Consensus community valuation

Post H1FY26 results

Finally, getting round to this update. I'm impressed how fast others can make decisions and act on them!

No evidence of new product growth and rising opex. Accounts are messy with revisions and changes in reporting.

The bull case is broken and too messy for now, focusing on base case i.e. no new product revenue.

Issues with trustworthiness in management aside, the big uncertainty is the revenue growth and its quality. I think it's clearer that costs, especially product development costs, will stay at current levels or rise.

For base case, given slowing tech revenue in all regions, I have revised down revenue growth to 70m revenue in FY28 (10% from FY26). Revised opex up with product development costs likely to stay elevated. Get a 7% EBITDA margin.

As before, using EV/EBITDA of 10 I get $0.17. That's lower than 1 x Revenue.

We need to look out further than FY28 to see flex in operating leverage.

So role it forward to FY29 and we get $0.27.

Base case $0.27 (previously $0.49).

Post FY25 results

I’ve modelled out to FY28 using a scenario approach.

I have spread my scenarios across what I consider the key sensitivities. The base case reflects only what’s been demonstrated: moderate transcription and customer growth, but no contribution from new products.

In all three cases, I assume flat total revenue in FY26, but technology revenue increases to $49m with higher gross margin. The drag is Asia pacific, there's still cannibalising of service revenue to work through. Services is almost 3x tech revenue here - that's a big shortfall to make up. Coincidentally (or not), they have stated new products (Voice) won't be meaningful until H2 FY26. So in my bull case significant top-line revenue growth, what the market seems to focus on, is forecasted only in FY27 and onwards.

I'm assuming 80% of revenue is at 86% gross margin, with a consistent cost base across all scenarios.

FY28 valuation:

Result = weighted valuation of $0.67.

My interpretation = The market is not attaching value to the bull case, that optionally is free at circa $0.50.

Guess on timeline = Better odds on whether bull case should be known in H2FY26.

------------------------------------------------------------------------------------------------------------

Pre-FY25 results: I had conservative valuation of $0.46 (no scenarios).

Geez Tony and co...not what you want to see after an already difficult reporting season.

Discl: Held IRL 3.87% and in SM

AIM's downward drift on no negative news is reaching the bottom of my previously marked top-up of 0.615 to 0.655 which is a decent support/resistance zone going back to Sep 2024.

Nest support level if this breaks is 0.46 to 0.49, from when AIM announced its FY25 results back in Aug 2025.

Discl: Held IRL 4.56% and in SM

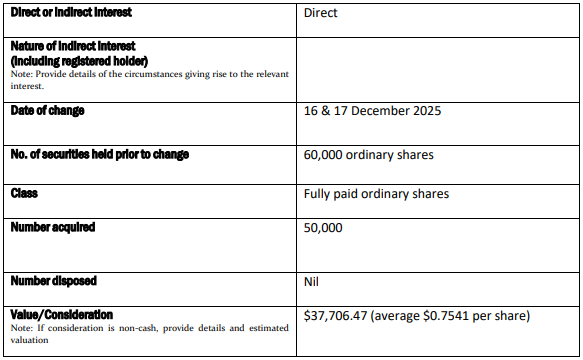

Very nice to see Brad Bender, one of the 2 high-profile-ish US-based directors AIM appointed in Oct 2024, top up his shareholding of AIM by ~83%. He added 50,000 shares to his initial 60,000 holdings from Dec 2024.

The value of $37.8k is small coin in USD, but better to see him buying than not.

Discl: Held IRL 5.16% and in SM

This came from AIM Investor Relations via email as I signed up to the AIM Investor Hub.

The spread of AIM information is a bit inconsistent right now. This email came direct. There is no announcement of this on the ASX nor on the Investor Hub itself. Tony has not posted on Linked In, but I expect him to do so shortly.

Looks like @Strawman and Tony are becoming/are best buddies!

Product & Market Webinar

Join CEO Tony Abrahams and CFO Jason Singh as they provide an overview of the Company’s current product suite alongside consolidated feedback from recent executive visits to Europe and the USA. The Company will outline how this international market feedback aligns with its existing strategy and product roadmap priorities.

The webinar will be moderated by Strawman's Andrew Page and investors are encouraged to ask questions on AIM's growth strategy and geographic expansion.

Webinar Details are as follows:

- Event: AI-Media Product & Market Update Webinar

- Date / Time: Wednesday 3 December 2025, 10AM (AEDT)

- Registration link: https://investorrelations.ai-media.tv/webinars/drLvQy-product-and-market-fit-webinar-dec-2025

The Company notes that this webinar is not a trading update. No financial performance, outlook, or guidance information will be provided, and questions will be strictly limited to product and market topics.

Ongoing demonstration of the growing momentum behind our LEXI AI captioning and translation platform

From planetariums to global media summits, broadcasters to local government, organisations worldwide are choosing AI-Media to deliver real-time accessibility and multilingual engagement, affordably, reliably, and at scale.

Recent wins highlight the versatility of our end-to-end ecosystem and why customers continue to displace legacy human-only solutions with AI-Media.

Scitech (Western Australia) – Making Live Science Truly Inclusive

Scitech, Australia’s leading hands-on science center with 300,000 visitors annually, faced a classic “impossible” captioning challenge: unscripted, fast-paced shows featuring complex astronomical terms inside a dome planetarium.

The Solution:

- LEXI Viewer deployed across the Planetarium, Chevron Science Theatre, and a fully portable mobile trolley for outreach events.

- Real-time AI captions handled terms like “Zubenelgenubi” and “Alpha Centauri” with ease.

Outcome:

What was once considered impossible is now seamless. Deaf and hard-of-hearing staff and visitors have praised the accuracy and responsiveness. Scitech is now more accessible than ever before.

“I’m impressed at how accurate and easy to use the LEXI Viewer is. This is a great step for making our venue more accessible.” – Leon, Planetarium Lead, Scitech

APOS 2025 (Bali) – Asia’s Premier Media & Entertainment Summit Goes Fully Multilingual

For the second consecutive year, Media Partners Asia selected AI-Media as the exclusive live captioning and translation partner for APOS – the region’s most influential media, telecom, and entertainment summit.

Solution:

- Large-screen English captions in the main hall

- Real-time translations into Korean, Vietnamese, Chinese, Thai, and Japanese delivered via the APOS app

- LEXI Voice AI dubbing streamed to foyer spaces and headsets

- Captioned live interviews broadcast from our on-site booth

Outcome:

550 delegates and 80+ global speakers experienced a completely inclusive, tech-forward event.

“AI-Media’s live captioning solution added a vital layer of clarity and inclusion… The live translation… further amplified access and engagement across APOS.” – Lavina Bhojwani, VP & GM, Media Partners Asia

Want to hear more about recent activity?

Discl: Held IRL 4.84% and in SM

The AIM chart is looking very interesting from a top-up perspective.

- Fell right through the 74.5c to 80c level which I thought would be decent support

- 72c is the 50% retracement level - “usually” a decent place to top up

- But better support could come at ~68c which is looking to be at the confluence of (1) support from the 1 year + uptrend line (2) the 200 Simple Moving Average and (3) ~60% retracement

- Failing which, there should be decent support at 61.5c to 65.5c

I suspect I will start nibbling at around 68c at this stage ...

Discl: Held IRL and in SM

Looks like Tony's hard sell on the AIM results to the market is paying off ... not sure what drove the 12.4% pop today, but a few things to note from the charts:

- It hit the 52 week high today at 0.95 - it was last here in Dec 2024

- Always nice to see a pop on decent volume - today's volume looks really good

Zooming out, the price is now firmly in the 90.5c to 99.0c zone - lots of history in this zone going back to 2021/2022, which it will have to digest before moving higher.

