Consensus community valuation

Held: IRL 4.93% and in SM

Very nice to see a “sustained” SDR up move for a change - it has been a while.

Price is still behaving nicely, technically:

- The $2.68 to $2.86 level has held nicely and the bounce happened from this level

- The $3.70 to $3.87 resistance has kicked in

- If there is more momentum, $4.53 to $4.63 is the next up level

However, the price is ripe for a pullback after this sharp move:

- Drawn the retracement levels - a 50% pullback to ~$3.29 would be very healthy in the long run

- Downside looks to still be limited to $2.68 to $2.86

Discl: Held IRL 3.87% and in SM

Kim Anderson made her 2nd recent purchase of SDR shares on 1 May 2026, buying into the dips, it would appear.

- Held 24,500 shares going back to Nov 2023

- Bought 10,500 shares on 27 Mar 2026 @$3.01

- Bought 10,000 shares on 1 May 2026 @$2.90

The support level between $2.68 and $2.86 has held up quite nicely since late Feb 2026 and there looks to be good accumulation at these levels.

Discl: Held IRL 4.05% and in SM

There was no ASX announcement, but SDR announced 2 products on 15 Apr 2026 to expand its platform into AI-drive booking pathways:

- AI-driven direct bookings via LLM’s, via Demand Plus and

- AI-enabled OTA/intermediary channges via Channels Plus

- The first announced “AI demand partner” is DirectBooker.

It wasn’t straightforward trying to work out these 2 new capabilities from the various press releases, but here is summary from:

SDR Press Release: https://www.siteminder.com/news/siteminder-ai-hotel-distribution/

eCommerceNews (the clearest view): https://ecommercenews.com.au/story/siteminder-expands-hotel-platform-for-ai-booking-channels

DirectBooker, Overview: https://www.directbooker.ai/

DirectBooker Demo Video on how it works with an LLM: https://www.youtube.com/watch?v=yN814CVnnKc&t=285s

PROBLEM SDR APPEARS TO BE SOLVING

- SiteMinder’s own research suggests ~80% of travellers want AI assistance during their booking journey

- The core issue for hotels is visibility to users at all points of initial travel discovery, including LLM’s

- Today, LLMs generally lack (1) real-time pricing (2) live room availability and (3) cannot reliably complete bookings -

WHAT DIRECTBOOKER DOES

- DirectBooker is an AI-native aggregation and connectivity layer that connects hotel data directly, and in real-time, into LLM ecosystems.

- Hotels, via SDR, provide real-time rates, inventory, availability data to DirectBooker

- Delivered via a Model Context Protocol (MCP) interface, a technical standard that allows AL platforms to access live hotel data in real time, directly to LLM’s like Claude, ChatGPT and Gemini

- LLMs can query this data live, at the moment of user intent - real-time access to inventory is critical if AI services are to move beyond general recommendations to actual bookings

1. EXPANSION OF DEMAND PLUS (Direct AI Booking Pathway)

- SiteMinder’s Demand Plus is now integrated with DirectBooker.

- Within the LLM’s, travellers will be able to discover hotels through recommendations, view live rates and complete a booking on the hotel's own website

- SDR is making its hotel network discoverable and bookable from within AI assistants, not just via traditional distribution channels.

2. EXPANSION OF CHANNELS PLUS (AI-Enabled OTAs, Powered by DirectBooker)

- Channels Plus opens SiteMinder's hotel inventory to AI-enabled online travel agencies and intermediaries that search, compare and book on behalf of travellers.

- Discovery and booking remain within the partner platform, while the reservation is passed through SiteMinder to the hotel.

How the Flow Might Work

- A user interacts with an OTA with embedded AI

- The OTA uses LLMs to interpret intent and generate recommendations

- Behind the scenes, DirectBooker pulls real-time data from SiteMinder

- The OTA presents results and completes the booking within its platform

- The reservation is fulfilled via SiteMinder into the hotel

MY TAKEAWAYS

- AI is fast becoming a new “front door” to travel - the booking journey is evolving from Google/mestasearch to LLM”s

- SDR is ensuring its hotel network is visible and transactable from within this new LLM front door by enabling the “AI Distribution channel” via both Demand Plus and Channel Plus and the Direct Booker

- SDR is making itself indispensable to AI-driven booking flows and distribution channels, both direct and via OTA’s, before those flows and the channel fully matures

- Control of room inventory, availability, rates etc still rests entirely with SDR, which forms part off, or is the properties systems of record and workflows

- I don't think this causes direct disintermediation grief to OTA's but more ensures that existing non-OTA bookings that hotels usually receive via DemandPlus, remains visible/does not get lost with increased usage of LLMs for travel discovery

There is no mention of how these new capabilities is/will be monetised, if at all. This could be treated as core infrastructure and is not monetised ie, no change to Channels Plus and Demand Plus subscription cost - this would be positioned as a critical value-add capability to ensure there is no leakage of bookings from LLM users, OR perhaps new tiers may be introduced to provide hotels with an option to be “AI-visible” at a higher cost.

I have sent a note to SDR Investor Relations, asking:

- Are customers being given the option to opt in to the AI-enabled Demand Plus and Channels Plus, or are the new capabilities simply added to both modules as an “under-the-hood, value add” upgrade?

- Is SiteMinder planning to charge customers of Demand Plus and Channels Plus for these new AI capabilities eg. via additional subscription tiers for AI-enabled vs non-AI-enabled or

Either way, this is very positive from my perspective. It gives me continued confidence that SDR is absolutely staying on top of AI-driven changes in travel distribution, and building capability that ensures it stays completely relevant to its customers. Monetisation of this would be a very nice cherry to top it off.

Discl: Held IRL 3.84% and in SM

More SDR Director on-market purchases - a good thing.

Chart-wise, the $2.68 to $2.86 support level has held out very nicely this week, so these Directors buying at this level is added validation that this is looking to be a nice entry-point if you can look past current drama’s.

I wasn’t quick enough to top up when SDR fell below $2.68 briefly yesterday, but remaining highly vigilant to act if it falls below again.

J Macdonald

- Doubled down on her purchases last week where she purchased 20,000 shares costing $59.6k (not $29.7k as I wrote last week) - purchased another 10,000 shares at the cost of $27.2k

- While these are not big amounts in itself, she has added ~43% more shares to her holdings with these 2 purchases - that is a decent and decisive uplift in investment

S Lawson

- Made her 1st insider purchase with investment cost just shy of $50k

Together with Kim Anderson, 3 of the 7 members of the SDR board have made purchases this month.

Discl: Held IRL 3.84% and in SM

Director Purchases

2 SDR Directors made on-market purchases of SDR on 25-26 Mar 2026.

Both bought 10,000 shares, Kim spent $31,605, Jennifer spent $29,700. Given the timing and volume, this may be part of a Director confidence building exercise. Still good to have them buy in vs not buying.

Chart Update

Updated the SDR chart from a week ago:

- $2.68 to $2.86 is looking to be a better representation of the base that SDR seems to now be forming - I previously had a single line at $2.85 in the last update a week ago

- This range goes back to Sep 2022 during Covid - see zoomed out chart below

- The SDR price has only dipped below this level for 4 days from Mon 26 Jun 2023 to Thu 29 Jun 2023 in its listing history, during which it made its all-time-low of $2.51

- We are thus very close to rock bottom levels, but SDR has grown several times since those 2022/2023 levels

With sentiment remaining in the dodrums, time to watch the price very closely as it is getting pretty close to back-up-the-bus levels for me ...

Zoomed out view

Discl: Held IRL 3.71% and in SM

SUMMARY

Have been thinking a bit deeper about how SDR is embedded into a hotel’s (probably crude) tech stack, I am now clear that:

- SDR’s data moat is a prized and formidable one

- The SDR modules are really an extension of, and hence, very much a part of a hotel’s tech stack and system of record - the SDR intermediation layer is not a thin one at all

- The risk of vibe-coded disintermediation of SDR capabilities on the hotel end is low to zero because minus the SDR-wide data intelligence platform, which is closed, any vibe coded capability will add almost no value to a hotel

- The risk of OTA disintermediation or of OTA’s encroaching into the hotel-end is low to zero - I just can’t see the use case/benefit/advantage any of these will bring to an OTA or an OTA-wannabe. If either happens, is likely to be an OTA-end issue. I expect SDR will end up managing the impact on behalf of the hotels via additions/changes to the Smart Distribution/Channels Plus capability.

