Discl: Held IRL 3.87% and in SM

AIM's downward drift on no negative news is reaching the bottom of my previously marked top-up of 0.615 to 0.655 which is a decent support/resistance zone going back to Sep 2024.

Nest support level if this breaks is 0.46 to 0.49, from when AIM announced its FY25 results back in Aug 2025.

Discl: Held IRL 4.56% and in SM

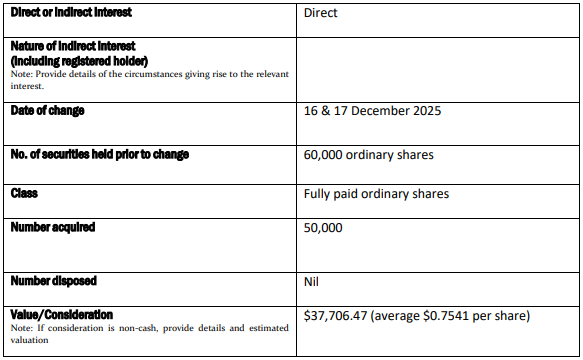

Very nice to see Brad Bender, one of the 2 high-profile-ish US-based directors AIM appointed in Oct 2024, top up his shareholding of AIM by ~83%. He added 50,000 shares to his initial 60,000 holdings from Dec 2024.

The value of $37.8k is small coin in USD, but better to see him buying than not.

Discl: Held IRL 5.16% and in SM

This came from AIM Investor Relations via email as I signed up to the AIM Investor Hub.

The spread of AIM information is a bit inconsistent right now. This email came direct. There is no announcement of this on the ASX nor on the Investor Hub itself. Tony has not posted on Linked In, but I expect him to do so shortly.

Looks like @Strawman and Tony are becoming/are best buddies!

Product & Market Webinar

Join CEO Tony Abrahams and CFO Jason Singh as they provide an overview of the Company’s current product suite alongside consolidated feedback from recent executive visits to Europe and the USA. The Company will outline how this international market feedback aligns with its existing strategy and product roadmap priorities.

The webinar will be moderated by Strawman's Andrew Page and investors are encouraged to ask questions on AIM's growth strategy and geographic expansion.

Webinar Details are as follows:

- Event: AI-Media Product & Market Update Webinar

- Date / Time: Wednesday 3 December 2025, 10AM (AEDT)

- Registration link: https://investorrelations.ai-media.tv/webinars/drLvQy-product-and-market-fit-webinar-dec-2025

The Company notes that this webinar is not a trading update. No financial performance, outlook, or guidance information will be provided, and questions will be strictly limited to product and market topics.

Ongoing demonstration of the growing momentum behind our LEXI AI captioning and translation platform

From planetariums to global media summits, broadcasters to local government, organisations worldwide are choosing AI-Media to deliver real-time accessibility and multilingual engagement, affordably, reliably, and at scale.

Recent wins highlight the versatility of our end-to-end ecosystem and why customers continue to displace legacy human-only solutions with AI-Media.

Scitech (Western Australia) – Making Live Science Truly Inclusive

Scitech, Australia’s leading hands-on science center with 300,000 visitors annually, faced a classic “impossible” captioning challenge: unscripted, fast-paced shows featuring complex astronomical terms inside a dome planetarium.

The Solution:

- LEXI Viewer deployed across the Planetarium, Chevron Science Theatre, and a fully portable mobile trolley for outreach events.

- Real-time AI captions handled terms like “Zubenelgenubi” and “Alpha Centauri” with ease.

Outcome:

What was once considered impossible is now seamless. Deaf and hard-of-hearing staff and visitors have praised the accuracy and responsiveness. Scitech is now more accessible than ever before.

“I’m impressed at how accurate and easy to use the LEXI Viewer is. This is a great step for making our venue more accessible.” – Leon, Planetarium Lead, Scitech

APOS 2025 (Bali) – Asia’s Premier Media & Entertainment Summit Goes Fully Multilingual

For the second consecutive year, Media Partners Asia selected AI-Media as the exclusive live captioning and translation partner for APOS – the region’s most influential media, telecom, and entertainment summit.

Solution:

- Large-screen English captions in the main hall

- Real-time translations into Korean, Vietnamese, Chinese, Thai, and Japanese delivered via the APOS app

- LEXI Voice AI dubbing streamed to foyer spaces and headsets

- Captioned live interviews broadcast from our on-site booth

Outcome:

550 delegates and 80+ global speakers experienced a completely inclusive, tech-forward event.