I do expect it to churn around at these levels for a bit.

But thats one hell of a journey in these 4-5 years-ish - went to hell, literally, it looks like it is moving towards the Heavens now ...

Discl: Held IRL and in SM

Another Tony Linked-In post from 3 weeks ago that popped up in my feed.

My takeaways:

- It reinforces that LEXI Voice is NOT competing with hyperscalers as they improve the accessability to personal language translation technology.

- "Consumer “magic.” Enterprise scale. Same story, different stage." - a nice summary

- Our Tony is watching all things translation like a hawk and comments on these developments to correctly position the development against AIM - I have no quarrels with this.

Preamble/Context

I've been a bit slow to commit to a valuation on SM for $AIM, despite having held it for just over a year. It is now another core holding in my RL ASX portfolio, thanks once again to the StrawPeople who got there earlier, as well as the opportunity to hear from CEO Tony in the SM Meetings. (I wasn't convinced after the first SM Meeting, but last year September's one got me over the line.)

A second reason for holding back on publishing my valuation was that, as other holders will know, if you buy into the FY29 Targets of "$150m revenue; $60m EBITDA; a billion $ company" - a message that Tony promotes with irrepressible consistency - you get such a large valuation that you'd be tempted to back up the truck ,...if you believed it.

Although I have set out some scenarios here that fall well short of Tony's vision, everything that follows is firmly anchored on the vision. And so, insofar as the vision fails to be realised, then so too the valuation will fall short. That's why I've entitled this Straw a "Bull Case".

Going through the exercise has enabled me to unpick the business and get a better understanding of the value drivers. As such (and as is the case for all my valuations) it is as much a tool to track the progress of the business over the coming years.

The good news is that there is a lot of room for the business to fall short of Tony's targets and still be a very valuable investment. Of course, it is in a very fast-moving space, and who knows what disruptions will emerge over the next 4 years!

The final reason to push myself to do this, is as part of preparing for the next SM Meeting with Tony, on 28th October.

SUMMARY of Valuation (the TLDR bit)

Method 1: FY29 P/Es of 35, 40, 45: $2.60 ($1.30 - $3.60)

Method 3: EV / EBITDA of 20, 25, 30: $2.40 ($1.30 - $3.80)

Note: Selected ratios considered conservative becaue EPS growth in FY29 typically in the range 55% - 80%. So there is every chance that if the market believes $AIM can achieve and sustain it's growth, we might well experience a Super Bull case, where a much higher P/E is offered by the market ... for a period of time.

Valuation Details

I start with Tony's FY29 target and I assume $AIM will fall well short of the goal. It is aspirational after all, and we are moving in a space where there will doubtless be innovation and competition.

However, there are some "Building Blocks" that I assume.

Building Block 1: Today's business with the human transcription service which is being shut down as we speak

Building Block 2: Tech Revenue, with an increase compoent of fast-growing ARR. The ARR has a %GM of 86%. Having looked at the trajectory to date, I assume the overall Tech Revenue will have a %GM that starts at around 80% today, and scales to 83% by FY29 - driven by the ARR component. This is hard-wired into all scenarios.

Building Block 3: A new services model, essentially a 50% Gross Margin professional services business to clients. Tony aspires to this delivering $30m in revenue by FY29. I am less ambitious, and have it contributing $5m in FY26 and adding $5m each year, as the business services a global existing and prospective client portfolio. This segement therefore gets to $20m revenue in FY29.

The Opex Base: Because we have the existing Opex Base, and can isolate the COGS of the two revenue streams, I am able to consider various scenarios for how the Opex scales over time. There are two sets of 5 scenarios.

Scenarios

I have run 10 scenarios (sensitivities, really) across two dominant group.

One group is a high revenue growth and relatively high opex growth model, where scaling the revenue entails higher costs, whether in sales and marketing effort or product development, tailoring solutions to meet client needs. In this case I consider annual Opex growth scenarios of between 6% and 12% per annum. Over the next 4 years the Tech Revenue growth is sequentially, +30%, +27%, +23% and +20%.

In the second case, more cost efficient growth is achieved as revenues are not chased so hard. Opex growth ranges between 6% and 10% per annum, achieving Tech Revenue growth sequentially of +27%, +24%, +21% and +18%.

To keep the model simple, I have applied a common D&A set of assumptions, on the basis that variations in platform development costs have been included in the Opex Scenarios, and most development is expenses.

Common Parameters

The "New" Professional Services Revenue and Gross Margins (50%) are common across Scenarios: $5m, $10, $15, and $20m over the next 4 years.

Interest Income and Cost are de minimis. Tax Rate is 30% (once profit is achieved). The discount rate is 10%.

Illustrative Revenue Profile

The figure below shows the revenue build from one scenario. A few things to get your eye in. First, FY29 hits $120m, vs. Tony's $150m aspiration. Second, we should be alert to the possibility of a significant revenue fall in FY26, as the old "Services" are switch off in December. If the market hasn't been paying attention, I wonder if we really will get one last opportunity to "back up the truck" if that happens? Particularly if the reporting of it coincides with the market being in a grumpy mood towards "growth" and "tech".

What happens in FY26 isn't really important to the valuation and I am not trying to model it - so it is not my forecast - but I will use the result to update the model!

Full Table of Scenario Inputs

Full Table of Scenario Outputs

Valuations

So When Would I Sell?

It is unlikely the market is going to offer prices that have me selling on these valuation grounds any time soon. So it is important not to anchor on these numbers as some kind of pre-ordained truth. They are just assumptions.

For me to hold, I really need to see the Tech Revenue sustaining high growth at good margins. I couldn't really care less about the "New Professional Services", nor do I mind if Tony starts to reset his $150m in FY29.

As long as Tech. Revenue is growing strongly consistent with one or more of these scenarios, then I'm likely to hold on tight, and I might even add more.

Disc: Held in RL and SM

AIM chart looks ok. Sma 50 is set to move up through the sma 200

Wed 1st Oct 25

You may recall my last post on AIM. The chats were looking good for a set up with a divergence on the 1 day chart and other indicators also showing a positive signals. Fast foward, it looks like the signals were spot on. Its not always the case though. After reading eveyones thoughts however I decided to stay out for now (and I did agree with members thought).

Its alway a dilemma though. Do you follow the charts (market sentiment on the stock) or the fundamentals (ideally both). Im always trying to refine my investment methods. I have a number of positions (15-20K) currently that are well ahead (50%+) now and plan to loadup on their next draw downs all going well . I built these position without a reasonable positive narritve on the fundamentals, purely on chart technicals. Feels great now to have snagged a couple.

Looking back now at AIM, I feel I should have built up the same kind of position their. If i had gone ahead I would have started with 5k and increased leaving w2 on the 1d chart up another 5-10k by the time it was just breaking above the 200sma on the 1d. Currently the stock is working on the larger W(i) on the 3d chart. We should then see a pull back by 50% to approx 0.73 for W(ii). So long as their is now major news to the negative, I dont think it will drop that far. Many stocks seem to be only dropping to 23.6% or 38.2% of W(i).

Anyway for now I waiting until W(i) is finished and start to see the bottom of W(ii). That one can be tricky when the market is feeling bullish on a stock. Some times I have missed it and it has exploded up and never reached my target for getting in. Oh well there's always more opportunity’s get enter I let update you om my thoughts once we start to enter that kind of area

It looks like sentiment on this stock is very promising shown by the recent moves since the bottom. Im thinking that this could be another DRO. Lets hope so

Disc: Held IRL and in SM

Attended the AIM AGM this morning. Only picked up a few newish data points from the otherwise non-event AGM this morning. Nothing to not like from my perspective.

