Coming up to the release of Playsides full year results I thought it would be worth starting to track the titles in production again. As Playside moves into larger titles with larger production budgets, managing the production timeline will be an important factor on the cost side.

Playside released their financials this morning. Some impressive numbers showing the growing opportunity. How did the market respond? Dropped down to 55-55.5c in the first 30min before rebounding.

Overview • We are the largest games development studio in Australia • 330 staff • ~260 staff working from three offices (two in Melbourne, one on the Gold Coast) • Remaining staff working remotely across Australia, NZ and the UK • 240+ artists, engineers and designers • Single-digit attrition rate • Very small executive/management layer • Almost all of our staff are actively contributing to the development of games • Average management (GM level+) tenure is over six years • A$360m market cap • Majority-owned by three co-founders (49%) and staff (~5

H1 Review (Trying to get this out before the Q3 update)

The Good

- QoQ revenue growth of 34% to $20.7m and $36.2m for the half. Annualised out to $72.4m which is above the increased guidance range of $60m-65m. Original IP increased 68% QoQ to 11.1m. This is likely going to be lower in future quarters based on the FY24 guidance.

- Quarterly EBITDA of $8.0m which is ~39% of revenue. Guidance for FY24 is $11-$13m on $60m which works out at ~ 20% of revenue.

- Even though staff expenses have increased, overall they have decreased as an % of overall revenue.

- Increase in cash position to$38.3m which is allowing playside to take on larger projects like the WB IP deal.

- Playside Publishing now has three titles in the works with the first scheduled for release this FY

The Not So Good

- Both Age of Darkness and Beanland appear to be on limited resources to reach a final release, with no target dates for either in the recent updates. This has been discussed in other straws, but so far, Playside has not had a commercially successful PC release and has relied heavily on DWTD franchise.

- Kill Knight release trailer meant to be released in Feb. Still no updates.

Watch Status:

Valuation Status:

Increase to bull case. Valuation upgrade.

What To Watch

- New mobile title coming out currently in early release - Wedding Planner - Match 3 Title (Target 4-6 Titles per year)

- Warner Bros IP to be announced in Q4

- Thrive - HLTC - Release target Q4 (Publishing)

- Dynasty of the Sands - Release target H1FY25 (Publishing)

- Project Phoenix announced as Kill Knight - Release targeted for H1FY25

- DWTD Netflix Title - Dumb Ways To Survive

https://www.youtube.com/watch?v=E4cT_PRRDRo

- DWTD PC / Console title - CY25

- Mouse - CY25 (Publishing)

