their straps yet with the Vifor acquisition.

Most Brokers think there might be some upside to CSL according to the commentary by Bronwyn Allen on The Motley Fool yesterday:

“Macquarie has an outperform rating on CSL shares with a $326 price target.”

“Morgans believes CSL shares are “poised to break out this year“.

The broker has an add rating and a $323 share price target for CSL.

Morgans says:

A key portfolio holding and key sector pick, we believe CSL is poised to break-out this year, a COVID exit trade, offering double-digit recovery in earnings growth as plasma collections increase, new products get approved and influenza vaccine uptake increases around ongoing concerns about respiratory viruses, with shares offering good value trading around its long-term forward multiple of ~30x.”

“The most bullish of the bunch is Citi. It has a buy rating and a 12-month price target of $340. This implies a 27% potential upside on the stock.

This actually represents a cut in Citi’s share price target following CSL’s recent update, which revealed currency headwinds for the company, given it reports its earnings in US dollars.

Citi was previously tipping $350 per share by the end of FY24.

There is still the threat of a US recessionin FY24, which of course, isn’t good for US shares or ASX shares.

But Morgan Stanley points out that US healthcare stocks have outperformed the market by an average of 13% during the past four recessions.”

The consensus share price target from 18 analysts on Simply Wall Street data is $324, which represents an upside of 21%.

Now all the analysts could be wrong. CSL is a complex global roll-up. I’m not even going to attempt to value it given there are hundreds of others who are more skilled than me already doing just that. Most think CSL is worth more than it is selling for now, and I don’t think it is going broke any time soon. So I think it might be a reasonably safe place to park a lot of cash for 12 months or so.