SUNSETING OF HUMAN SERVICES

- 3 remaining customers to transition from humans to AI - UK Parliament in Oct, then Channel 9 and Channel 7 by Dec 2025, fully completing the sunseting of old legacy translation services

- New professional/consulting services will commence 1 Jan 2026, to comprise 20% of revenue going forward - customers have requested for this to help leverage the benefits from AIM technology stack - this was a nice, simple summary to end confusion around this topic, as it should have been from the start

FUTURE SALES MODEL

- Pivot to indirect sales model to enable global scaling - this is an area I would like to better understand when we get a chance to chat with Tony again as this is going to be the key distribution model going forward

FIRST PAID LEXI VOICE CUSTOMER

Similar to Playbox Neo deal, this deal shows a few of the strategic levers that Tony talks about, in play:

- Channel Partner driven, with the Partner having opportunities in the other municipalities

- 1 of 45,000 municipalities in the US

- A win in the Government/AMER quadrant in the 9 squares model

MONITORING OF AIM SERVICES

AIM has a strong focus on collecting and monitoring of operational data on translation accuracy, latency etc - while needed for auditing etc, from an investors perspective, it gives me confidence that the operational stats that AIM presents will be factual and hence, can be relied upon

COMPETITORS

Translation Technology:

- Hyper scalers who will build and deliver themselves, GoogleMeet, MS Teams, Apple Airpods etc - these are AIM’s product competitors but they are all delivered Direct to Consumer on their devices

- AIM does this translation in an open live environment, doing the translation at source to broadcast with quality control to everyone

Human Translation Competitors:

- Other competitors are the actual human translating competitors

Encoder Competitors

- Largest competitor of encoders - Enco, 20% market vs 80% AIM,

- City of Rialto unplugged Enco to plug in AIM

Not yet seen anyone who has done the orchestration, Live thus far

TONY’S LTIP

Carried with no conversation

THE DEMO

- The Lexi Voice to translate live English to Spanish speech was demonstrated - this was to show the maturity of Lexi Voice in western languages

- Then 2 AIM employees spoke Mandarin and Hindi, respectively - Lexi Text was picking up and displaying the speech into Mandarin and Hindi text almost real time. But speech translation lagged, almost on a paragraph basis. Tony said that while accuracy was to standard, the latency of the voice translation was not - this was what they were focused on addressing in FY26

I thought the Lexi Voice to Spanish was a bit of a non-event as I am a believer that it works, and it worked well.

Having done enough live demo’s myself, the choice of Mandarin and Hindi was rather bold, I thought, as the Voice translation clearly lagged. But I appreciated that boldness and openness to publicly admin it is not yet good enough and in a perverse sense, added to my confidence that they will find a way to get it down to the right level of latency. It does feel like Tony is setting the scene up for something in the Asian-language space for later with the choice of these demo’s .... time will tell what exactly!

Discl: Held IRL and in SM

There is good value monitoring Tony Abrahams' Linked In as his announcements platform.

I can't confess to clearly understand what Playbox Neo is, even after my buddy Chat spat out the info below.

While there is no indication of deal size, I think it is a really good real example of AIM's value proposition, moat, combo of Text + Recorded + Voice product strategy, sticky SAAS revenue, European regulatory tailwind, all playing out in this single deal:

- AIM technical stack inside the PlayboxNeo technical stack - assuming PlayboxNeo feeds content to those ~20,000 channels live/recorded, AIM is plugged into that direct pipe, this could well be a moat inside a moat setup - very nice!

- Combo of Lexi Text, Recorded and Voice - the holy trinity of translation!

- New logo Europe customer with 23 human employees in 2023 who just added a no-human technical service to be European regulatory compliant

- 20,000 channels globally , 120 country reach - presents a really good upselling opportunity when AIM adds more countries to its capability - technically, they should be able to turn on each country as soon as AIM is country-ready

- Which translates into Lexi Network minutes + Lexi Text + Lexi Recorded + Lexi Voice minutes.

PLAYBOX NEO DEAL

A new deal with PlayBox Neo was announced 2 days ago.

Key components included:

- ALTA 2110 IP Encoder – Supports SMPTE ST 2110 workflows, delivering same-language and translated captions with ultra-low latency.

- LEXI Text – Automated captions with broadcast-grade accuracy, powered by AI-Media’s Topic Models for speaker names, technical terminology, and brand-specific language.

- LEXI Recorded – Pre-recorded captions produced in less than half the program runtime.

- LEXI Voice – Real-time multilingual voice translation for live and on-demand content, extending reach globally.

WHO/WHAT IS PLAYBOX NEO

Products & Services

- PlayBox Neo is a company that builds broadcast / media-playout / playout automation / channel branding and streaming solutions. Key offerings include:

- Channel-in-a-Box systems, which integrate several functions needed to run a channel: playout automation (AirBox Neo), live ingest (Capture Suite), scheduling (ListBox), graphics (TitleBox Neo), etc.

- Cloud2TV: a cloud-based virtual playout / cloud playout solution enabling remote operations / flexibility

- Media Gateway: for routing, encoding & decoding, especially in IP / hybrid SDI-IP workflows

- Capture Suite: for live ingest / content acquisition.

- TitleBox Neo / graphics solutions: for interactive graphics, channel branding, overlay, etc.

- Support services: 24/7 customer support, technical maintenance, software upgrades (ASM&TS – Annual Software Maintenance & Technical Support) etc

They provide solutions in hardware, but also software, and as “hardware or as a service” / cloud models.

They serve a broad set of types of TV/branding/plublic/OTT channels: free-to-air, FAST, local channels, corporate channels, satellite, etc.

Customers/channels/reach

They report powering over 20,000 TV and branding channels worldwide.

The geographic reach is “over 120 countries”.

So their “customer base” is fairly large in terms of channel deployments, though the exact number of unique customers (companies) is much lower.

Revenue

This is where public information is more limited. I found some clues, but no reliably confirmed figure for total annual revenue.

- The company has said it had a “record year with increased revenue growth” as of 2024.

- It is described in various sources (e.g. Tracxn) as an unfunded company, meaning it has not raised external investment.

- The number of employees: about 27 employees in 2023 (according to EMIS for the Bulgarian entity).

- Company is based in Sofia, Bulgaria.

I had a go at making some SaaS valuation metric charts. Not sure where to put this, but it's relevant to AIM.

I tried using AI to scrape the data by uploading pdfs but quickly run into free usage limits. I also had issues since I wanted forecast data and non standard metrics like EBITDA.

Once I got the data though, it was easy to create the charts. Disclaimer: completely possible some of the data is wrong, but hopefully direction-ally close enough.

The first chart is backward-looking. It compares EV/LTM (Enterprise Value divided by Last Twelve Months revenue) against the Rule of 40, which I calculated as EBITDA margin plus LTM revenue growth rate.

As we know AIM is cannibalising it's own revenue for growth in higher quality technology revenue. So LTM revenue growth was -2% plus the EBITDA margin of 5% giving a rule of 40 of 3%. It looks to be valued at low EV/LTM for good reason. This is the typical kind of automated valuation something like simply wall street or similar might do.

The second chart is forward-looking. It focuses on ARR (Annual Recurring Revenue) and includes forecasts rather than historical data. This one is EV/NTM ARR against Rule of 40, which is EBITDA margin plus NTM ARR growth rate.

A portion of the technology revenue has been labelled as ARR, which they have guided for 35% growth to $23m. Adding the current EBITDA margin of 5% we get 40%, meeting the rule of 40. Since we don't include all the other revenue in this method, we get a higher EV / ARR of 5.5. I think the median EV / Rev in Australia for SaaS is somewhere around 5.