- Updates on Beanland and Age of Darkness

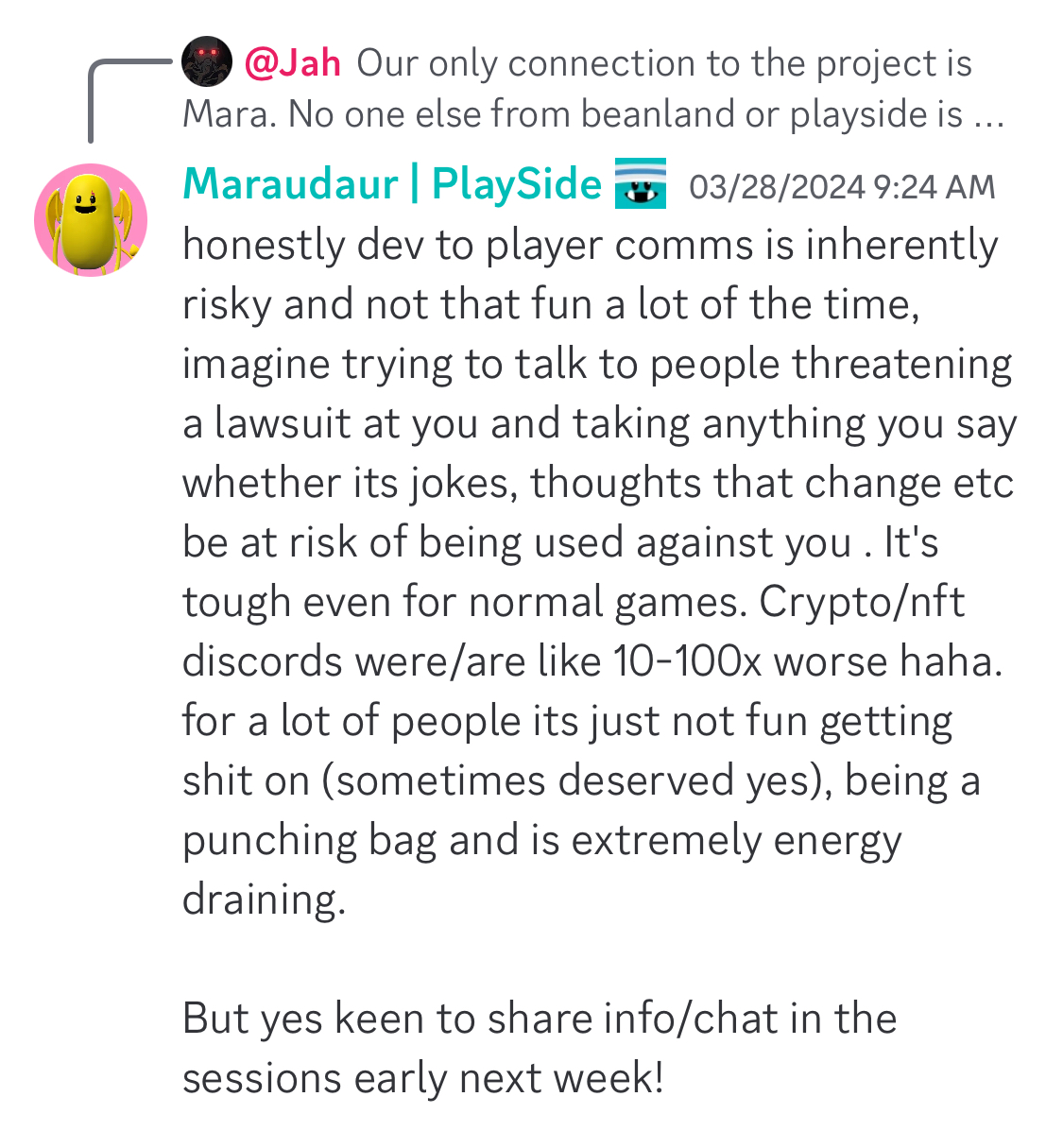

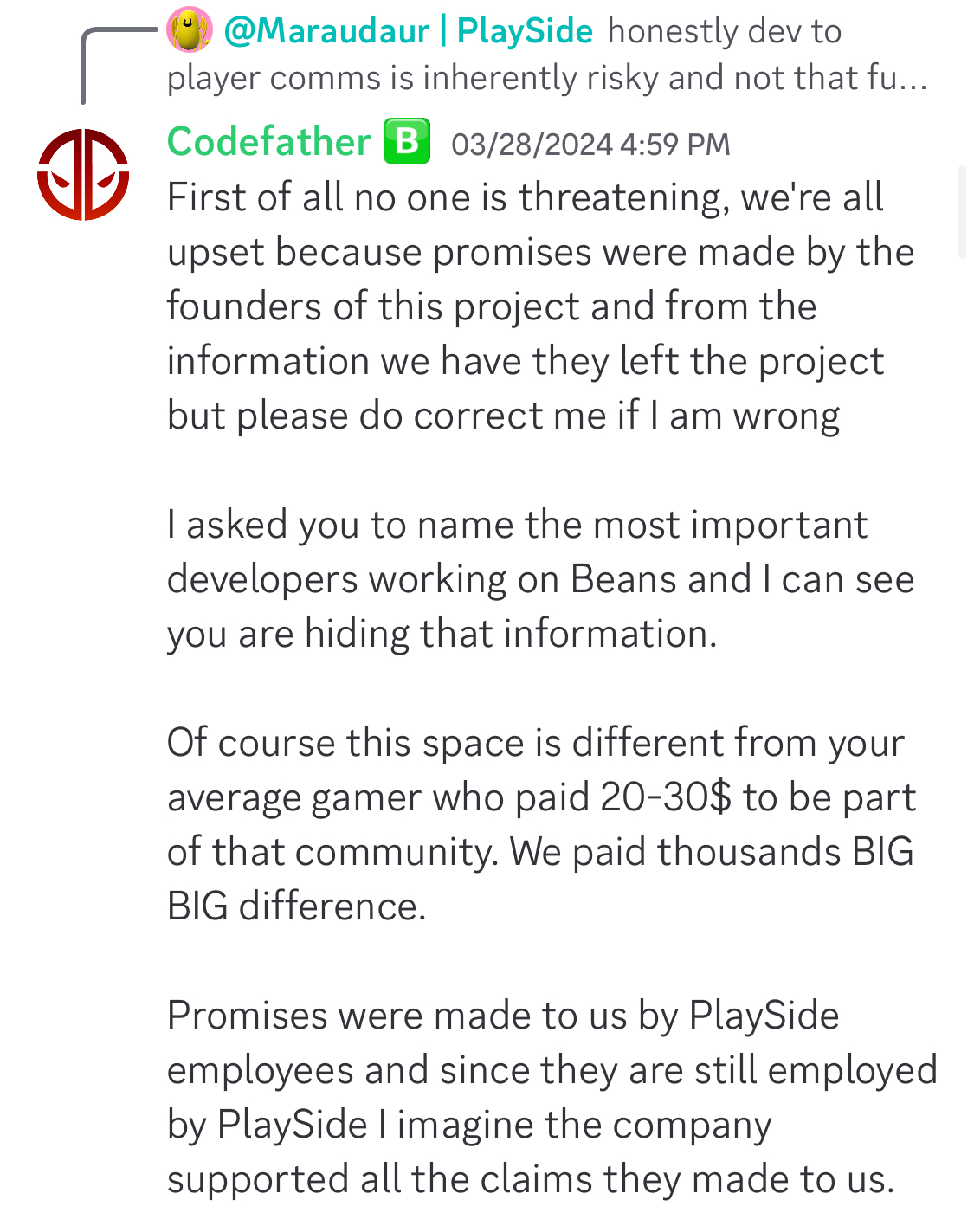

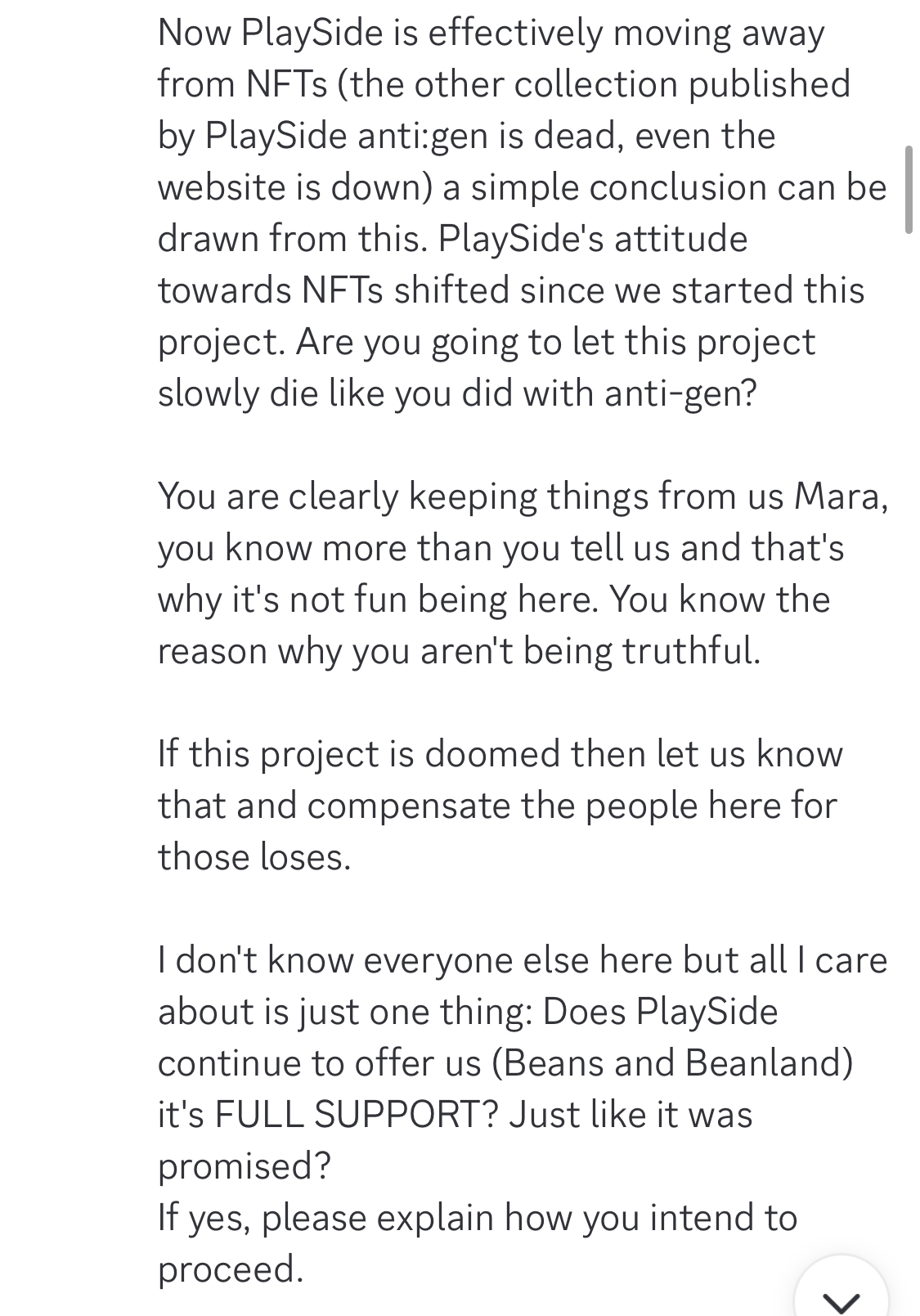

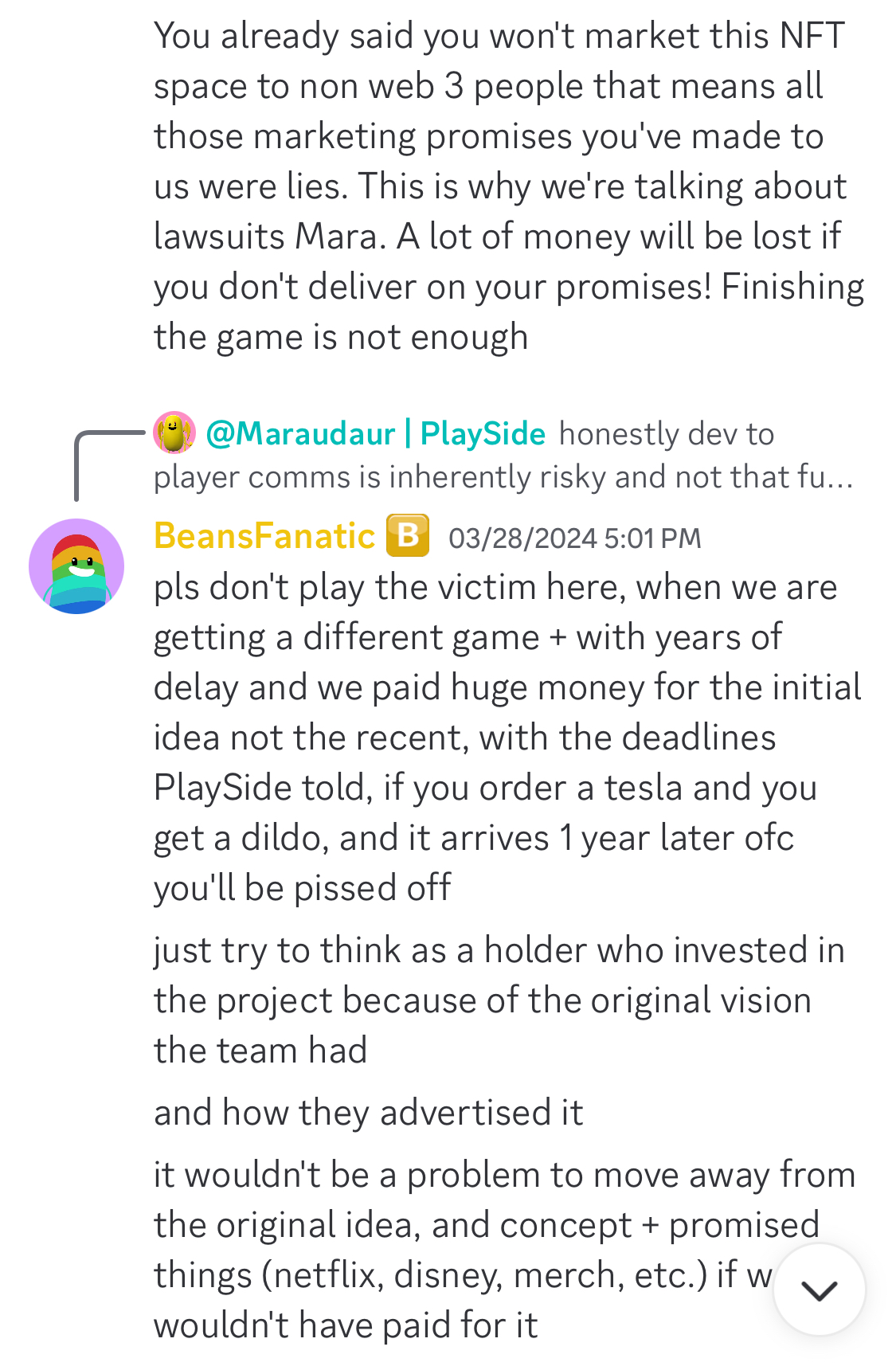

There’s been quite a bit of negative sentiment on the Beanland discord channel recently and rightly so after the long delays and constant changes to the development road map.