Based on the thesis review below and how far the SDR price has fallen, I started nibbling to top up today at $3.18. With the ongoing volatility, there is every chance it will dip closer to $2.85, a 2.5 year support area. Will be topping up again closer to that level if it dips that far.

REVIEW OF SDR’S MOAT

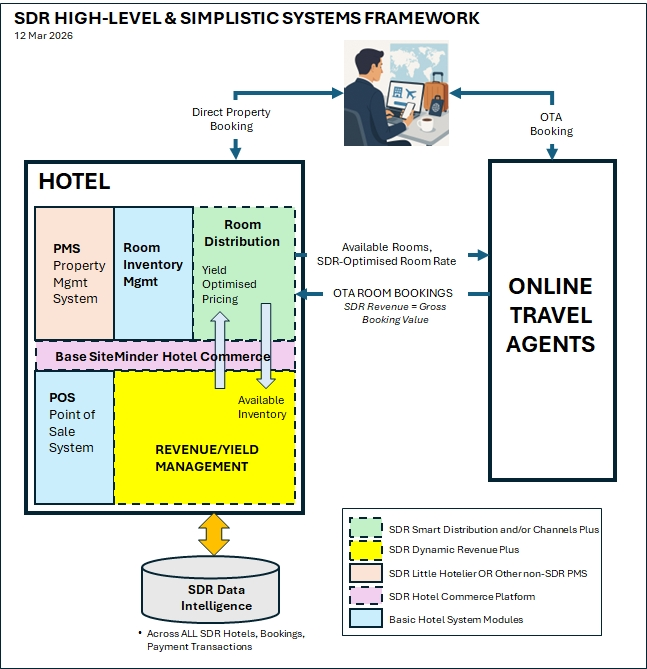

How SDR Fits Into A Small Hotel’s Tech Stack

This is how I am now thinking of SDR from a Hotelier’s perspective:

The barebones basic modules that a hotel would likely have before buying SDR would be a:

(1) Property Management System (PMS) to manage the overall hotel operations - this could well be manual or Excel or the various PMS systems available in the market;

(2) Point of Sale system - this is the system to manage any Food & Beverage outlets;

(3) Room Inventory management - some means of managing reservations, room inventory etc - could be a manual reservations book, Excel or is part of the PMS;

SDR modules are in dotted boxes - the intent is not to map out everything that SDR offers, but to highlight the key capabilities that SDR brings to a hotel that it is highly likely not to have, or can afford, as standalone systems, either because of cost, or the lack of expertise to actually use those systems/capabilities. I signed up to the SDR demo’s on their website which has some walkthroughs of the various modules, which I found helpful.

I thus see:

- SDR modules, base and Smart Platform, are either extensions of, or ARE the hotel’s operating system and operational workflows - the extent will depend on what systems the hotel already has/does not have currently;

- Every transaction flows through SDR and hence, SDR becomes part of, or THE, system of record of the property - that is what SDR has positioned itself more clearly recently;

- SDR Smart Distribution and Channels Plus as the hotels distribution connectivity/pipe to the room distribution capabilities of the Online Travel Agents (OTA);

- Revenue/Yield Management via Dynamic Revenue Plus is uniquely SDR - this is what completely differentiates SDR from any other “distribution” company, which is how analysts categorise SDR - I still think this is the biggest market misunderstanding of the capability benefit SDR actually adds to its Hotel customers.

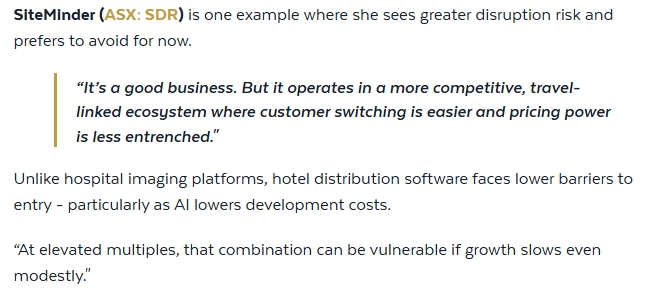

A good example of this is commentary from Ten Cap’s Jun Bei Liu, which I thought, quite honestly, was disappointing. I have no issue with her not wanting to invest in SDR, but the reason for avoidance reflected a poor/superficial understanding of how embedded SDR is, in a hotel’s tech stack. I have no idea what she means by “customer switching is easier” as SDR’s customers are hotels and their capabilities are actually embedded on the hotel-end.

AI Risk, Impact

From an AI disruption standpoint:

1. Because of SDR’s deep embedment into the core systems and workflows of a hotel, SDR is very much part of the hotel’s workflow and trusted system of record. In many cases, it is likely to be THE workflows and trusted system of record.

2. There is no per-seat licensing issue - licensing is per property and, SDR’s revenue is increasingly transaction-based.

3. The SDR Data Intelligence capability, built from millions/billions of transactions across its entire hotel customer base, is a formidable moat - SDR recognised this years ago and the Smart Platform modules was its strategy to monetise the insights, creating its own data flywheel, completely inaccessible from outside the platform.

4. Given the integration of the modules across a hotel’s tech/manual stack, and given the very basic level of IT in smaller hotels, I do not see vibe coding of any of SDR’s modules as a credible threat - the context and input from the data flywheel which continuously enriches the data intelligence simply cannot be replicated in a vibe coding scenario. I also cannot see what incentive there is for a small hotelier to spend any energy vibe coding as running a hotel is essentially a 24x7 endeavour.

5. SDR IS absolutely the neutral Revenue Manager for the Properties - revenue management is fundamentally challenging/previously non-existent, but SDR has found the way to deliver this, cost effectively, at scale, to small properties so they now have some capability they never dreamed of having. And SDR is performing this role with both its own AI agents over its extensive data around bookings, pricing, yields etc. - I don't think public LLM's will get here as the data remains completely closed

6. I cannot see how any possible disintermediation in and around the OTA’s, if it ever happens, will impact SDR - folk like Google have tried and failed. The booking engine itself should be “relatively easy” to vibe code, but the CONNECTIVTY out of the OTA’s and into the millions of hotels around the world, is not something that is easily (1) replicated (2) implemented (3) supported and (4) maintained, on an ongoing basis, never mind issues of security, payments etc. SDR’s Smart Distribution and Channels Plus capabilities were introduced to simplify connectivity to the distribution channels - that this is growing nicely is indicative of how much of an issue this area of the hotel tech stack is.

7. Any OTA-replacement through disintermediation, must still end up being connected to a hotel, either through a dedicated or ad-hoc pipe - this will all continue to be managed by SDR, as it makes no sense for hotelier to bypass SDR and DIY this. I expect that SDR would would appropriately react to any moves around disintermediation and find news ways of connecting to newly created OTA’s such that SDR does the integration once, and all hotels get access to that via Smart Distribution and Channels Plus

8. Similarly, the OTA's themselves could theoretically bypass SDR via AI agents, but then we go back to today's 1 OTA to a gazillion properties big and small and each property has 1 pipe per OTA - you would essentially unwind everything SDR has done to date. I can't see a business case for the OTA's doing this at all, even with agents, for the exact same reasons as in point 6. For OTA's, they only have 1 pipe into SDR and SDR takes care of everything else on the hotel-end. To undo this just because they have an agent to do this, doesn't make sense to me.

From an AI Productivity standpoint, I expect SDR to continue to use AI to mine its Data Intelligence platform and continue to find ways to add new capabilities that will add value to hoteliers, boost internal development productivity etc.

It feels that SDR will absolutely benefit from AI rather than be threatened by it. And it has not been standing still, doing nothing. I have every confidence in Sankar’s leadership that SDR will be AI-ing everything they possibly can and as fast as they can.

Discl: Held IRL 3.17% and in SM

Super pleased with SDR’s result today. In pre-Ai-mageddon times, this would have lit a rocket under SDR’s price, but I’ll take the ~9.5%+ rise today - it beats more red any day.