Arguably, all this is useless, since it is so broad brush and lacking nuance. ARR is not really the same, in IKE's case I actually use Exit Run Rate and it's not so reoccurring. There can also be lots of churn but covered up by the growth of new customers. In RDY case, there a ton of D&A so using EBITDA is pretty dodgy. Perhaps most importantly, it's just a point in time and short-term focused. All that said, It can be a good starting point to understand what characterises a company vs others.

I imagine this is what investment bankers do - chuck this into a slide deck, send to their boss, then spend a few more hours adding logos and changing colours, $400/hr please!

Interesting to see Salter Brothers sold down 2.505m of their 12.08m share holding recently. I would be interested to know why they sold down some of their holdings given the glowing endorsement Gregg Taylor gave to Tony's FY29 target plan in an Aus Biz interview only 10 months ago.

Discl: Held IRL and in SM

The AIM price feels like it is really in a good spot today in that it is “somewhat behaving”, chart-wise.

Bit more volume(at least through the ASX, Chi-X is another story altogether - see other thread on this) as the price tries to push through the 61.5c to 65.5c resistance area. The last time it pushed through was in mid-July 2025, but failed to stay above it, then the results kicked in. As “expected”, the price hit resistance at the 200 SMA line - almost smack bang on the line today.

So, the combo of the 200 SMA and the 61.5c resistance area is a short term hurdle to cross - does not feel like it will cross both today, but hell, it looks like it is trying, as it did last Thurs as well.

We also know some Directors are selling, possibly selling hard. The market seems to have absorbed that selling pressure quite nicely since the results. Tony looks to have done a good job with the fundie road show because whatever the Directors give, the pumped up fundies appear to be taking, it would seem. This absorbing of selling pressure is very reassuring for me as the price is holding strong/pushing upwards, which should mean more believers are jumping onboard.

When the selling eventually abates, and assuming no other drama’s, the price looks to be in a good position to cross and stay above 65.5c, which should be a nice forward base thereafter.

If the selling continues, suspect it will keep moving sideways and bounce between 49c and 61.5c.

My 53.5c top up point on results day looks to be a decent entry point. Still waiting patiently to see if a dip to 49c occurs as I want one more top up bite before it gets out of reach ...

Some may wonder why $AIM SP opened up strongly after the release of the results this morning, but then has actually dropped significantly after the investor call.

Before explaining why I think this has happened, I want to say that, in my opinion, $AIM gave a reasonable update today. I haven't gone through it in detail yet, but I'll jot down some of the highlights at the end of this straw.

So What's the Big Deal?

I wonder if anyone else noticed the sleight of hand which - to me anyway - is a significant change in strategy? (I wrote this sentence when the SP was still up amost 10%, and I guess the answer is "yes" lot's have noticed!)

Spot the difference in the following 2 slides: the first is today's at FY25, and the second from 1H FY25.

From today at FY25

From 1H FY25 6-months ago

Put simply, the target for FY29 Tech revenue has come off from $150m to $120m in 6 months.

And so, a continuing Services revenue (being new professional services to help clients embed new products) has been created.

Magically, $30m revenue is targeted for this new Services product, so the $150m overall revenue target remains, but presumably the previous $60m EBITDA will be reduced. However, what the $60m has become was not communicated (but can easily be calculated).

I was a bit slow at picking up this difference (didn't realise until it came up on the Q&A), and so I consider that Tony and his CFO were less clear in explaining the change in thinking.

My Assessment

For those of us who have modelled what a $150m revenue tech business in FY29 looks like in terms of value, the SP today does not reflect this value. In fact, the margin of safety is so large, that there is ample room for several more "downgrades" like today.

If you want to have a quick look, consider @Travisty's recent valuation (noting the discount rate as well as margin of safety applied!)

Pending a deeper analysis of today's result, I think $AIM is making progress. But this material change in just 6 months is - to my way of thinking - a clear demonstration of why a high discount rate and/or factor of safety is warranted for this business.

My assessment of risk also means I will maintain my current position size of 5%.

Should, in future reports, $AIM demonstrate that it can scale towards its lofty ambition, there will be ample opportunity to add more.

Selected Other Highlights

Above, I have focused on the big shift of the day, there is also a lot to like in the FY delivery, including:

- Encoders growing by +39%

- Tech revenue up +19%, accelerating +$23.6m in H2 from +$17.5m from 1H

- Cash balance up by +$3.8m to $14,2m and no debt - aided by change to structure of contracts

- Investment in product fully expensed ($3.5m off EBITDA)

- Expanded from 11 to 25 countries, driven by EU

- LEXI Voice is now being implemented in initial customers, with revenue expected in H2 FY26

- LEXI AI is targeted for launch at the NAB show in April 2026

There are a few technical revenue issues that I need to work through, including it sounds like some restatement of last year. (Note to self to have a closer look.)

Tony peppered the presentation with progress at several high profile clients. A few examples:

AWS is switching off its human services and moving fully to Lexi, one of $AIMs largest enterprise customers, for the live events it hosts. (Breaking news today,....based on accuracy of the AI being better than humans.)

Wins in the US Government (US Congress and US Senate, leveraging a reference case from the US) and Canadian parliament - indicating progress on the Government row of the 9x9..

Conclusion

Long term aspirational targets are a double-edged sword, Initially last year we saw the $AIM SP benefit from them, and today we are seeing it suffer. However, overall, this business is executing its strategy, and is growing strongly, with the new products moving into commercialisation phase and potentially opening up the addressible market.

While the aspiration has been reset, from my perspective, the overall thesis is intact and the changes are relatively minor within the margin of safety.

Disc: Held in SM and RL

AI media reported a 2% decrease in revenue- the market doesnt like it- however as has been laid out here before this misses the fact that tech SaaS revenue is growing whilst the old revenue model is deliberately being phased lower.

tony reiterated his FY29 outlook which may be overly optomistic however there is a large margin of safety at todays current market cap!

encoder sales are increasing

tech sales are increasing

LEXI voice and LEXI AI are expected to contribute to revenue over the next 1-2 years.

i think the market is missing a trick here and i have topped up on todays weakenss making AIM my second largest holding in RL

keen to hear the brains trusts opinions on todays results

Thursday 28 August 2025 Registration link: https://us02web.zoom.us/webinar/register/WN_6mTAMpSbS1W3SgXHuDjzCg Investors will be able to use the Q&A function on Zoom during the webinar, or can submit their questions ahead of the webinar to [email protected] This announcement has been approved for release by the Company Secretary

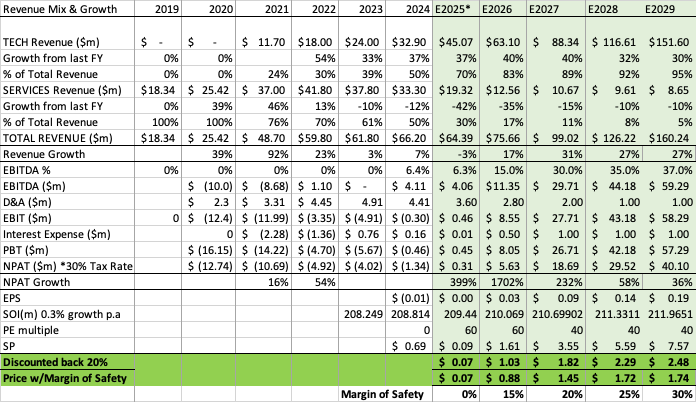

UPDATED VALUATION Ahead of FY25 results (AUG 24th 2025) of $1.74

I forgot to update my valuation and projections post HY25 results in Feb, but I wanted to get ahead of the full year results. Below is an updated valuation table, mainly to the estimated FY25 result.