“AI-Media’s live captioning solution added a vital layer of clarity and inclusion… The live translation… further amplified access and engagement across APOS.” – Lavina Bhojwani, VP & GM, Media Partners Asia

Want to hear more about recent activity?

Some may wonder why $AIM SP opened up strongly after the release of the results this morning, but then has actually dropped significantly after the investor call.

Before explaining why I think this has happened, I want to say that, in my opinion, $AIM gave a reasonable update today. I haven't gone through it in detail yet, but I'll jot down some of the highlights at the end of this straw.

So What's the Big Deal?

I wonder if anyone else noticed the sleight of hand which - to me anyway - is a significant change in strategy? (I wrote this sentence when the SP was still up amost 10%, and I guess the answer is "yes" lot's have noticed!)

Spot the difference in the following 2 slides: the first is today's at FY25, and the second from 1H FY25.

From today at FY25

From 1H FY25 6-months ago

Put simply, the target for FY29 Tech revenue has come off from $150m to $120m in 6 months.

And so, a continuing Services revenue (being new professional services to help clients embed new products) has been created.

Magically, $30m revenue is targeted for this new Services product, so the $150m overall revenue target remains, but presumably the previous $60m EBITDA will be reduced. However, what the $60m has become was not communicated (but can easily be calculated).

I was a bit slow at picking up this difference (didn't realise until it came up on the Q&A), and so I consider that Tony and his CFO were less clear in explaining the change in thinking.

My Assessment

For those of us who have modelled what a $150m revenue tech business in FY29 looks like in terms of value, the SP today does not reflect this value. In fact, the margin of safety is so large, that there is ample room for several more "downgrades" like today.

If you want to have a quick look, consider @Travisty's recent valuation (noting the discount rate as well as margin of safety applied!)

Pending a deeper analysis of today's result, I think $AIM is making progress. But this material change in just 6 months is - to my way of thinking - a clear demonstration of why a high discount rate and/or factor of safety is warranted for this business.

My assessment of risk also means I will maintain my current position size of 5%.

Should, in future reports, $AIM demonstrate that it can scale towards its lofty ambition, there will be ample opportunity to add more.

Selected Other Highlights

Above, I have focused on the big shift of the day, there is also a lot to like in the FY delivery, including:

- Encoders growing by +39%

- Tech revenue up +19%, accelerating +$23.6m in H2 from +$17.5m from 1H

- Cash balance up by +$3.8m to $14,2m and no debt - aided by change to structure of contracts

- Investment in product fully expensed ($3.5m off EBITDA)

- Expanded from 11 to 25 countries, driven by EU

- LEXI Voice is now being implemented in initial customers, with revenue expected in H2 FY26

- LEXI AI is targeted for launch at the NAB show in April 2026

There are a few technical revenue issues that I need to work through, including it sounds like some restatement of last year. (Note to self to have a closer look.)

Tony peppered the presentation with progress at several high profile clients. A few examples:

AWS is switching off its human services and moving fully to Lexi, one of $AIMs largest enterprise customers, for the live events it hosts. (Breaking news today,....based on accuracy of the AI being better than humans.)

Wins in the US Government (US Congress and US Senate, leveraging a reference case from the US) and Canadian parliament - indicating progress on the Government row of the 9x9..

Conclusion

Long term aspirational targets are a double-edged sword, Initially last year we saw the $AIM SP benefit from them, and today we are seeing it suffer. However, overall, this business is executing its strategy, and is growing strongly, with the new products moving into commercialisation phase and potentially opening up the addressible market.

While the aspiration has been reset, from my perspective, the overall thesis is intact and the changes are relatively minor within the margin of safety.

Disc: Held in SM and RL

AI media reported a 2% decrease in revenue- the market doesnt like it- however as has been laid out here before this misses the fact that tech SaaS revenue is growing whilst the old revenue model is deliberately being phased lower.

tony reiterated his FY29 outlook which may be overly optomistic however there is a large margin of safety at todays current market cap!

encoder sales are increasing

tech sales are increasing

LEXI voice and LEXI AI are expected to contribute to revenue over the next 1-2 years.

i think the market is missing a trick here and i have topped up on todays weakenss making AIM my second largest holding in RL

keen to hear the brains trusts opinions on todays results

25th July 25

Tracking along nicly so far though looking forward to hearing everyone’s comments once figures are released. Im figuring, this climb as far as most are concerned here, would be in anticipation of better figures at this stage, right?

Tracking along nicly so far though looking forward to hearing everyone’s comments once figures are released. Im figuring, this climb as far as most are concerned here, would be in anticipation of better figures at this stage, right?