Whilst it is unlikely to have any major impact to the company overall, it isn’t a great look for a listed company to make a cash grab and then effectively deliver nothing to those that backed the project as they weren’t small amounts of money for the bean NFTs.

It also leads into another risk I see with Playside leading into their big IP console titles, which is their ability to close out projects in announced timeframes. This is likely due to their WFH contracts taking precedence over their own titles at this stage of the company growth, but Age of Darkness has been having similar issues in reaching final release.

Small exchange from discord below:

The Good

- QoQ revenue growth of 22% to $15.5m. Annualised this is above the $50-$55m revenue guidance provided at the end of FY23. Revenue growth was strongest in the original IP division, with a new record quarter of $6.6m. This was just shy of my last quarters estimate.

- Original IP revenue increase is likely driven by the milestone payments for the DWTD Netflix and Meta titles as following the mobile downloads there hasn’t been any significant changes across the catalogue.

- Staff costs look to be levelling out from the recent growth phase. If playside can continue to generate growing IP revenues, this is where operating leverage will come into play, otherwise further staff growth may be required to continue to grow the WFH revenue streams.

- Only slight increases in advertising expenses and still significantly down as a proportion of IP revenues.

- Cash position remains strong at $31.7m

The Not So Good

- Age of Darkness release date still TBC. It looks like this is waiting for multiplayer to be locked down, however updates from the Playside team in the Discord channel indicate that this has been a challenge. The longer this is in pre-release, the more development costs need to be recouped.

What Status:

What To Watch

- Expect Q2 to be cash flow and EBITDA positive. Track EBITDA margin for future valuation estimates.

- New deal announcements from recent games conferences. As @Rocket6 has stated, this may lead into the AAA title announcement and start to show up as increased investing cashflows.

- Original IP revenue lumpiness. Given the milestone payments for the DTWD title development, these have the potential to create lumpy IP revenues throughout FY24 until the titles are released.

- Pipeline Targets

- Next release - Beanland (Q2FY24). I don’t expect any significant revenue contributions from beanland given it will be free-to-play. There is a very small chance that it could spark some interest in the Beans NFTs again. I don't really attribute any value to the Web 3.0 segment of the business.

NFT Sales since launch (Volume & Price)

- Project Phoenix title announcement.

- Potential increase in capitalised development costs

- Third publishing title announcement

- New mobile title

Market not that impressed with Playside's results. They seem ok to me:

- Revenue up 90% (ex NFT sale)

- EBITDA and Cash flow positive in second half

- Well funded, with $32m in cash

- Guiding for (roughly) 37% growth in revenue for FY24

Revenue growth has been pretty strong historically, as they highlight here:

Shares now on a P/S of about 3.5x

Let's see what Gerry says later today when we catch up with him.

The Good

- Record quarterly revenue of $12.7m, demonstrating ongoing growth especially in the WFH business. Original IP revenues continue to remain strong, likely driven by the DWTD IP.

- Another cash flow positive quarter, again driven by low advertising revenue. I thought that this would have increased this quarter, however it has moved in the other direction. I still don’t think this level of expenditure can be maintained, however it is a positive indication that Playside isn’t having to resort to buying revenue.

- Dumb Ways To Die IP continues to drive business for Playside with a title for the Meta Quest in development. This title includes development fees and ongoing net revenue share. Both the Netflix and Meta deals include licensing fees to be paid out during development. Mobile downloads have also remained high from the peak.

- $50m to $55m revenue guidance provided for FY24 which is at least a 30% increase on the $38.4m for FY23. This shows confidence from management

- Strong cash position of $32.2m. With the company moving into consistent positive cashflow territory this leaves a very strong capital position for future business development and larger title development budgets.

The Not So Good

- Staff costs continue to rise. This is to be expected to be able to service the increased WFH contracts as long as staff to revenue ratio doesn’t increase beyond historical levels

- World Boss' full release at the end of June didn’t do anything to boost the player numbers. At this point in time it would be reasonable to assume that so far World Boss has been commercially unsuccessful.

- Mobile titles (ex DWTD) downloads on the decline

What Status: Positive

What To Watch

- How the gaming tax offset is reported. I’m not sure how the rebate is handled by the ATO but potentially a substantial payment in Q1FY24? Are WFH expenses counted within the rebate?

- Based on the guidance numbers provided from the vantage point conference slides can expect Q1 WFH revenue to stay within the $7m to $8m range

- AoD release date and ongoing downloads

- Dynasty of the Sands updates and progress

- News on new PC / Console title - Project Phoenix

- New mobile titles planned in FY24. The first of these to come out is Dumb Ways To Climb. Currently ranked number 64 in Action on the app store. Once again this is a re-skin of other similar games on the market, but its probably a good time to be cashing in on the DWTD IP

This one slipped past me yesterday -- Meta (Facebook parent) has engaged Playside to develop a VR title for its Quest device, based on the Dumb Ways To Die (DWTD) IP.

Playside will get a license fee as well as periodic development payments. They also get a share of net revenues in perpetuity.

They expect launch will take 18 months.