I know there are a lot of numbers in my projection and only small deviations can change things dramatically. However my thesis is this, at least for the upcoming FY as the first step to the 2029 target:

- Tony has stated many times in interviews over the past 6 months that they expect the transition of TECH to SERVICES REV composition will continue and expect TECH to be at 80% of total REV by Dec 2025. So, I have estimated a 70/30 split between TECH and the declining (on purpose) SERVICES sections for this FY, then at 80/20 split from HY26. *Please note if this is achieved and considering a similar growth in Tech Rev of 37% for FY, then the H2 REV for Services would drop from $14.3m in 1HY25 to ~$6.7m in the 2HY25. A huge drop that may not happen and therefore may surprise on the top line.

- Tony has also mentioned multiple times, including on his most recent Strawman interview that they project $4m in EBITDA, which I have included in my FY25 projection.

- D&A are estimated based on the run rate from HY25 and also comments from previous CFO (John Bird) on the FY24 earnings call. Only thing that would blow this out is if AIM send big on PPE or some intangibles during the 2nd half, but as Tony has said numerous times, they like a "clean balance sheet" and therefore don't like to capitalise asset purchases onto the balance sheet, they prefer to expense it on the P&L.

- While my projection goes out to FY29 to see how things could possibly move towards the stated target of of $150m in REV & $60m in EBITDA (mainly through organic growth using the 9 box matrix outlined as their focus), I have used a very conservative discount rate of 20% as well as using incrementally larger margins of safety on the future years to reflect the additional execution risk.

I'm eager to see how the numbers look and hear what Tony and Jason have to say on Thursday!

Disc. HL in RL & on SM. (one of my largest Small/Micro Cap positions)

SCROLL DOWN FOR UPDATE....

RePost of initial valuation so it's easier to read. Thanks @Bear77 for your guidance on copy & pasting. it worked perfectly!

Hello Straw People!

My name is Travis, and this is my first ever company valuation. I am newbie "premium" member but have been a "free" member for a couple of years now and have thoroughly enjoyed reading through the various forums, straws, and valuations of others, albeit 4 weeks delayed.

My background in finance is limited to some minor study alongside a huge passion for reading and self-education, which is why I decided to become a premium member, as the collective thoughts, experience and truthful and honest feedback provided here I know I will find most valuable in the process of trying to make a rational investment.

*Please note, I was very hesitant to put my valuation and thoughts out there as I am a novice investor and far less experienced than many here and I assume off the bat that I will have errors in my judgement and analysis that will be highlighted, for which I am ready for and implore you to provide constructive critic and highlight were I may be biased in my thinking!

Before I start, please let me apologise if I babble on, repeat myself or just plainly confuse some with my explanations.

The aim of my valuation (no pun intended) and time of posting was to get It out there prior to the release of the Annual Report on Thursday.

Ok, back to my valuation. I have been a shareholder of AI-Media for just over 12 months and found out about the company here first, alongside @Wini’s previous appearances on the Coffee Microcaps webcast. Which alongside the Meetings on Strawman (which I finally have access too) I find this to be a great way to discover and hear from Small Cap companies.

I hope to write at length about the specifics of my thesis in time, however at this stage the valuation is based on a few important factors that I believe the company has in place and the opportunities in the future.

1. Founder led company, with Tony being extremely passionate and knowledgeable about the company and how Ai-Media’s product suite fits into the workflows of its customers.

2. He has considerate Skin in the Game, which should align our goals of increased shareholder value.

3. They have a product suite in which the Falcon Encoders are imbedded into the workflow of customers, with Lexi sitting on top to provide a captioning service that is faster, more accurate and 90% cheaper than current Human in the Loop captioning.

4. They have a tailwind with advancement of Ai technology, while also having several additional markets to build on. The market matrix of 9 sections was a highlight of the growth potential Americas/Broadcast (currently the biggest Rev generator), Americas/Government, Americas/Enterprise, EMEA/Broadcast, EMEA/Government, EMEA/Enterprise, APAC/Broadcast, APAC/Government, APAC/Enterprise.

5. The market may not be entirely aware of the Tech growth part of the company’s Revenue and how that transition of revenue mix is going accelerate their revenue growth, their margin expansion and EBITDA to get to the FY29 target of $150m in Revenue and $60m in EBITDA.

Which brings me back to my valuation. While it is detailed, I have tried to use as many numbers as possible that are historical, not too outrageous as well as any information I could obtain from the financials both in the reports and from the webinars that Tony and John Bird (outgoing CFO) have held over the past 3-4 years.

Below is my DCF for the company out to FY29 to see what is required for them to get to the target Tony has spoken about. Please note, DCF’s aren’t my forte and I’m sure I’ve made glaringly obvious mistakes, so please point them out to me as I need as many honest minds to provide me with feedback.

NOTES to my DCF:

- EBITDA Margin is based on a progression to 40% by FY29 to get the $60m target amount.

- SOI growing by 0.3% based on the growth from FY23-FY24. Tony and John have said they have no intention to capital raise, which should limit SOI growth.

- D&A future estimates based on CFO (John Birds) comments in FY24 results webinar. See at 1h5min mark here. Although he expects D&A to drop to around $0.5m in 3-4yrs. I’ve kept it higher in case of future acquisitions that they decide to capitalise on the balance sheet.

- Interest Expense based on a conservative future amount. I don’t foresee AIM requiring any debt to fund future growth, as Tony and John have said numerous times that it will be funded with cashflow. However, I thought I would include some interest expense just in case.

- PE is the most difficult variable to add in the mix. I went with a 40x multiple in FY27-FY29 based purely on a conservative multiple for a company averaging 146%pa NPAT growth between FY25-29.

- I’ve used a 20%pa. discount rate as well as a tiered Margin of Safety to account for the risk projecting so far into the future.

So, there it is! My first ever Strawman Valuation for $1.61 for Ai-Media (AIM).

Please let me know where I might be wrong in my calculations, or where I may have stated lofty or incorrect numbers that could have affected my valuation.

Disc. I hold shares in RL & on SM.

UPDATED VALUATION Ahead of FY25 results (AUG 24th 2025) of $1.74

I forgot to update my valuation and projections post HY25 results in Feb, but I wanted to get ahead of the full year results. Below is an updated valuation table, mainly to the estimated FY25 result.

I know there are a lot of numbers in my projection and only small deviations can change things dramatically. However my thesis is this, at least for the upcoming FY as the first step to the 2029 target:

- Tony has stated many times in interviews over the past 6 months that they expect the transition of TECH to SERVICES REV composition will continue and expect TECH to be at 80% of total REV by Dec 2025. So, I have estimated a 70/30 split between TECH and the declining (on purpose) SERVICES sections for this FY, then at 80/20 split from HY26. *Please note if this is achieved and considering a similar growth in Tech Rev of 37% for FY, then the H2 REV for Services would drop from $14.3m in 1HY25 to ~$6.7m in the 2HY25. A huge drop that may not happen and therefore may surprise on the top line.

- Tony has also mentioned multiple times, including on his most recent @Strawman interview that they project $4m in EBITDA, which I have included in my FY25 projection.

- D&A are estimated based on the run rate from HY25 and also comments from previous CFO (John Bird) on the FY24 earnings call. Only thing that would blow this out is if AIM send big on PPE or some intangibles during the 2nd half, but as Tony has said numerous times, they like a "clean balance sheet" and therefore don't like to capitalise asset purchases onto the balance sheet, they prefer to expense it on the P&L.