Not convinced AI-mageddon is done yet and the price will continue to drift, so am not in top up mode yet, but hell SDR is absolutely staying in my portfolio as a high-conviction holding.

SUMMARY

- Essentially, almost, if not all metrics, operational and financial grew at least on-trend - too many metrics to list!

- Underlying EBITDA was up 134.4% YoY, and was up 36.3% HoH

- Reported EBIT improved by a sharp 64% YoY and 48% HoH - not yet positive EBIT, but it feels very close to that now

- Margins rose sharply - this was the standout for me, given that revenue continues to skew towards dilutive transaction revenue

- SDR is now scaling very nicely and the Smart Platform products are giving SDR the boost that it always said would happen

- Will deep dive the AI-portions of the pack as a separate exercise as part of my portfolio but I see no immediate issues

OVERALL

Smart Platfom momentum is clearly driving strong growth, more than doubling of EBITDA/reduction of EBIT losses and strengthening unit economics

KEY METRICS

Scaling nicely - Number of properties added, number of properties, transaction product uptake all grow slightly above trend - this is very reassuring

2,900 properties added to 53,000 vs 2,700 added in 1HFY25 and 2,900 added in 2HFY25

Transaction product uptake is accelerating YoY and HoH

SDR continues to target larger hotel properties following the pivot into this adjacent space 18-24M ago.

RECURRING SUBSCRIPTIONS, RECURRING TRANSACTIONS, ARR

Nice on trend revenue growth in both Recurring Subscriptions and Recurring Transactions

ARR jumped sharply YoY, and that acceleration continued HoH

This revenue expansion is broad-based and across all regions globally

Of note is the America’s where travel spend has clearly been impacted by the Trump regime - growth momentum has sustained across the last 12M

SDR’s revenue transition from Recurring Subscription revenue to Recurring Transaction revenue continues to progress in a steady trend, driven by the Smart Platform products

ARR GROWTH, ARR REVENUE GROWTH

YoY ARR Revenue Growth, Organic was on trend

YoY ARR Growth, Organic, was above trend

Growth momentum has absolutely sustained

ARPU

Very nice on trend rises in Subscription ARPU, Transaction ARPU and overall ARPU

PROFITABILITY

Sharp improvement on EBITDA, Underlying EBITDA, Reported EBIT, both YoY and HoH, at significantly higher growth rates than the growth in Revenue - a clear sign that Operating leverage is really kicking in

GROSS MARGINS

Transaction GM will always be lower than Subscription GM, and the expectation is that Group GM will gradually dilute as the % of revenue increasingly skews towards the lower GM transaction revenue - the GM trend against this narrative is looking much more positive than would be expected from the narrative

Transaction GM rose sharply HoH and YoY, contributing to a very healthy increase in Group GM of 1.5% YoY and 2.3% HoH - this is really impressive

These gains show that scale, operating leverage is kicking in nicely

Management is also saying the higher margin Smart Platform initiatives, implementation of AI tools and the cycling of short term new customer incentives have contributed

This also makes sense in terms of where $ is being spent

UNIT ECONOMICS

LTV/CAC is trending up very nicely, and accelerating

RULE OF 40

Translating into accelerating Rule of 40

OUTLOOK

No real change towards the medium term 30% revenue growth in the medium term, but the language is becoming increasingly more bullish as evidence becomes clearer.

Discl: Held IRL 4.80% and in SM

Keeping a close watch on the SDR chart as the position allocation drifts below the ~6% allocation I would ideally like to be holding.

The 5.64 to 5.95 support zone has held up very nicely since late Nov 2025. This is a rather interesting technical zone as it is at the confluence of 3 "usually-strong" support factors:

- Medium-term support/resistance going back to March 2024 and prices bouncing up from this zone since late Nov 2025

- Rectracement from the previous uptrend move is around 50% on no adverse news - quite a bit of froth should have been taken out in the process

- The 200day Simple Moving Average is hovering around 5.63

With these 3 factors occurring at roughly the same level, the theory suggests that this may be a reasonable place to top up ...

If this area does not hold, then the next support looks to be ~5.45, from which the last gap up occured following the FY25 earnings announcement in late Aug 2025, failing which, 4.81 to 4.92.

Earlier this week, I initiated a 6% position in RL in $SDR for $5.95 (funded by exiting my remaining holding in $RUL).

I originally took a smaller position (3%) in Feb this year; however, as is sometimes the case for me with "new holdings" as I got deeper into learning about it, the conviction I thought I had wobbled and when presented with a short-term profit of 30%+ and a need to allocate the funds elsewhere on the day of the FY25 results, I “bottled it” and exited. (This was not an intended short term trade, I simply doubted the basis on which I originally entered, and changed my mind!) However, I’ve used the time on the sidelines to reconsider the proposition and today I have a clearer view as to what I am doing!

For a more complete write-up of $SDR, particularly since the FY25 Results in August and the Investor Day in September, I refer to excellent straws by @jcmleng which includes helpful analysis. That work allows me to be more selective in my write-up here.

What is $SDR?

- An enterprise SaaS software business serving small/medium sized hotels and related accommodation (individual properties and small chains)

- Serves a truly global market, and is leader in its segment having already scaled to 50,100 customers in 150 countries for 250+million Room Nights annual. (This represents a global market share of only c. 5%.)

- While currently unprofitable, the business is at the inflection point and is expected to generate positive free cashflow in FY26.

- With 4 years of operations as a listed company, the operating economics including operating leverage are clear. (That said, a strong FY23 benefitted from the global re-opening of international tourism, so the results folllowing IPO must be understood in context,)

Leadership

- CEO Sankar Narayan joined in 2019 from $XRO.

- At $XRO he learned how to run an international SaaS company as CFO and Chief Operating Officer.

- I rate Sankar very highly.

Market

- Global, small and medium size properties, often independent operators, single properties or small chains.

- Most of its customer base are relatively immature in procuring software.

- Of those who have invested in systems, many have multiple, dated systems that lack integration (both within the property as well as externally to the increasingly-important online travel agents (OTAs)). These require manual interventions and support, and many properties are now looking to invest in next-generation products, including functionality which was hitherto only accessible by the larger chains.

- Quantifed, the global TAM is anywhere from 0.3% to 1.5% of the industry's Gross Booking Value of close to $1,000bn.

The Opportunity

The key chart I am focused on is the following one from the recent Investor Day.

New customer acquisition has and continues to drive subscription revenue growth at low double-digit percentages annually.

More recently, the development and launch of a suite of “Smart Products” is adding volume-based transaction margins, where $SDR clips the ticket on specific, value-adding transactions for clients.

As @jcmleng highlighted following the recent AGM, this chart should be read together with this insight from Sankar's address at the AGM.

“We are moving beyond the role of a channel manager to become their central revenue platform - the unified interface where revenue decisions are made, executed, and automated."

Historically, most subscription revenue has been driven by Channel Manager, which connects a property's vacant room inventory to online travel agents (OTAs) that that act as channel partners. (Think Hotels.com). $SDR’s products are dynamically integrated, maintaining the inventory/availability live across multiple platforms. Without the use of a platform like $SDR (or the various other competitor offerings available) this has traditionally been a significant pain point for property managers.

Until recently, $SDR’s revenue has grown primarily as new properties subscribed to the product.

However, over the last 3-4 years, $SDR has been developing a suite of Smart Products, which include increased transaction revenues, where $SDR clips the ticket for activity in each of its Smart Distribution, Payments, Channel Optimisation, and Revenue Management modules.

The "Smart Platform" was launced in earnest in FY25. The chart above shows how in the last few years, the transaction-driven component of revenue is growing more rapidly than the growing subscription base. And it is very important to recognise that it is still early days in rolling out the Smart Platform to customers, as the following chart indicates.

The FY25 result is only starting to show transaction revenue contributions from “Smart Distribution” and even less from “Channel Plus” (C+). In fact, at Investor Day, $SDR told us that 5,000+ properties have contracted C+, which is around 10% of existing customers. Reportedly, over 500 customers are signing up per month ( 1% or 12% annually).