As a reminder, they bought the rights for DWTD for just $2.25m in 2021. They already made $9m just from NFT sales!! (yeah, a terrible "investment" for those that bought them, but it was great for PLY). Anyway, what a great purchase that's turned out to be.

This news has led Playside to guide for FY24 revenue of $50-55m. They recently told investors to expect $35m in revenue for FY23.

The top line growth has really been remarkable:

Also worth noting they have $30m in cash and were cash flow positive in the March quarter.

Yes, shares are on something like 4x sales. But maybe that's not so high given the growth and scalability of the business.

See full announcement here

Article from ABC News today talking about the games industry in Australia and the rebates available from governments to promote the industry and new impact of the new Digital Games Tax Offset that was effective from 1 July 2022.

Source: ABC news

So far this year, Playside have spent $16.4m on staff, and will likely land somewhere in the $22m to $23m range for the full year

Based on the legislation expenditure up to $67m is claimable, so Playside still has quite a large window of growth to be eligible for these rebates.

Source: ATO

What I did find valuable is this comment here about exchange rate risks for the WFH business, which although fairly obvious, I hadn't considered before. Although Playside isn't owned by a US company, the cost effectiveness of outsourcing is still impacted.

Playside have added a new mobile title to their catalogue this month. Find It: Scavenger Hunt which is free to play so will rely on the normal model of advertising and in game purchases. The game itself is pretty polished in the artwork and seems like a relaxing time filler.

But wait, what's that, this game is basically identical to many others in the store already all using some combination of Find and Scavenger in the title or description.

This is one of the main areas I'm not sure what to think of Playside's business model. I know Gerry has talked in the past of using data better than competitors to optimise their traffic and conversions, but without knowing the development and ongoing support costs of a title like this, its hard to see where the value is in competing is a crowded space like this. For me it also detracts from the image of Playside as a studio.

I will add this to my download tracking with the others in the catalogue, to try get an indication of how this performs in comparison to their other titles

World Boss full release date has been announced:

As World Boss is a free title, revenue boosts for Q1FY24 will need to come from in game purchases. There will be a new battle pass and I imagine some new content packs at release, but they will only matter if people are playing the game and currently regular numbers are very low. There will be a new map and sounds like new game modes, so that may be more enticing to new players on release.

Based on World Boss being release just in time for Q1 I think we will see Age of Darkness getting its full release around Q2FY24

Good news this morning: Playside has announced that Rocket Flair Studios’ (RFS) Dynasty of the Sands is the first title to be signed to its publishing division.

The game is an Ancient Egypt-inspired survival city builder, teaser trailer here.

Playside will provide RFS with development advances relevant to agreed milestones, consistent with industry benchmark requirements for bringing the game to launch. Playside will be responsible for publishing and marketing, and will pay RFS a share of net revenue from the sale of the game as part of the agreement.

Playside has indicated it cannot predict likely revenues at this stage. This slide from H1 FY23 provides some clues around potential performance for indie games:

It is difficult to make forecasts at this stage, but it is obviously good news for the division to have signed its first deal. Should Playside gain traction with its publishing division, there is real potential of this one day being the largest revenue contributor for the company.

The Good

- Record Original IP (OIP) revenue of $5m, which exceeded my forecasts for the quarter. This was largely driven by the DWTD games, which management said provided an extra $1.9m for the quarter. The increased revenue shows the power of viral marketing across social media networks and Playside did well to try to maximise engagement across these channels. The DWTD IP continues to bear fruit for Playside, having acquired the IP for $2.25m.

- Cash flow positive quarter. This was largely driven by the increased original IP revenue, which was recorded off a lower advertising requirement. How much Playside can maintain this in the future is uncertain, but I expect higher advertising cost ratios going forward.

- 30 Month WFH hire contract signed with Skydance. Whilst the value of this contract hasn’t been announced, it shows that Playside is continuing to keep a solid stream of contracts in the pipeline. Given WFH still makes up a significant portion of revenue, to maintain positive cash flow, the WFH deal pipeline needs to continue as staff costs continue to rise to meet the resourcing requirements.

- Further indications that the company is progressing through the transition to larger titles with a new indie game to be announced in coming quarters.

The Not So Good

- Total revenue slightly down on the previous quarter at $9.3m vs $10m. This was largely driven by a decrease in work for hire revenue, but management have highlighted that these contracts are based on milestones so some lumpiness is to be expected going forward.

What To Watch

- Based on the guidance numbers can expect Q4 revenues at a similar level ($9 - $10m) with OIP ~ $3.5m -$4m & WFH $5.5m to $6m.

- DWTD 4 coming out in May. This release may just miss the TikTok spike, but if the game is good and engaging, it will start from a strong position.

- No updates on AoD & World Boss, these are looking likely for full releases in FY24 which will help contribute to future revenue growth. Other contributors to monitor:

- Meta Mixed Reality - Revenue Share

- Beanland Alpha/Beta release & impact on NFTs

- Publishing division first game

- Based on the success of the DWTD IP the company may be on the lookout for other similar opportunities where they can own IP rights rather than licence. This wasn’t flagged but I can imagine that management have considered it given the success. This could be a risky use of capital.

Games Update

Download stats are out for March and it looks like there has been a general decline in most titles except for the DWTD TikTok boost. Based on these numbers and the forecast of additional revenue from DWTD I expect the original IP numbers to be marginally better than Q2, which may bump up to an new all time high for original IP (Current is $3.28m in Q2FY22)

Looking forward into Q4 there is an opportunity for the revenue increase to continue with a few key events:

- Legally Blonde and Godfather have recently both just had significant updates, which means they may start to get another marketing push. This will be seen in a change in download trends

- DWTD4 is scheduled for global release on May 2nd which may catch the end of interest TikTok trend

- Beanland is scheduled for alpha release in May progressing for to open beta in July

- The beans NFT are starting to get more attention as the beanland release approaches

- Age of Darkness full release is getting close. As a full price game, the initial release sales should also provide a nice bump to original IP revenue.