- While my projection goes out to FY29 to see how things could possibly move towards the stated target of of $160m in REV & $60m in EBITDA (mainly through organic growth using the 9 box matrix outlined as their focus), I have used a very conservative discount rate of 20% as well as using incrementally larger margins of safety on the future years to reflect the additional execution risk.

I'm eager to see how the numbers look and hear what Tony and Jason have to say on Thursday!

Disc. HL in RL & on SM. (one of my largest Small/Micro Cap positions)

25th July 25

Tracking along nicly so far though looking forward to hearing everyone’s comments once figures are released. Im figuring, this climb as far as most are concerned here, would be in anticipation of better figures at this stage, right?

Tracking along nicly so far though looking forward to hearing everyone’s comments once figures are released. Im figuring, this climb as far as most are concerned here, would be in anticipation of better figures at this stage, right?

Note: Deanne Weir no longer on the board and has recently sold AIM shares refer annoucement https://announcements.asx.com.au/asxpdf/20250317/pdf/06gqbgly00tqbn.pdf

Current Market Cap of Ai-Media at $0.53 is $110.6m

Recent Management Buying Summary

Buy

Otto Berkes

· 13 June 2025

26,315 price $0.57 per share ($15,003.74)

Brent Cubis

· 10 June 2025

35,000 price $0.555 per share ($19,425)

Anthony Abrahams

· 16 December 2024

312,500 price $0.80 per share ($250,275)

Cheryl Hayman

· 9 December 2024

50,000 price $0.86 per share ($42,887.39)

Management Bio's

John Martin - Non-Executive Chair (appointed February 2024)

John joined the Board in 2010 and served as Chair until 2013, NED until 2024 and has been re-elected as Chair in February 2024. He is an experienced company director and business executive, having served as CEO and director of ASX-listed Babcock & Brown Communities, Primelife and Regeneus. He is a former corporate and commercial partner of law firm Allens. John is a Non-Executive Director of Australian law firm Sparke Helmore; Sydney biotech company Biopoint; US internet services company Lokket and Melbourne not for- profit CCRM Australia. He is also a member of the Australian Institute of Company Directors.

Alison Loat - Non-Executive Director

Alison is the Managing Director, Sustainable Investing and Innovation at OPTrust, a Canadian public pension plan. Previously, she was the Senior Managing Director of FCLTGlobal, a long-term investing organization, the CEO of a think tank and a consultant at McKinsey & Company. She’s also on the board of two Canadian educational institutions and a privately held media company. Alison received the Queen’s Gold and Diamond Jubilee Medals and was named one of the 100 Most Powerful Women in Canada. She received the ICD designation from Canada’s Institute of Corporate Directors. She has degrees from Queen’s University and the Harvard Kennedy School.

Cheryl Hayman - Non-Executive Director

Cheryl joined the Board in March 2022. Has extensive experience working as an independent Director across multiple sectors including ASX-listed companies as well as industry bodies and not-for-profit organisations. Cheryl is currently on the board of Silk Logistics Holdings (ASX:SLH) [Chartered Accountants ANZ and Guide Dogs NSW/ACT]. Cheryl’s corporate experience encompasses a range of senior strategic technology, digital strategy roles and global marketing roles including Head of Marketing and Innovation at Sunrice, George Weston Foods, Unilever Australia, NZ and UK, Yum Restaurants International and Who Weekly magazine. Cheryl is a Fellow of the Australian Institute of Company Directors and a Fellow of the Governance Institute of Australia, and serves as Chair of AIM’s Remuneration and Nomination Committee and member of the Audit and Risk Committee .

Brent Cubis -Non-Executive Director

Brent joined the Board in July 2024 and is Chairman of the Audit and Risk Committee. Brent is a highly experienced Non-Executive Director and CFO with over 30 years of board level experience in senior finance roles for global businesses in Health, Medical Devices, Media, Property, Tourism and started his career at Deloitte. Brent has been the Chair of the Audit and Risk Committees for all the public and private companies outlined below. His previous executive roles have included CFO of Cochlear Ltd and Nine Network Australia and for various other private companies.

Brad Bender - Non-Executive Director

Brad was appointed as a Director in November 2024 and brings over 25 years of global experience in technology, product innovation, and general management. As Vice President of Product Management at Google, he led AIdriven initiatives for Google News and Search Ecosystems, including the transformation of Google’s News experience and AI-driven initiatives reaching billions of users worldwide. Earlier in his career at Google, he founded the Google Display Network, growing it into a multi-billion dollar business. Before Google, Brad was Vice President of Product Management at DoubleClick. Brad’s expertise spans product innovation, AI-driven solutions, and scaling global technology platforms. A holder of multiple patents in data and privacy, Brad was named a Crain’s New York Business "40 under 40" leader in 2012. He holds a Bachelor of Science degree from Cornell University and is currently an advisor, investor, and board member to a range of start-ups, businesses, and nonprofits across the tech, media, entertainment, and services industries, including currently serving as an independent board director at Entravision (NYSE:EVC).

Otto Berkes - NON-EXECUTIVE DIRECTOR

Otto Berkes received a BA in Physics from Middlebury College and an MS in Computer Science and Electrical Engineering from the University of Vermont. He was an Xbox co-founder at Microsoft where he drove groundbreaking hardware and software innovation in computer graphics, home entertainment, mobile devices, and cloud services. After an 18-year tenure, he moved to HBO to build their video streaming services, and, as CTO, to lead their technology division and to champion the company’s digital transformation. He subsequently joined CA Technologies as EVP to spearhead new product incubation and to direct the company’s shift to cloud services and subscriptions. After the company’s acquisition by Broadcom, he joined Acendre’s board and later accepted the CEO role. Through a combination of acquisitions and organic development, be created HireRoad, an end-to-end analytics-driven talent platform. Otto is coinventor on thirteen patents, a recipient of Microsoft’s Xbox Founder Award, an Emmy Award, and an Edward R. Murrow Award. He is the author of Digitally Remastered: Building Software into Your Business DNA, a book about digital transformation in the enterprise and the new role of software. He recently completed a six-year term as a trustee for the University of Vermont and is a member of the board at Integral Ad Science, a leading advertising technology business, Intelagree, an AI-driven contract management solution, and AI Media, a global provider of AI-powered captioning services. Otto currently pursues his passion for software engineering writing apps for weather enthusiasts that are available in Apple’s App Store.

Tony Abrahams - CO-FOUNDER AND CEO

Tony Abrahams co-founded AI-Media in 2003 and has led the company as CEO from inception, through a period of significant transformation. Driven by a passion for technology and inclusion, Tony has steered AIMedia from its origins in human-based captioning to becoming a global leader in AI-powered language solutions. He was the force behind the acquisition of EEG, a U.S.-based tech company whose innovations - including the LEXI automatic captioning engine and iCap delivery network - have been central to AI-Media’s shift toward real-time, scalable captioning and translation technology. Today, AI-Media’s solutions help broadcasters, enterprises, and governments deliver accessible content to audiences worldwide. Tony holds a Bachelor of Commerce (Honours) and Bachelor of Laws from the University of New South Wales, where he was awarded the University Medal in Accounting. As a Rhodes Scholar, he completed both an MPhil in Economics and an MBA at the University of Oxford. While at Oxford, he contributed to the establishment of the Oxford Internet Institute, which researches the societal impact of the internet. Tony’s commitment to social impact extends beyond AI-Media. He served as a Director of Northcott Disability Services from 2010 to 2018 and was named a Young Global Leader by the World Economic Forum in 2013. A member of the Australian Institute of Company Directors since 2006, Tony continues to advocate for technology that drives both innovation and meaningful inclusion.