Smart Channel management takes on more of the operational tasks of managing the relationship and room availability and promotion process with the OTAs. $SDR can do this more effectively and efficiently than a property manager, because the process is automated in the $SDR software. Instead of the flat subscription fee that hotels have historically paid for the standard Channel Manager integration into the OTAs , the Hotel only pays for the incremental value added by the OTA bookings in the Smart Platform, and in return, $SDR takes a transaction fee.

The roadmap chart above is important when we considered how both subscription and transaction revenues are evolving, shown in the following chart. This shows that transaction revenues are growing much faster than subscription revenues. However, the growth rates for both are clearly declining.

But taking together the Smart Platform roadmap chart and Sankar’s comment at the AGM, together with his oft-stated target that revenue growth will re-accelerate to 30% in the medium term, it is clear that $SDR are confident of the value the Smart Platform will capture.

In fact they’ve quantified this. They believe that based on the subscription platform and early transaction capabilities, $SDR currently captures 0.3% of its customers Gross Booking Value (GBV). For customers deploying the full Smart Platform suite, $SDR believe this can increase to 1.5% of GBV – a 5x revenue growth opportunity from within the existing customer base.

So, it is central to my thesis that in FY26, as we come to see a full year of C+ and Smart Distribution penetrating the existing $SDR customer base, that Transaction Revenue growth will accelerate.

But as Sankar said at the AGM, this is just the start. The real game changer is once Dynamic Revenue Plus (i.e., automated revenue management) kicks in, starting in FY26, and then building from FY27 onwards. Dynamic Revenue Management is something the large hotel chains have been doing for many years. However, it is a capability that small / medium-sized operations have yet to embrace ("80%" of hotels have not adopted a Revenue Management System as of early 2025).

As a global market leader of software for independent and small chain operators, $SDR is positioned to now capture this opportunity with the Dynamic Revenue Plus (DR+) offering, clipping the ticket along the way.

So, What’s the Track Record in Capture Transaction Revenue Opportunity?

This sounds great, But where’s the evidence $SDR can achieve this?

The chart below shows just how successful $SDR has been to date in selling its transaction revenue generating products. This growth is only now starting to include $SDR bringing "Channel Plus" and "Dynamic Revenue Plus" into the existing, growing customer base.

There’s a lot more detail about the rollout plans for the Smart Platform in the Investor Day pack, as well as why each module will deliver value to customers.

Before moving on to my valuation, I do believe that with the launch of Smart Platform in FY25 and the early adoption evidence, we will see an acceleration of transaction revenue in the years ahead.

However, from the analysis I have done, I am not convinced that $SDR will get back to overall 30% annual revenue growth. However, I do believe that $SDR will do significantly better than the market is currently giving credit for. Hence the investment opportunity today,

The valuation that follows provides a framework for me to track progress over the next year or two. I believe it shows that at $6.00, $SDR is a good buy.

Valuation

First, I am NOT going to assume that $SDR can achieve Sankar's 30% revenue growth vision. That would be an UPSIDE BULL CASE to what I am modelling.

The model projects EPS growth out to 2030 – the timeframe of the Smart Platform rollout.

I build the revenue model in two elements:

- Subscription Revenue: I assume scenarios of Subscription Revenue growing at 9%, 11% and 13% annually, delivering a constant Gross Margin that expands progressively from 86.0% in FY25 to 88,0% in FY30,

- Transaction Revenue: scenarios of 20%, 25% and 30% annual growth are assume, with a flat Gross Margin of 33%.

Taken together the combination of revenue scenarios delivered FY25 to FY30 Total Revenue CAGRs from 13.7% to 20.6% - still a far cry from Sankar’s aspirational 30%!

Annual Opex Growth (including D&A) vary across scenarios from a low of 6% up to 9% (underlying Opex growth was 0% in FY24 and 7% in FY25). I’ve matched the higher Opex Growth scenarios to higher revenue growth scenarios, assuming that these will related to more aggressive customer acquisition strategies and platform development investments. Overall, I think these are reasonably prudent scenarios, given the operating leverage presented in the FY25 results, showing a clear trend over that 5 years since FY21.

Finally, my model includes several constant parameters as follows:

- Finance Costs/Revenue = 0.5% (assumes $SDR maintains zero long term debt)

- Tax Rate = 30%

- Annual Growth in Share on Issue = 1.2%

- Discount Rate 10%.

FY30 EPS was calculated. Given that in FY30 the modelled EPS growth rate ranges from 60% - 67%, I’ve applied P/E ratios in FY30 of 45 (blue), 55 (orange) and 65 (green) – shown by each of the curves graph below.

The implied valuation at the start of FY26 is shown in the graph below.

From this, my estimated valuation is $8.10 ($4.50 - $12.00).

Given that $SDR is still unprofitable today, the uncertainty in the valuation is necessarily very wide indeed. However, I am comfortable that at an entry price of $5.95, the assumptions I have used generate a good asymmetry with even my uppermost scenarios being well short of the CEO’s revenue growth goals.

As ever, I’ll will reconsider the various assumptions in my model with each future report. However, on this basis, I was happy to buy $SDR on Monday of this week.

When I Would Sell

For my thesis to remain on track, I need to see:

- Continued new property additions, at minimum high single digit % growth annually (allowing for some pricing uplift).

- Transaction Revenue growth needs to re-accelerate. It certainly cannot continue to decline as we get further into the Smart Platform Roadmap execution.

- Cost control must be maintained - although there is some headroom for a more aggressive customer acquisition strategy.

- Low historical churn levels need to be maintained.

A significant deviation on any one of these metrics would require a fundamental revisiting of the thesis and could be a thesis-breaker.

I’d also like to see Sankar remain in post. However, with the strategy set and the product set built, this is a business that can now be executed by any competent operator, IMHO.

Disc: Held (RL 6%)

Discl: Held IRL 5.10% and in SM

SDR is looking to have entered a nice top up zone for me:

- Approaching the 50% retracement level from the recent run up at ~5.69

- The 5.64 to 5.95 is a medium-term support/resistance area that goes back to March 2024

- The 200 SMA line is hovering around 5.46, providing the next downside support

- Thereafter 5.15 is the 61.8% retracement level

Discl: Held IRL 5.72% and in SM

Had a quick look at the SDR FY25 AGM material. It was a good opportunity to sit back and reflect on the journey thus far (super-pleased) and where this is all heading (north-ward bound!).

The one significantly misunderstood aspect of SDR is that it is NOT a channel distribution manager but a central revenue platform manager. Very pleased that during the FY25 results and the recent Investor Day, management has used more decisive and precise language to articulate this sharp pivot in positioning - this continued in the CEO address, highlighted below.

KEY THEMES FROM ADDRESSES

The SiteMinder team is delivering: “We are delivering for our investors, achieving a strong financial performance headlined by accelerating growth, improving unit economics, and critically, profitability, with both underlying EBITDA and free cash flow positive for the financial year”

On AI:

“We are not just participating in this shift; we are defining the future of our industry”

On FY25:

“It was a year defined not just by our strong financial achievements, but by the successful execution of our Smart Platform strategic plan”

“FY25 was a year where the travel industry faced volatile and challenging trading conditions buffeted by geopolitical conflicts and policy pivots. Against this backdrop, SiteMinder managed to deliver robust growth and momentum .... This acceleration is a powerful endorsement of the resilience of the business, our strategic product initiatives and the growing value hoteliers find in our platform”

“Our enhanced operating model provides the healthy, self-sustaining bedrock for our continued expansion, ensuring that our growth is fully funded by our own success”

On the Smart Platform:

“By successfully executing the Smart Platform strategy, SiteMinder is leading efforts to address critical challenges facing hoteliers, and redefining how the hotel industry manages revenue and guest acquisition

“We are moving beyond the role of a channel manager to become their central revenue platform - the unified interface where revenue decisions are made, executed, and automated.

On the opportunity ahead:

Our current annual recurring revenue unlocks approximately 0.3% of the $85b of gross booking value we facilitate. This is a very small fraction of the value we create for our hoteliers. However, when we estimate the potential value unlock at full product attach - meaning customers adopting the full suite of Smart Platform tools - that figure rises to over 1.5%. This is a significant revenue opportunity simply by deepening our relationship and value delivery to our current customers. This is an organic, high-margin, and a greater share of wallet from additional product adoption.