- Worldboss reviews continue to improve as further updates are released. No indication yet for date of the full release.

@RobW has already touched on this one, but I am also reassured that the team at Playside are making the right calls with business strategy. For me, although the bottom line numbers for the half weren’t great and the outlook for weaker original IP revenue for the remainder of FY23 is still in place, this half was about the longer term direction that the company wants to head in.

Mobile titles still remain a focus for Playside and revenue from the catalogue of titles is becoming more diversified which is a positive. What I didn’t expect to see was that Legally Blonde was the best selling mobile title, which aligns with the sensor tower revenue data. (This may be based on in-game purchases and other games generated more, but through advertising?)

Although there has been some success with the new mobile titles, Gerry did confirm my thoughts that they are looking toward larger titles in the future.

In terms of the titles that were written down, it looks to be the Anti Gen NFT project, Pillage Party and DWTD titles. Gerry’s reasoning for this direction was sound.

The Work For Hire business looks to remain at consistent levels for some time and the deal structures are improving in both size and revenue share arrangements. The fact that Playside can pitch ideas, get paid for developing and also get to share in revenue demonstrates the relationships they are forming.

For the publishing division, looking to sign something this calendar year, and starting off small and low risk in terms of resource requirements.

Side Notes:

Sounds like World Boss might be taken out the back of the shed if the full release isn’t substantially better than the soft release (in a few months). Referred to as a brand building exercise. Without substantial resources I don’t see the game improving.

I may have been a bit harsh on the Legally Blonde and Godfather downloads. It sounds like the marketing on these titles has been scaled back while they improve features (They still have to essentially buy downloads though)

@Rocket6 posted about DWTD going viral. The original IP revenue will get a nice boost this quarter with a conservative forecast of $800k coming from DWTD alone.

World Boss has now been released on steam for Early Access and so far the reaction from players hasn’t been great with negative reviews far outweighing the positive.

The biggest detractors so far are the performance issues and the lobby issues on launch day which the team were quick to address but it definitely hurt first impressions.

This game was meant to be one of Playsides marquee titles so I will definitely be watching reviews and so far the poor market reception is a strong signal to review my thesis and holding

Following on from @RobW and @Rocket6 posts I was going to wait until the end of the quarter to put this together but wanted to add my thoughts to their posts. Below is a table showing the status of the targeted release schedule from previous company announcements. Green is full release, blue is a soft release.

First up the Mobile Titles

Legally Blonde

The Legally Blonde game was released across 100 countries at the start of the quarter. Tick. The game itself is a pretty basic colour match puzzle game with a legally blonde “story” overlay. Progress through the game is incentivised by requiring levels to be completed to progress through the story and earn rewards to customise your character. Customisation and level power ups can be purchased to fast track progress.

In August the game started to get a bit of traction with an estimated 160k downloads and $100k in revenue for the month.

Mobile game download and revenue statistics from Sensor Tower https://app.sensortower.com/

Godfather

Next up is the Godfather game which is still in early release and currently only available in Australia, Great Britain, Canada and the Philippines. The game is an “idle” style which involves upgrading items to generate more money, wait a while then upgrade them further once you have accumulated the required amount, the game in general nudges the user to speed up the upgrade cycle with purchases. There is some Godfather flavour to the game but it really is superficial with some basic dialogue and quests. The level layouts and artwork is generally well done, but that's as far as the game goes. Reviews on the game have been mixed so far, mostly down to bugs that are still being worked out, but to me there isn’t a lot of “game” there and I feel like it is a missed opportunity with some good IP.

DWTD

DWTD: Dumb Choices is out as a very early release and so far early reviews have not been kind. Currently it’s not available in the appstore to try out. Screenshot is from Playside promotional material

The other DWTD title is a sleep assistance / meditation app for kids. Dumb Ways to Sleep. I gave this one a download and listened to a few of the tracks. It looks like the team has gone to some effort to create some decent content here and the app itself is pretty polished in regards to the UI and artwork. Playside have partnered with Peaceful Kids, a mindfulness and positive psychology program when developing the app. The problem I see is the price point. $15 /month in a very crowded market place.

Idle Recycle

Idle recycle is another idle game. This time about recycling! Collect cash, upgrade your facility, repeat. If this game looks familiar, it’s because it is identical to the previous game Idle Area 51. In previous updates Playside said they had developed a toolkit which allowed for the fast development of new titles. It appears that the toolkit is just changing the skin of the game and changing a few lines of text. Other than that, some of the initial reviews look to be positive.

Dino Warfare

On toolkits, the other toolkit Playside have developed is WARKit which looks to also be getting a few reskins. Dinosaurs this quarter, fantasy beasts in Q2. Once again there aren’t any new developments in this iteration of the Warfare series. There are dinosaurs though.

For those who are unfamiliar with the warfare titles, you start with a single unit and earn coins after each successful battle. Those coins are then used to run a lucky dip on a new unit, which you can then merge to upgrade, rinse and repeat against progressively larger and harder armies. Both armies are controlled by AI so there isn’t any skill involved in the game. I was going to say that the difficulty level doesn’t even force you to watch ads to progress, but I did hit a wall at Mega Iguanodon below.

The previous warfare titles have been successful and I can’t see why this one will be any different as I can see the dinosaur theme being attractive to players. So far there isn’t much data to be able to determine how this title is heading, however there should be some better metrics available after the month’s end. (For this title and the other recent releases). These will be worth tracking month to month.

On pricing of the mobile titles in game content in general, the price of items in the store are downright crazy. $100+ for some gems (insert other object) to get some more items / speed up the game?! This was always one area where I was hesitant in investing in Playside due to the predatory nature of the in game currencies in mobile gaming. I will definitely be reviewing my holding in the company after seeing the cost of items in Playsides stores.