@occy So without reading you analysis I went ahead and charted it out. I hadn’t read your remarks completely as I didnt want my own obscured off the bat. Now i have read your commentry you can see the differences between them. Where it is right now on the charts, Im not seeing any direction to really enforce with any certainty which direction it will take so ill take with the worst case, thinking its got more to drop for now. You could actual say that From A up to B on the 1d is the start of the rise forming the wave1 up with the most recent low on the 5th March being wave 2 down, however the indicators aren’t providing my enough confidence so I will wait. As you may be aware, i like to wait for the 1/2 up and even the next i/ii after that along with improved Indicators.

Have finally worked through the AIM 1HFY25 video and releases. My immediate reaction on reading the releases back then was one of uncertainty as the financial numbers did not line up with the positivity from Tony. Unpacking the content took time, but it was well worth the effort as I feel significantly more educated on AIM as a company and I remain 100% onboard.

Discl: Held IRL and in SM

ICAP NETWORK AND LEXI USAGE ARE FIRING

Firstly, I plotted the iCap Network and Lexi Usage Trend slides from both the 1HFY25 and FY24 slide packs into a graph so that I can get a continuous HoH view (both the original slides only show pcp, which only tells half the story)

- I like what I am seeing in terms of the clear and consistent upward trajectory of both (1) the monetisation of the iCap network and (2) Lexi usage

- Revenue must, almost be definition, grow correspondingly over time - which is why upfront, the shortfall in revenue did not quite make sense

- It is clear that Tony considers this trend to be the main leading indicator of how well the business is travelling, the technology uptake etc - similar to C79’s samples processed per quarter chart, this makes sound sense to me

PRODUCT IS READY FOR ASSAULT ON EUROPE BROADCAST

The speed of iCap/Encoder product rollout has significantly accelerated:

This significant solution acceleration is impressive as different orchestration methods between the broadcast playout systems (works completely differently from the US) and different character sets was needed (particularly for the Slavic languages - Poland, Romania, Slovakia, Czechia etc)

- “We are dealing with languages that iCAP and Lexi have never actually had to produce a particular character for before - this work is now done”

European Accessibility Act comes into effect on 28 June 2025 - The Act mandates that a range of products and services such as consumer electronics (TVs, smartphones, computers, gaming consoles, etc.), ticketing and vending machines, websites and mobile acts, among others, comply with accessibility requirements for persons with disabilities

AIM has sold a technology product in each of the 14 countries on the right for the first time in this half

The full focus on opening up Europe has happened/is happening and the ability to extend the iCap and Encoder to new countries in weeks will continue to increase the pace of opening up markets outside of North America

2 NEW PRODUCTS

Lexi Voice is clearly launching 7 April 2025 - big tick

Lexi Brew - I am positively cautious on this - it uses the same iCap/ Encoder architecture/AI, it opens up new revenue streams, and I can see how it will help the Enterprise square, but it felt like it could distract from the immediate focus on the main EMEA game from a technical/product development perspective. Also, this puts AIM down the “AI Play” path, which is not quite how I saw/see AIM. Need to think about this a bit more.

MAKING SENSE OF THE REVENUE SHORTFALL

The underwhelming revenue numbers were actually a bit of a worry as this was the first sign of inconsistency in Tony’s narrative. Plotting the revenue by regional operating segments going back to 1HFY2022 post the EEG acquisition, the 1HFY25 revenue shortfall was quite glaring against trend. This really did not make sense if the iCap and Lexi Usage numbers were climbing as they were (per above).

Dinesh made the following comments against the P&L Summary slide:

3% fall in revenue is driven by Services revenue decline, as a business we are trying get out of

Increased billing of Lexi of 45%, sales has increased 45% (this correlated to the growth outlined in the iCap/Lexi usage slide, but can’t see it manifest in the revenue numbers), invoiced the client and collected cash but is sitting as deferred revenue in the balance sheet - reflected in cash flow (this also makes sense)

Transforming into a SAAS business - billing upfront on long-term contracts, and unwinding that over a period of time

To confirm this, Note 8 in the Appendix D showed a sharp increase in Billings-During-the-Period in 1HFY25 - from $10m to $13.8m, and the closing balance rising sharply from $4.3m to $7.0m - this correlates to what Dinesh said above:

Around 1:39 of the video, Tony made the point that about $2.6 or $2.7m of the $7m Contract Liability balance was Lexi forward sales this period that will be progressively realised in the future and that it was all relating to North America

At 1:41, Tony clarified that the $7.0m of Contract Liabilities in the balance sheet all relate to Lexi forward sales ($4.3m of which were prior period forward sales which presumably still cannot be recognised this period)

I thus added ~$2.6m to the revenue chart against North America and Total Revenue - the blue bar, meaning that if AIM COULD recognise 100% of the Lexi revenue already invoiced and collected for upfront, it would seem that the revenue for 1HFY25 appears to run higher than the run rate of the actual trend line

Tony and Dinesh explained at length that AIM was transitioning from upfront recognition of revenue to periodic recognition of subscription revenue and that during this transition period, the revenue numbers will bounce around. The focus should be on Lexi usage and Lexi revenue growth as that is the true indicator of future revenue and the success of the business - from an accounting perspective, this commentary makes sense.

The challenge that AIM has is that it is not explaining this very well in terms of actual revenue sold, but recognised in this period vs the next etc - Alcidion is a good example of where they are clear with every contract signed, the TCV and the amount of the TCV that is recognised in the current period. HSN also had the same problem in 1HFY25 with lumpy periodic licensing sales in 1HFY24 distorting the 1HFY25 numbers and comparisons.

Tony’s frustration on this front is clearly evident. Telling the market to “ignore the revenue numbers and focus on iCap/Lexi sales/revenue” is not the answer though. Tony and Dinesh need to find a better way to disaggregate the Technology revenue, provide visibility of the forward sales which cannot be recognised and clearly state Lexi-related sales revenue, so that the market can then work backwards and reconcile the “true” revenue position, during this messy transition period.

The combination of (1) 45% growth in Lexi sales that has actually been invoiced and collected (2) the insight on Contract Liabilities (3) the transition from upfront revenue recognition to SAAS revenue recognition gives me confidence that the revenue shortfall is merely an accounting treatment transition issue.

OTHER TAKEAWAYS

Operating cash flow positive of $3.3m again, following slight ($0.1m) negative in 2HFY24 - contributed to a healthy cash balance of $14.1m

Key cyber security accreditations that AIM is focused on is SOC II Implementation and ISO27001, against the new Lexi platform - these are painful implementation and input processes, but once obtained, will address a significant amount of customer concerns around security

QUESTIONS TO ASK TONY

- Would like to unpack “Encoders” in the ecosystem slide - there is mention of Falcon, Alta and Encoder Pro, then “Alta everywhere” - I have thought about the encoders as an EEG box, period ...

- Can he and Dinesh please find a way to clearly disclose Lexi Sales booked and recognised/not recognised as a disclosure item to prevent unnecessary confusion around the revenue numbers.

- Lexi Brew - how and why this can be done in parallel without distracting the big focus on EMEA, what is the competition like

SUMMARY

Having worked through the concern areas, my conviction remains intact. With the current market volatility, will look to top up if the price dips below $0.65, the close to $0.60, the better

I'm just off the $AIM 1H FY25 Results call. I'm not going to summarise the results here. At the headline level they look underwhelming as the business transitions from a legacy people-supervised AI translation service, to a fully AI model. In fact, the market reacted to the headlines opening down 10% as - I assume - holders who don't understand the business traded out on the headline. Hopefully we'll get more opportunities like that, as I'll likely be on the other side of any such price action.

Instead this is a recommendation to any StrawPeople (whether holders in $AIM or not) to watch the recording of the call when it becomes available. My head is buzzing with everything CEO Tony shared with us and, to be honest, I'm going to have to watch the whole two hours again to really understand it.