Outlook and Trading Update:

“ ... the positive momentum from the end of FY25 has continued, with ARR growth (on a constant currency and organic basis) tracking in like with the rate achieved in FY25 (27.2%) - reinforcing the stability and resilience of demand across our platform”

Only picked up 2 new slides, worth pointing out:

Good summary of the momentum in play across the SDR business

And the opportunity ahead - the Smart Platform rollout is really only just beginning.

Chart Review

The share price made another all-time high today, peaking at $7.96. While I think the market is taking notice and becoming increasingly bullish, the price does feel somewhat exhausted for now after the post FY25 results re-rating. I do not expect it to do too much other than bounce around at this levels and retrace a bit - not a bad thing to take some froth out of the price ahead of the 1HFY26 results.

Discl: Held IRL and in SM

Very pleased to see SDR make a new all-time-high price of $7.85 today, surpassing its previous all-time-high price of $7.77, which was achieved on the day it listed on 9 Nov 2021. It has never seen this level until today, 3 years 11 months-ish later.

The price did not have sufficient momentum to close above $7.77, settling at $7.72 instead.

It sure has been a bit of a journey ...

Since the FY25 results pop, the re-rating has been rather orderly and textbook-like. Probably due for a bit of consolidation and thus expect the price to move sideways a bit, quite possibly down to ~$6.60-ish, which would be very healthy for the price thereafter.

Business-wise, SDR is only at the start of the Smart Platform journey, so will be letting this run for quite some time ...

Discl: Held IRL and in SM

Had a good look at the SDR Investor Day Presentation from 23 Sept 2025. It really annoys the hell out of me that as a retail investor, I can’t seem to participate in any of these SDR sessions ...

It is a large pack of slides intended to give investors a deeper understanding of the Smart Platform capabilities, the problems they solve etc. Having had some previous Reservations and Hotel IT systems and operations background, these capabilities make a lot of sense and is very exciting to see.

SUMMARY

There are 6 key themes that emerge from this very software-functionality driven slide pack:

- There is a sharp pivot to positioning SiteMinder as a “Revenue Management Platform for Hotels” - this really makes sense to more sharply differentiate SDR’s capabilities and value add, and allow SDR to pull away from being categorised as a “hotel distribution system” - it should now be clearer that global distribution is only 1 of many SDR’s capabilities

- Introduction of the concept of a “Revenue Flight Deck” - an integrated experiencing unifying intelligence, revenue management and distribution

- Better clarity on the problems that each Smart Platform capability is intended to solve and the value this brings to hoteliers

- The huge volume of very hotel-related data that SDR has and continues to collect, the “SiteMinder iQ” Data Lake that stores and manages this data and how the data is then leveraged to improve internal operating efficiencies and the embedded in the SDR products to enable better dynamic predictive/forecasting capabilities for hoteliers.

- With the Smart Platform, SDR is adding transaction revenue at subscription-like margins.

- Unit economics are getting stronger - Lifetime Value is rising, Cost of Acquiring Customers is falling as there is minimal incremental cost to upsell

MY TAKEAWAYS

The harder pivot towards Revenue Management is long overdue. To badge SDR as yet another global hotel distribution platform is to misunderstand SDR’s value add to the hotel industry across the continuum of hotel size

I get the very clear sense that SDR is now in scaling mode with very attractive economies of scale ripe to kick in given the already large base of customers, a significant portion, if not all, who can absolutely benefit from the Smart Platform capabilities

The real SDR journey is now truly beginning ...

SUMMARY OF SMART PLATFORM PRODUCTS

DATA AND AI

Nothing fancy with the SDR Data/AI strategy - it makes sense. SDR has significant data capability, which is is looking to directly monetise:

- $85b+ of Global Booking Value

- 130m+ reservations per annum

- 50k hotels in 150 countries

- 2 year forward rate plans, with full property booking insight

AI is then used on data accumulating in the Data SiteMinder iQ Data Lake to (1) drive efficiencies across operational functions (2) embedded in SDR’s products to drive additional customer value - both adding to the velocity of the flywheels of efficiency and value.

Next generation hotel clustering techniques - the practice of grouping properties most comparable to your own to shape commercial strategies

Leverage AI to deliver statistically rigorous forecasting tools for hoteliers - enable better demand forecasting

GO-TO-MARKET

This brings out the typical lifecycle of the customer, the scaling opportunity ahead with the Smart Platform products and the economies of scale benefits - there is a lot to like with this.

Discl: Held IRL and in SM

Bailador took some nice profit with the sale of ~3.46m SDR shares, ~25% of its holdings of SDR

Post the sale, BTI still holds 75% of its SDR holdings

Market seems to have absorbed the sale very nicely with the share price moving sideways and staying above both the 7.20 support line and the medium term uptrend line, despite the heavier-than-normal volumes - a really encouraging sign of continued price strength.

Nice to see a sharp, detailed, get-stuffed, response from SDR to the Speeding Ticket it received.

Since the re-rating, the price has consolidated in a nice textbook flag pattern, with the all time-high intersecting with the long term uptrend line at ~7.03 up ahead. Expecting the price to go sideways between ~6.40 to 7.03-ish for a while.

Discl: Held IRL and in SM

Discl: Held IRL and in SM

SDR Things To Focus On

Pre-reviewing the results, I listed these 6 questions to answer, followed by the answers:

- Is revenue growing - dollars, ARR, ARPU? Absolutely - a decent noticeable acceleration in 2HFY2025

- Are the Smart Platform products contributing to growth? Hell yeah .... ! Big Tick

- Was there progress on LTV/CAC? Yes, improvement of 0.8x to 6.2x, driven by rising Customer Lifetime Value (LTV) vs flat Customer Acquisition Cost (CAC)

- Was there progress on Rule of 40? Yes, 3.9% increase to 21.3%

- Was there progress in the path to profitability? Absolutely - 2 consecutive Half’s of Positive Underlying EBITDA, EBITDA 2H jumped HoH (1H: $207; 2H $6,704) resulting in SDR’s achieving the target of full year Underlying EBITDA positive in FY25 $7,052 - Big Tick

- Was there progress to positive FCF? Yes, Net Cash from Operations up sharply YoY from $14.4m to 23.6m, Cash Burn fell YoY from ($10.8m) to ($7.6m), cash balance $33.4m, need to peel FCF report more

TLDR SUMMARY

- Cracker of a result all round

- My 1H commentary was “Thesis is very much intact. 2HFY25 should be more interesting as rollout of the 3 Smart Products will be in full swing and the impact of accelerating revenue should be more pronounced.” - this has now played out very nicely

- Smart Platform products are now contributing to revenue and revenue acceleration from 2HFY25

- Strong continued momentum on all operating metrics - ARR, New Property Additions, No of Properties on the Platform, Transaction Product Uptake, ARPU

- Market concerns around slowing travel discretionary spend does not appear to have materialised - revenue growth was strong in all regions

- Translated into strong Revenue Growth across both Subscription and Transaction Revenue

- Margins have improved: Subscription 86.4% (FY24: 85.1%) and Transactions 33.7%, (FY24: 33.7%), Overall gross margin has fallen to 66.3% (FY24: 66.5%) as expected, due to the shifting revenue mix of 62% Subscription: 38% Transaction (FY24: 64%:36%) - very healthy

- Translated into a jump in EBITDA in 2H, and the first full year of Positive EBITDA and Underlying EBITDA

- And improved Free Cash Flow

Chart Review

Market has responded positively, but there is long-term resistance at ~7.03, which goes back to post IPO days of Dec 2021 as well as the long-term upward trend line, both converging at around the same levels, which has limited the pop.

Expecting the price to now bounce sideways around the ~6.40 to 6.50 levels, while the analysts re-crunch the numbers.

Action

None - already fully allocated

This is a long-term high-conviction hold as the thesis is only just starting to play out and need to give management time to build the growth momentum in the next 1-2 years.