PC Titles

Age of Darkness

Age of Darkness is now coming up close to a year in Early Access. In the Annual Results summary it was advised that the release will be pushed into H2FY23 to continue to develop the campaign and multiplayer modes. This is the release I am most interested in as it is the first of the real games that Playside have in the development pipeline. AoD continues to get downloads on the steam store, however any meaningful revenue won’t be generated from the game until it is a full working title. I’m still yet to play AoD as I was hoping to wait for the full title, but might have to give the early access a spin. Reviews on steam continue to indicate good things with 82.98% positive out of 4474 reviews.

Some recent gameplay footage below.

https://www.youtube.com/watch?v=7AjrLVBpWfM

World Boss

World Boss was the next PC game that was scheduled for an early access release this quarter. It looks like it may miss the window, with SteamDB recently showing that it could be up for a 20 October 22 release. Currently it is in closed Beta testing, with some streamers releasing gameplay footage. It's hard to get a read on how the game is received in the discord channel as there is so much other general chat room noise.

https://www.youtube.com/watch?v=zQFYwAehVYo

Game website:

The game looks like it could be a fun straight forward FPS. Do I think it has what it takes to get a cult following? Not at this point, but as @Rocket6said promotion is where the streamer partners will get to earn their keep

.

.

@Hands s posted in a straw a year ago that at the time based on the game catalogue, Playside did not have a future, currently I think the truth of that statement is very dependent on the success of these bigger PC titles. Mighty Kingdom is cautionary tale of what happens when IP fails to hit the mark. Particularly with the time and resources required.

The next several months are going to be telling for Playside, whether they can continue their growth as a studio in its own right or end up functioning as a labour hire for the big studios that reskins some mobile games every few months.

Thanks @RobW. This was the reminder I needed to do some DD on World Boss. With early access expected to occur in Q2 FY23, it is probably a good time to open up some dialogue on Strawman.

First things first, World Boss is a collaboration with influencers LazarBeam and Fresh. Who are they?

LazarBeam

Lannan “LazarBeam” Eacott is an Australian YouTuber, who rose to fame at the height of Fortnite’s popularity boom in 2018. By 2019, Lazar had hit 10m subscribers and was the third-most-subscribed Fortnite content creator on YouTube.

He still streamed Fortnite separately on Twitch until Jan 2020, when he signed an exclusivity deal with YouTube. He currently has over 20m subscribers on this platform, with a few million on Twitter.

Fresh

Harley ‘Fresh’ is an Australian Twitch streamer and YouTube celebrity – and like Lazar, he is known for his Fortnite content. Fresh currently brings around 18 million followers and subscribers across his socials and his YouTube channels and has accumulated over 2.5 billion lifetime views throughout this career.

I mentioned this a few months ago – getting influencers on board can have a significant impact on the reach and subsequent revenues associated with a game. Playside has done one better here: they have collaborated with two significant gaming influencers that have millions of subscribers between them and an ability to reach gaming markets across the world, with minimal (paid) advertising required.

The game

World Boss is a first-person shooter with a roguelike progression system, where players will take on 15 other players in fast-paced arena combat. The game itself looks pretty appealing, with clear similarities to Fortnite and Apex Legends, although slightly more ‘Arcadey’ based on the snippets I have seen. Like these games, World Boss looks like it has the ingredients to be addictive.

Playside is the developer and publisher (unlike AOD, which Playside developed in conjunction with Team17).

The game will be free to play, with in-app purchases offered to allow for earning rewards and unlocking cosmetic options (again, similar to Fortnite). This makes forecasting the success of the game incredibly difficult, even when we are able to provide estimates around player numbers. Essentially, successful free to play models require an ability to reach people globally, so the collaboration with two prominent YouTube personalities is really important. Finding the balance is also really important -- on one hand you want as many people playing the game as possible, and this is easier when it is free to play; but on the other hand, there is a requirement to make money and keep the lights on. Fortnite nailed this, and many games are starting to shift towards this model (eg Counter Strike, Apex Legends), so it isn't exactly new. But this also results in World Boss relying heavily on in-game purchases to pay for servers and recoup game costs -- and then split any profits between the collaboration team and Playside. But announcements already suggest the game will feature a comprehensive progressive system, with unlockable perks and weapons, customisable builds and playstyles, and a rankings leaderboard. If they are able to foster a competitive landscape where players are actively involved in trying to 'progress', often helped by in-game purchases, a free to play model could work really well.

Both Lazar and Fresh have started to market the game, requesting that followers ‘Wishlist’ the game on Steam and join the new Discord group.

For example, Fresh released a video in Jan 2022 discussing the game. It has received more than 1.3m views to date – link here. As we get closer to release, you can bet that both Lazar and Fresh will start to hammer their socials promoting the game. Additionally, post-release, Lazar (and probably Fresh) will start to stream the game. When you consider the audiences that will see what they are playing, it will peak curiosity and naturally start to draw people to the game. If it starts to gain popularity, it will attract other prominent streamers, and this is where the snowball effect can start to happen. As mentioned above, it looks like World Boss has lots of similarities with Fortnite. This is obviously the game where both Lazar and Fresh made a name for themselves. As you would expect, a good majority of their subs would be Fortnite fans and interested in watching/playing similar arena-based games like World Boss. This bodes well for the game's release.

Highlights

- Cash flow positive, with 8.5m inflows and PLY’s second quarter of cash flow positive results.

- Record quarterly revenue of 14m – up 403% on pcp and 157% on QoQ. That sort of growth requires no commentary…. bloody impressive. BEANS generated 8.4m alone – exclude this and PLY have experienced revenue growth of approximately 5.4m (vs 5.3m in Q2).

- This takes revenue to 23m for the FY thus far. This blows my initial 2022 revenue projection out of the water (20m).

- Generated a record 14.77m cash receipts from customers during the quarter, an increase of 642% pcp and 167% QoQ.