But what stands out for me, is the evidence this presents in how the "application layer" of software leveraging AI is disrupting business processes, not just in $AIM's legacy media business, but pretty much everywhere.

Tony was very generous with his time in explaining the use cases and key metrics, and there is a lot to unpack in the presentation.

Although in RL I have taken only a modest 3.8% position in $AIM, I was asking myself over and again during the presentation the question @Strawman put to me during my SM meeting last year, along the lines of "how much would you be prepared to put behind a "fat pitch"?" I really am starting to wonder if $AIM is such a fat pitch.

Of course, it is important to temper the excitement that naturally comes from listening to Tony with the reality that there are countless other players moving to be part of the AI disruption and revolution. I have no doubt $AIM will be successful in the top row of its 9-square matrix (see below chart), but it is probably important to be somewhat more circumspect about the rest.

But with Lexi Voice and Lexi Brew, maybe they ARE moving fast enough. If they can execute successfully across the entire 9-squares, then all bets are off as to the valuation.

For those StrawPeople who are Trekkies, during the call, I whatsapp'd my daugher in London a picture of Lexi Voice, with the message "The Universal Translater is Launching on 27th April, with an initial 125 languages".

Related to discussions here today and yesterday about another Strawman favourite, Tony is the exact opposite in terms of communication. He is clear, deliberate, almost to the point of painful detail of explaining what they are doing and what the key metrics are to track. Every question got answered ... in detail ... with supplementary questions returned to as well. A full 2-hour call.

I'm not going to do anything rash or hasty here. But I do wonder whether this is a "fat pitch".

Disc: Held in RL and SM

AIM CEO Anthony Abrahams has bought another $200,000 worth of AIM stock @ $0.80

Adding to his significant skin in the game.

https://investorpa.com/announcement-pdf/20241209/78690.pdf

Understanding the use cases of a company’s products and services can be challenging when we don’t interact with them directly. I thought I'd highlight a recent use case of a type of event Ai-Media plays a role in with their captioning products and services.

AWS recently hosted their annual re:Invent 2024 event in Las Vegas. I’ve been watching a couple of the keynotes - mainly around the new AI models they're launching. It was a bonus to be able to catch some of the live captioning provided by Ai-Media’s LEXI AI captioning services. The quality is very good and with delays of just 2-3 seconds.

The event videos are available on Youtube, and you can catch glimpses of the captions at certain camera angles to evaluate their quality: https://www.youtube.com/watch?v=LY7m5LQliAo. Turning on the captions in Youtube will display the LEXI generated captions with all the timing synced up - with no delay.

To put the scale and complexity into perspective, re:Invent had 70k attendees, with multiple simultaneous stages and overflow rooms, live streaming online and over Youtube. Beyond the main stages, the event featured smaller presentations. In fact the conference had 40+ rooms with in-room live captioning.

These types of events are huge, with lots of competing demands from large in-person crowds and live-streaming viewers worldwide. Lots of different presentations going on simultaneously, and very high stakes. And for Ai-Media’s range of encoders, iCap cloud and LEXI AI captioning service - this is their bread-and-butter.

In fact, AWS is now lugging around 51 Ai-Media encoders to some of their biggest events:

Hopefully this provides an idea of the types of areas Ai-Media is playing in.

Sources:

- https://www.linkedin.com/pulse/reinvent-streaming-recap-2024-gabriel-spence-aftac/?trackingId=LzVfwEqPS4aY043ZaHgwVA%3D%3D

- https://www.linkedin.com/feed/update/urn:li:activity:7270979056978825216/

- https://www.linkedin.com/pulse/training-ai-make-live-experiences-more-accessible-taylor-wilkins-gep2c/?trackingId=IuMtFII9SZapBXKGvi2oQA%3D%3D

Media Release: https://announcements.asx.com.au/asxpdf/20240829/pdf/0676bss606c3jj.pdf

FY24 Annual Report: https://announcements.asx.com.au/asxpdf/20240829/pdf/0676bnpw5ms0lw.pdf

FY24 Presentation: https://announcements.asx.com.au/asxpdf/20240829/pdf/0676bzwbglkvw6.pdf

FY24 results were released today and once again the top line results were a yawn-fest with revenues growing by 7% to $66.2m. However, the real story lies beneath the surface, where the company’s dynamics are shifting. Ai-Media’s fast-growing Technology division (good co) contrasts with its declining Services division (bad co), leading to significant changes behind the scenes.

The company continues to recomposition itself from Services to Technology leading to increased gross margins

The positive trend in profitability continues

Technology revenue grew by 37% over the year and now run-rating at 52% of the group’s revenue and 68% of its gross profit. Ai-Media is rapidly transforming from a people-driven captioning service company into a caption technology and AI company. Management anticipates that Technology revenue will comprise 80% of the Group’s revenue by December 2025. If anyone needs a reminder of how well the Technology division has grown over the years, just take a look at the revenue chart below.

EEG was acquired by AI-Media in 2H FY21

This is one where I’ll need to go back and review my notes and old transcripts, but as my memory stands right now, there appears to be a distinct shift in management’s optimism during the conference call.

The key talking point was their “aspirational” five-year organic growth target: $150m in revenue and $60m in EBITDA. This translates to CAGR of 17.8% for revenue and 70.9% for EBITDA over five years. This is a significant leap from the single-digit top-line growth rates of recent years. However, it’s also quite attainable, given the rapid expansion of the Technology business, which now accounts for a much larger share of revenue and gross profit. Management believes they can achieve this by expanding beyond their core US broadcasting live caption market, targeting new geographies (with Europe and the UK as key areas), sectors (focusing on Government and Enterprise), and product offerings (including new AI-enabled language services).

The prevailing sentiment is that Ai-Media is positioned at the right time and in the right place. They provide the industry-standard captioning infrastructure used by US live broadcast companies, and there is surging demand for AI technologies to reduce captioning costs and extend reach, especially since the rise of generative AI tools like ChatGPT in recent years. The company has already demonstrated high-profile, high-stakes use cases for fully AI-generated live captions, such as during the recent Paris Olympics for broadcasters in the US (NBC in English and Telemundo in Spanish!) and Australia (Channel 9). Moreover, access to new large language models and machine learning advancements is making it increasingly feasible to develop additional automated services beyond traditional live captioning. Over the next 12 months, the company plans to roll out human-level language translations, voice dubbing, audio descriptions, topic models, and sound effect recognition.

In a recent, and super awesome, episode of Invest Like The Best with Gavin Baker, there’s a segment on “AI First” companies. It’s around the 56min mark: https://overcast.fm/+ABA27uWiTk8/56:00. I immediately thought about Ai-Media. They act as a thin wrapper around AI models (leveraging transcription services from Microsoft, AWS, and Google), delivering what feels like magic to their customers and not only going after software budgets but labour budgets. Gavin also asserts that although AI First companies are experiencing rapid growth, it’s very challenging to build long-term defensibility around their business models.

But this is where the comparison ends. Ai-Media isn’t an AI First business; it’s a labor-based company that has transformed into an AI business. The company dominates the North American live broadcast market, with its hardware and software encoders deeply embedded into their customer’s workflows. Additionally, Ai-Media still offers a labor component for customers who require that extra peace of mind. This integration provides a level of defensibility that the vast majority of pure AI First companies lack.

Despite the bump today, it’s still trading at trailing 1.4x sales and 34x Normalised EBIT. The market is still skeptical that a 30%pa growing Technology division with a 80%+ gross margin will become the vast bulk of the business going forward.

EDIT: I had a EBIT multiple wildly wrong