--------------------------------------------

Attaching my detailed commentary for anyone interested in the detail:

Financial and Operating Metrics

- ARR has accelerated - sharp jump in 2H, ARR Growth Organic now 27.2% (1HFY25: 22%), driving Revenue Growth 19.2% (1HFY25: 17/2%)

- Significant jumps in Transaction Revenue ARR Growth and Transaction Revenue growth - SDR’s focus to monetise transactions flowing through the platform are now paying off

- Transaction ARR growth of 48.3% YoY Organic is running significantly ahead of revenue growth as the scaling of the Smart Platform initiatives kicked in towards the end of FY25

Strong continued momentum in (1) New Property Additions (2) No of Properties on the Platform and (3) Transaction Product Uptake

Continued focus on penetrating larger hotel properties - this was not SDR’s original customer base, but is now becoming significantly more important as SDR monetises Gross Booking Value on the platform.

Which drives continued ARPU increase momentum:

And translating into continued HoH Revenue and Annualised Recurring Revenue growth, respectively

Rate of revenue growth in 2HFY25 has noticeably increased - a 14.8% jump HoH vs fully year increase of 17.7%.

Revenue growth has driven profitability with 2 consecutive Half’s of Positive Underlying EBITDA, resulting in SDR’s achieving the target of full year Underlying EBITDA positive in FY25.

3.9% improvement in the Rule of 40

0.8x improvement in LTV/CAC, driven mostly by Customer Lifetime Value increases, with Customer Acquisition Costs remaining quite flat.

Regional Performance

Revenue growth was strong across all regions - debunking market concerns about slowdowns in travel-related spend, a discretionary expenditure, as cost of living pressures kicked in during FY25

- All regions grew in excess of 20% Organic in 2HFY25

- APAC and EMEA accelerated HoH reflecting resilient travel trends (perhaps the pivot away from the US as a travel destination) and contributions from the Smart Platform initiative

- America’s sustained HoH momentum - contributions from the Smart Platform initiatives offset the moderation in general travel conditions - the Trump effect?

This resilience augurs well for FY26 as the global interest rate cycle moves more firmly towards an easing bias in FY26.

Smart Platform

This is a really good slide which emphasises a point which I think the market still has not got clearly - SDR is not a global room distribution platform alone - it is much more than that.

SDR’s Smart Platform has deeply embedded capability in (1) Revenue Management - previously the domain of large hotels with dedicated headcount to directly manage revenue and (2) Guest Experience ON TOP OF (3) the more traditional “Guest Acquisition” capabilities - a very nice term for the Booking Engine, Global Distribution, Channels Plus capabilities

The monetisation engines would reside primarily in the Guest Acquisition and Guest Experience areas

Late FY24 into all of FY25 was about building out the Smart Platform capabilities and then deploying them to SDR’s customer base - evidence from 2HFY25 is that meaningful revenue is now coming through from these recently deployed capabilities - this was what the market needed to see to believe.

Cash Flow Position

Cash flow performance looks good at face value but need to peel this a bit more, especially the adjustments

- From the cash flow statement:

- Net Cash from Operating Activities was significantly up YoY - FY25 was $23.6m vs FY24 $14.4m

- Net Decrease in Cash fell to FY25 ($7.6m) from FY24 ($10.8m)

- Cash Balance is $33.4m, vs FY24 $40.2m

- No concerns on cash

OUTLOOK

More of the same FY25 in FY26

No change to the general medium-term 30% revenue growth target

Interesting, although I do not fully agree with the point around "room night demand heavily driving revenue". That "hotel room distribution" boxing of SDR's revenue is, in my view, an overly narrow one. The revenue base has platform subscription revenue, revenue management capabilities via the Smart Platform, payments-driven revenue etc.

Sentiment on SDR clearly has been hit by the caution around travel discretionary spend.

Very eager to see how SDR has gone this half amidst that caution, hopefully offset by the increasing impact of the Smart Platform products being rolled out and the ARR that that should drive.

Discl: Held IRL and in SM

The SDR price has recovered nicely and is now sitting above the long-term 200 SMA, clearing 3 resistance areas along the way ...

Per Macquarie - this is in regards to the travel industry for CTD/FLT. Most of this seems positive read through in terms of conditions. Hopefully offsets weakness in the US from Trump.

Volumes better than feared. Since peak tariff uncertainty in Mar/Apr, the market has been concerned about overall volumes and activity in the US. US volumes appear to be holding up better than feared, with 2QCY24 TSA data down only -0.9% YoY. Subdued inbound leisure volumes will likely be a headwind, with inbound volumes from Canada/Mexico down 13%/7% in June. Across other regions volumes are solid, outside the timing of Easter shifting some travel to April.

• Airfare deflation still a headwind. Although the pace of airfare deflation has slowed, it remains a headwind and is likely most severe in the US (domestic fares down -3% in May). US airlines have been rationalising capacity to reflect the demand outlook. Combined with softer traffic, this has driven an increase in airfare deflation. In ANZ, we expect domestic airfares to grow at inflation and international to deflate mid-single digits. Continued international deflation is a drag on TMC's commissions and overrides, but appears to be stimulating volumes.

• Hotels and accomodation. Recent industry calls with European operators indicated industry conditions remain strong. Although conflict in the Middle East has caused some disruption, it appears to be isolated to specific countries, and concentrated around major news events.

Given the sizeable lots, this looks like Australian Ethical Investment has upped its stake in SDR by 1.27% between 3 Apr and 6 May, to now hold 6.31%. Can’t hurt!

Discl: Held IRL and in SM

The following few SDR slides from the Macquarie Conference caught my eye:

Firstly, the Trading Update. Acceleration of the ARR sounds promising ..

This was a simple slide, but helps clarify where SDR plays between the Hotel and the Global Travel Distribution Channels

Lastly, 2 slides on its resillience. Presumably this is in response to market concerns that discretionary travel could be hit when the proverbial hits the fan once tariffs kick in, talk of recession etc.

One of my key thesis drivers when I first looked at SDR was that it more than survived Covid when the travel industry was as decimated as could be - my thinking than, and still remains, is that if it can survive Covid, it should be able to survive anything thereafter ...

The FY25 SDR results will be extremely interesting as it will reveal the traction from the rollout of Smart Platform products vs global concerns on recession, cutback of discretionary spend and how that impacts revenue and growth ...

Discl: Held IRL and in SM

Welcome to the SDR register, KKR .... a nice confidence booster which can't hurt.

Price has recovered nicely in line with the broader market. But will be interested to see how SDR travels through end-May/early June when tariff realities full bite and the Yanks reassess further discretionary spend like travel ...

Discl: Held IRL and in SM

Nice to see 2 Directors buying on-market into SDR's freefall. Looks like a staged action though - the volume is "coincidentally" around 10,000 shares. Probably small coin for them, but still 1 zero more than spare cash that I have. Definitely happier with them buying than selling!

From today's chart, looks like the selling has abated somewhat today, closing at $4.90, which was around where I thought it would find support. Whether it holds or not will be revealed in the next few days. But it is entering into my buy zone quite nicely now ...

Discl: Held IRL and in SM

Intelligent investor weighs on SDR bear case

Research Wrap

Little Aussie Tech stocks are having a moment. SiteMinder, an unprofitable business that helps hotels navigate the complex world of online travel agents, has a higher price-to-sales ratio than Booking.com, Expedia and Airbnb, all of which are profitable.

Even worse, the company is—perfectly legally—minimising its losses by taking some of its payroll off the income statement, which in the trade is called ‘capitalising R&D’. Strange but true: accounting standards mean companies now get to decide whether developer salaries in a software business are a cost or an asset ($).

Other than the growth, where is the Rule of 40 in this chart?

This is more expensive than, dare I say, Gentrack? I remember screening this before and the Price to sales of SDR is "through the roof"

Summarised the CEO's Speech and Preso from this mornings FY2024 AGM as I digest and internalise the information. The more I read about the Smart Platform Strategy, the clearer it is becoming.

I highlighted in bold italics, insights that either I had not picked up before or further crystallises the strategy, all positive!

