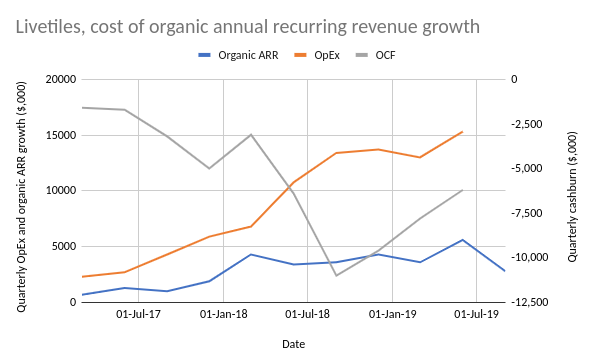

Last week, Livetiles (ASX:LVT) released its most recent quarterly update. In contrast to the June update, where annual recurring revenue (ARR) increased from $34.5 to $40.1 million, this update was undoubtedly underwhelming, recording just a $2.8 million increase – the lowest increase since December 2017 before acquiring Wizdom.

Shares are now trading at less than half of their all time high. Being a loss-making company means many investors were attracted to the growth rate in revenues and ARR, which now appears to be less of a compelling argument. Traditionally, sales teams close a majority of contracts nearing deadlines for the full year and half year. But even in a traditionally slower quarter for software sales, these numbers were below consensus.

Livetiles management also worryingly flagged an increase on their projected operating expenditure of $15.9 million for the quarter, in part due to the costs of the recent capital raising.

A saving grace in the short term may be the combination of a confirmed $3.8 million R&D government grant and the record quarterly revenue which was flagged but not disclosed – traditionally it is released in the 4C. These will hopefully result in a further improvement in quarterly cashburn which was most recently -$6.2 million.

So how does Livetiles look as a $250 million market cap company?

Livetiles targets mid to large organisations moving from traditional code heavy digital workplaces to drag and drop, customisable and machine learning oriented intranet software. They are the global leader in intranet software, and management claim a $13 billion total addressable market to which they have penetrated less than 1%. As always, especially after an underwhelming announcement, these claims must be taken with a grain of salt.

From here, ARR needs to compound at 62% annually to reach the stated target of $100 million by June 2021. After this most recent quarterly increase of just 7%, that may prove to be an ambitious goal.

Still, at today’s lows Livetiles is trading at an ARR multiple of just 5.7x. For a company which reported a 132% improvement in annual revenue last year, and continues to have expectations for ongoing strong growth (even if it is less than the stated target), the value proposition is now more attractive.

The Strawman community seems to be of the opinion that the recent drop makes Livetiles worth a closer look; ranked #8 by members, the consensus valuation remains well above the current market price.

Click below to see the full Company report.

Strawman is Australia’s premier online investment club. Join for free to access independent & actionable recommendations from proven private investors.

Disclaimer– The author may hold positions in the stocks mentioned in this publication, at the time of writing. The information contained in the publication and the links shared are general in nature and does not take into account your personal situation. You should consider whether the information is appropriate to your needs, and where appropriate, seek professional advice from a financial adviser. For errors that warrant correction please contact the editor at [email protected].

This Service provides general financial advice only, and has not taken your personal circumstances into account. Strawman Pty Ltd operates under AFSL 501223 . For more information please see our Terms of use. Please remember that share market investments can go up and down and that past performance is not necessarily indicative of future returns. Strawman Pty Ltd does not guarantee the performance of, or returns on any investment.

© 2019 Strawman Pty Ltd. All rights reserved.

| Privacy Policy | Terms of Service | Financial Services Guide |

ACN: 610 908 211 | Australian Financial Services Licence (AFSL): 501223