- Over 40m in cash holdings, a stronger position than when they entered the quarter – plenty to fuel future growth without having to tap shareholders on the shoulder.

- WFH agreement with Activision Blizzard, which similarly needs no introduction or commentary.

- Signed the lease for a new studio on the Gold Coast, with a planned opening of early May.

- PLY increased its workforce to 152, with a whopping 60 staff added during Q3. This includes producers, programmers, artists etc etc.

This was a cracking result, largely fuelled by PLY dipping their toes in the murky NFT waters. The business will launch additional products within the BEANS universe over the next 48 months, so that is something to keep an eye on – particularly due to this being key for PLY’s Metaverse and Web 3.0 strategy.

Original IP was again impressive, with 11m in revenue (including 8.4m from BEANS). This figure also includes Age of Darkness development revenue in addition to revenue from its mobile games’ portfolio, but they don’t reveal how much. Of note, the Age of Darkness release is planned for global launch in Q2 FY23.

Work for hire revenue from the quarter came in at 2.78m. Nothing phenomenal, but the ongoing validation here – in addition to steady revenue inflows – provide PLY with brand benefits and cash to keep the lights on while they pursue original IP opportunities.

The business provided updates for their original IP titles in development. I won’t repeat them here, but there are 7 titles (not including Age of Darkness which I discuss above). The majority are planned for launch in early FY23.

The business will split original IP into three divisions – mobile, PC/console and Metaverse/Web 3.0 – with GMs appointed to each. This sounds pragmatic and will help the business align staff with relevant skills to the right division. The business has also hired a GM for WFH – lets hope this individual knows how to talk the talk because you would think the role is primarily outwards facing -- dealing with AAA developers/publishers.

Last thing from me – this quarter's cash flow statement reflects how efficiently gaming companies can generate cash when original IP titles start to gain success:

When you compare this with PLY’s Q2 results, you will see that there is almost no difference to the business’ marketing, staff and corporate costs – so revenue earned will shift straight to PLY’s bottom line – an excellent example of operating leverage.

Disc: held

It looks like Playside are learning the hard way that life in the current Web 3.0 is still very much the Wild West after having their discord channel hacked and potential comprise of holders wallets.

This will be interesting to see how they navigate through this and how it impacts the current Beans NFT project

09-Feb-2022: Canaccord Genuity: BEANS launch drives ~40% revenue upgrade [BUY, PT raised from $1.10 to $1.30]

10-Feb-2022: Canaccord Genuity: A blizzard of activity [BUY, PT: $1.30]

Author: Benn Skender | Analyst | Canaccord Genuity (Australia) Ltd. | [email protected] | +61 3 8688 9105

Twitter: Benn Skender (@bennskender) / Twitter

I know @shivrak will have some input on this but thought I would get in early.

It looks like there has been a bit of funny business going on with the Beans NFTs. Recently on the discord channel the team has announced that the NFTs that were to be burned have now been minted and released to the market impacting the value of the secondary NFT market.

https://opensea.io/collection/beans-dumb-ways-to-die

So now the company has taken the initiative to keep community sentiment in the project by buying back NFTs to raise the price.

This could be a costly exercise which will impact the total proceeds from the project announced today, given they are going to be buying back at a premium to the minting price. Currently there are 396 listed NFTs below 0.6 ETH. There will likely be an on market announcement tomorrow to follow on from this. Interesting times.

Playside are jumping into the NFT space under the Dumb Ways To Die franchise with the announcement of Beans NFTs under the Playside and DWTD twitter accounts. I really hope that Playside incorporates some utility into the NFT, as it seems that every man and his dog are creating a NFT for something these days. Based on the roadmap on the project website, it looks like there will be an upcoming AR Title that provides utility for your “Bean” within the game.

Project website www.beansnfts.io

Currently scheduled for minting in February 2022, this is likely to contribute to Q3 revenues, however there are no details as yet on qty or minting costs.

The DWTD franchise lends itself well to the current NFT mania with its bright colourful characters that also carry with them a sense of nostalgia. If the discord channel is an indication then this project will likely be a success as it has over 17,400 members since creation on January 6, although for myself as a holder of Playside, I really hope this is more than just a cash grab.

In the FY22 Roadmap released in the Q4FY21 update, Playside had indicated that a multiplayer update would be released in Q2FY22 for Animal Warfare which has been their most successful mobile title to date.

Multiplayer was added in Version 2.9 in December 2021.Multiplayer adds a more challenging element to the game as it is fairly easy and repetitive in solo mode. This update should add some extra longevity for players and continue to generate revenue from the title for the rest of FY22.

The update itself isn’t major, however is a positive as an indicator of Playside hitting release targets. If the PVP is successful, it could also be incorporated into the other warfare titles.

As per Playside's Instagram page, they're opening a new studio on the Gold Coast.

https://www.instagram.com/p/CWXugvpPQxF/?utm_medium=share_sheet

So far the intial release of Age of Darkness seems to be solid. Currently showing up on the featured banner and top sellers list on Steam and has ~90% Positive reviews at the time of writing. Playside are also already proactively communicating upcoming updates to the community in the development roadmap which seem to address most of the issues raised in negative reviews. However they haven't provided a timeline around each of the milestones.

For how well the game sells only time will tell, but devs and Team17 seem to be putting it in the hands of streamers with some pretty big followings (eg. SplatterCat - 668k subscribers)

Steamdb which shows download estimates based on the number of reviews and other sources and is currently showing a range of 6k - 18k. I will come back to this site and compare to Q2 quarterly if they release some figures to try gauge the accuracy for estimating revenue from the game.

The other factor for estimating revenue is the split. If they split evenly with Team 17 it would look something like this.

Valve (30%) Team17 (35%?) Playside (35%?)

Which at the current price of $28.75 equates to about $10 to download.

Now I just need to get a better computer so I can actually play the game.