Discl: Held IRL and in SM

SUMMARY

No new news, but more clarity on the Smart Platform Strategy, the components, progress and revenue impact

No change in guidance for FY2025 but 1QFY2025 looks to be tracking nicely on both subscriber additions, transaction product adoption and Smart Platform development progress

SiteMinder also expects to be underlying EBITDA profitable and underlying free cash flow positive in FY25

SMART PLATFORM STRATEGY

The centrepiece of our plan to build on our strong momentum is the Smart Platform strategy. Announced last year, the strategy is about making the strengths of our platform work better together so we can help our hotelier customers and partners generate more revenue.

The three pillars of the Smart Platform strategy work together to deliver more revenues for hoteliers and our partners.

The key initiatives of the strategy are focused on answering three questions:

Q1. SiteMinder has a large and valuable repository of data unrivalled in size, depth and geographical coverage. How do we make this data accessible and useful to our hoteliers?

Q2. How do we translate that data into actionable recommendations across not just pricing but other commercial levers as well?

Q3. How do we help hoteliers execute those recommendations with minimal effort?

This is about creating a unified revenue management experience, something that doesn’t exist in the industry today but operators are crying out for.

SMART PLATFORM STRATEGY PROGRESS

The team has made great progress on delivering the Smart Platform strategy with all three pillars – Dynamic Revenue Plus, Channels Plus and the Smart Distribution Program – either in pilot or having commenced their launch.

Dynamic Revenue Plus

We were pleased to launch Dynamic Revenue Plus in Australia and New Zealand last month.

Dynamic Revenue Plus provides our hotelier customers with proprietary insights and execution tools to optimise key commercial decisions and drive more revenue. The launch has received very positive feedback from our hotelier customers and industry partners.

Dynamic Revenue Plus will level-up early next year with the integration of pricing recommendations from IDeaS ahead of its global launch in March 2025. IDeaS is the industry’s most trusted revenue management system, and we are pleased to have deepened our partnership with them.

This is very exciting but it is just the start of the journey for Dynamic Revenue Plus.

Advanced capabilities are under development that will combine the latest in artificial intelligence with SiteMinder’s deep and comprehensive data assets, to deliver even greater revenue gains for our hotelier customers. I look forward to sharing more details of these capabilities in due course.

Channels Plus

Second pillar of our Smart Platform strategy and is focused on making it easier than ever for our hotelier customers to distribute their inventory.

In less than five minutes, they can sell their inventory to 30 participating distribution partners. Achieving the same outcome without Channels Plus would take weeks, if not months, and is practically impossible for most hoteliers to sustain.

Today we have more than 1,000 hoteliers and 30 distribution partners signed up for Channels Plus.

We’ve received strong interest from our customers and have received strong support from some of the world’s leading booking platforms.

From January 2025, Channels Plus will be a default inclusion for all new customers on the SiteMinder platform.

Smart Distribution Program

The third pillar of our Smart Platform strategy is the Smart Distribution Program.

The Smart Distribution Program will drive unprecedented collaboration between our hotelier customers and distribution partners to deliver win-win-win outcomes through enhanced connectivity, optimised set-ups and technology investments. The program commenced during the September quarter just passed.

IMPACT ON REVENUE

For SiteMinder the Smart Platform strategy represents more than just incremental revenue.

The strategy transforms our revenue model from one that is just hotelier-oriented and largely based on fixed fees, into one that touches other parts of the travel ecosystem and is increasingly focused on activity based fees. This will allow us to better participate in the success of our hotelier customers and partners.

The three pillars will meaningfully contribute to revenue at different times over the next few years.

The Smart Distribution Program will come first, and its contributions will be compounded by Channels Plus and Dynamic Revenue Plus. Together they will help us achieve our guidance for 30% organic annual growth in the medium-term.

TRADING UPDATE

While we are doing a lot of work to position the company for the future, we have not lost sight of the now and present.

The company has continued to perform well in the first quarter of the 2025 financial year:

- Net property additions are tracking ahead of last year with continued focus on larger properties which present attractive long-term revenue opportunities for the company.

- The adoption of transaction products continues to grow across incoming and existing customers.

- On the Smart Platform, we are progressing as planned with the commencement of the Smart Distribution Program.

- Channels Plus is on track for its full commercial launch in January 2025

- Dnamic Revenue Plus is progressing through its staged launch program with positive early industry feedback.

Our guidance is unchanged. We continue to target organic revenue growth of 30% in the medium-term, aided by contributions from the Smart Platform.

SiteMinder also expects to be underlying EBITDA profitable and underlying free cash flow positive in FY25, and make continued progress on the Rule of 40

I know people are keen on SITEMINDER but with every hot tip share spike there are shorters around the corner. Short interest spiked with recent price increase.

Bear - 20% Revenue growth slowing to 15%

Base - 25% Revenue growth slowing to 20%

Bull - 30% Revenue growth slowing to 20%

Discount rate lowered to 12.5% since operating cashflow positive milestone met.

SUMMARY

A very good all round operational result - very hard to find fault with it as the business appears to have fired on all CURRENT cylinders.

Smart Platform new capabilities are being progressively rolled out in 1HFY25 - sets the foundation for a good step up in revenue in 2HFY2025.

Focus is now increasing on larger hotel properties vs SDR’s earlier focus on small hotel properties - this opens up the TAM, is a good sign of growing product/platform confidence and will support future revenue momentum given the higher Gross Booking Value of larger hotels

Am very bullish as things are falling into place very nicely.

Thesis of SDR being the dominant platform in small and medium-sized hotels is very much intact and in play with the existing capabilities, and with the promise of more from the imminent Smart Platform capability rollout.

Market does not seem to have recognised this and prices have fallen to my top up zone of ~$4.90

Topped up today at $4.92 IRL and in SM, with dry powder kept on standby to further top up around $4.60, if prices fall to those levels.

Disc: Held IRL and in SM, High Conviction holding

Financials (all amounts and %’s are YoY comparisons)

Total revenue up 26.0% to $190.7m - while this is shy of SDR’s “medium term” goal of ~30% annual organic growth, it has grown at a fast clip and is before new Smart Platform capabilities are released.

- Subscription revenue up 18.8% to $122.4m, driven by a 13.8% increase in properties of 5,400 to 44,500 properties

- Transaction revenues up 41.2% to $68.3m, driven by strong Transaction Product Uptake which increased 41.2% to 26,300 products

- ARR is up 20.7% to $209.0m

- Revenue mix is shifting slowly in favour of Transaction Revenue, from 68% Subscription:32% Transaction to 64%:36%

- Revenue was earned more or less evenly across all 3 regions of APAC, EMEA, North America

Margins have been sustained:

- Reported margin - 66.7%

- Underlying subscription GM improved from 83.2% to 85.1%

- Underlying transaction GM moderated from 34.8% to 32.0% due to product mix, temporary expansion into new segments and acquisition channels - no concerns on this

Underlying EBITDA turned positive from FY23 ($21.9m) to FY24 $0.9m, importantly, this occurred in 2HFY24, reflecting the benefits of operating leverage and cost discipline

LTV/CAC continues to improve on a steep trajectory - 31.7% improvement from 4.1x to 5.4x

- Customer Lifetime Value improved 8.3% from $22,312 to to $24,130

- Customer Acquisition Cost (CAC) improved by 18.2% from $5,469 to $4,472

Rule of 40 performance improved 230%, from 5 to 17, reaching 21 in 2H

Operating leverage is kicking in as revenue increases - this is very evident in falling product Development Cost despite the intense focus on developing and deploying the new Smart Platform capabilities in the back half of FY2023.

Balance Sheet

Underlying FCF improved from ($34.0m to ($6.4m)

- FCF as a % of revenue improved from (22.5%) to (3.4%)

- FCF positive was achieved in 2HFY24, generating $2.3m or 2.4% of revenue

$72.3m in available funds, which includes $30.0m of undrawn debt facilities

3-Pillar Smart Platform Strategy

Clear evidence that the SDR platforms are being actively used

The industry is coming onboard, including the big Global Distributors

New capabilities appear on track for rollout in 1HFY25 - expect revenue to get a good leg up in 2HFY25 as a result

My notes on SDR's Appendix 4C and Trading Update today. I really like how things are panning out not only for FY24, but also what is ahead for FY25 ...

Disc: Held IRL and in SM

TAKEAWAYS

- Operating leverage and cost management is evident from the 4C, which should translate into improved EBITDA

- 2H Revenue of $99.0m, has increased $7.3m or ~8% from 1H revenue of $91.7m

- 2H Operational Costs of $86.6m has fallen $7.3m, ~7.7% from 1H costs of $93.9m

- Good solid growth across all metrics, but suspect it will fall short of 30% annual organic revenue growth in FY2024 - this 30% growth was positioned as a “medium-term” objective, so not achieving this in FY2024 should not be an issue so long as SDR demonstrates tangible YoY growth, which the 4C and Trading Update suggest, it has

- FY2024 into 1HFY2025 is the period where significant capability is being piloted, built/improved, ready for rollout throughout FY25 - Dynamic Revenue Plus, Channels Plus, Payment Solutions, Metasearch Manager, and the newly announced Smart Distribution Program - the rollout of these capabilities broadens SDR’s monetisation opportunities and hence, underpins the medium-term 30% organic growth target guidance

- The FY24 growth is thus all the more impressive as it does not include any revenue from any of these new capabilities

- Assuming the new capabilities are rolled out in FY25 as planned (and indications thus far that they are on track), FY25 revenue growth could be very interesting ...

Summary of the Updates on Key Metrics

SMART PLATFORM STRATEGY

Dynamic Revenue Plus

- Equips hoteliers with the ability to assess and react to changes in demand quickly and accurately - commenced pilot in Australia and NZ.

- Phased development is progressing as planned with the ANZ release on schedule for Q1FY25

- Entered into agreement with IDeaS to provide price recommendations for the product - 35-year track record in hospitality pricing, industry’s most trusted revenue management software - combines IDeaS pricing engine with SDR’s distribution execution capability and deep global and local intelligence to reset how hoteliers execute revenue management

Channels Plus

- Allows hoteliers to expand their distribution to multiple channels with ease and control

- General release remains on track for Q2FY25

- Pilot commenced in April, attracted interest from 25 distribution partners

Smart Distribution Program - Newly Announced

- 3rd pillar to accelerate and expand the revenue potential of SDR’s Smart Platform

- Designed to accelerate and expand the revenue potential of the Company’s Platform

- Secured support and commitment from key global distribution partners to jointly improve the distribution configurations of hoteliers through the Smart Platform to capitalise on significant opportunities to maximise revenue performance

TRANSACTION PRODUCT INITIATIVES

Payment Solution

- Extended into SIN and HKG, additional markets will go-live in FY25

- Work on introducing physical payment terminals, well progressed, pilot scheduled to commence in Q2FY25, followed by staged rollout from Q3FY25

Metaseach Manager

- SDR’s metasearch solution for the enterprise segment

- Entered pilot with strong interest from hotel groups looking to better manage their meta search campaigns

GUIDANCE

- Still targeting 30% organic annual revenue growth in the medium term, aided by contributions from the Smart Platform

- No change to financial guidance

- Underlying EBITDA profitable

- Underlying FCF positive for H2FY24

Good to know Aust Super is accumulating SDR, adding another 1%.

The Good

- Increase in positive operating cash flow to $4.9m for the quarter. FCF is still not quite positive due to investing cash outflows of $5.3m. Siteminder is trending well to meet their FCF target by the end of FY24.

- Operating expenses remain flat, so going forward, most of the top line growth should be going to the bottom line.

- $39.5m in cash available as the business reaches FCF positive. Cash balance should improve going forward offering a solid operational buffer for future R&D spend.

- 14 agreements signed on for Channel Plus which indicates there is a demand for the new product. Currently this is running in pilot for Q4FY24 so unlikely there will be any significant contribution from Channels Plus until H2FY25.

The Not So Good

- ARR is up YoY and the previous quarter but still down on Q1. It’s a similar story with quarterly revenue, which has been largely flat for FY24 and still down on Q1. For the company to be close to the targeted growth rate of 30% much of this will need to come over the next 2 quarters.

What To Watch

- Channel Plus and Dynamic Revenue Plus release as per target in Q1FY25

- Siteminder Pay Terminals rollout in H1FY23

- Updates on Little Hotelier Autopay and contributions to increase in transaction revenue.

Watch Status

- Unchanged. Slower growth QoQ but business developing opportunities for FY25 and beyond.

Valuation Status

- No Change

Following the post on SDR's 1HFY24 results earlier, here is the summary of the SDR 3QFY24 Appendix 4C. More of the same from 1HFY24 ...

Very excited with progress on the 2 new capabilities currently in pilot release ahead of 1QFY25 release as this will propel SDR's next phase of growth, in parallel to the ongoing growth in the current base products.

Discl: Held IRL and in SM

KEY POINTS FROM THE ANNOUNCEMENT

- Revenue increase driven by SDR’s metasearch offering, Demand Plus, driven by accelerated adoption and strong booking activity

- Net subscriber addition momentum continued from 1HFY24, focused on larger properties (vs the target market of small, independent hotels)

- Continued improvement in FCF - underlying FCF was ($0.2m), now only (0.4% of revenue) - accelerating throughout FY24 thus far - continuing benefits of sustained strong organic growth and operating leverage

- Liquidity remains strong at $72.2m

- No change to FY24 guidance - (1) organic revenue growth of 30% in medium term (2) underlying EBITDA profitable in 2HFY24 (3) underlying FCF positive in 2HFY2024.

- On track for mid-CY2024 release of 2 Smart Platform products

- Channels Plus:

- Signed up Trip.com Group to participate in the Channels Plus Program

- Channel Plus continues to gain traction - 14 distribution partners have signed up

- Channel Plus pilot commenced 29 April 2024, limited to 1,000 hotels, has drawn strong registered expression of interest from existing customers

- Dynamic Revenue Plus:

- Mobile App launched in March well received by users

Belatedly worked through SDR's 1HFY24 results and last week's 3QFY24 Appendix 4C after leaving it aside for about 6M.

The FY2024 slides is an easy read and tells the story very clearly SDR 1HFY24 Preso

Added notes taken during the 1HFY2024 call and a summary of the P&L and KPI's across the halfs, so that I can more clearly see the trend across half's rather than pcp.

SUMMARY

- This is a company that is firing on all cyclinders today, with new capabilities in pilot release now, which will drive the next wave of growth from FY2025

- Positive momentum and operational KPI’s all steadily trending in the right direction and improved on the pre-Covid 2019 trajectory - subscriber growth, across all regions

- Scale and leverage is clearly showing as revenue grows - unit economics continue to improve, LTV/CAC continues to grow, Sales and Product Development expense as a % of revenue continues to fall

- Underlying cash flow positive in 1HFY24 - on track to target of cashflow positive in 2HFY24

- Driving industry change via Smart Platform - the integration of Distribution, Intelligence and Revenue Optimisation, as the hotel industry is far behind airlines in yield management

- Smart Platform will provide the next step increase in SDR’s growth - good progress made in 1st 2 capabilities of Demand Plus and Channels Plus - due for release in 2HFY2024, will full impact to be felt in FY2025 - increases the moat

- Smart Platform will also see more transactional monetising opportunity for SDR by taking a clip of the gross booking value that goes through the SDR platform

- SDR is rapidly growing its base market with a huge TAM to go and in parallel, rapidly building new capabilities that will drive improvements in hotelier revenue via improvements in yield management

KEY POINTS FROM 1HFY24 INVESTOR CALL

- Comparison CY2023 against Pre-Covid CY2019 a better indication of performance as CY2022 was Covid-distorted - unable to sustain acceleration rates when compared to a distorted 2022, but underlying growth from CY2019 is ongoing

- APAC and Aust - higher growth pace, expect Asia to grow scale

- Subscription growth momentum - good pipeline and additions in 2M in CY2024, no slowdown

- Transactions held up better than most majors:

- GDS - big beneficiary of return of leisure travel post Covid

- Pay - on par with average growth rates

- Demand Plus - strong ability to drive activity and share of Gross Booking Value - strong in Jan/Feb

- LTV/CAC is 5.3x - higher than pre-Covid, LTV has expanded and CAC continues to moderate

- Channel Plus Partners - signed on Agoda and Hopper

- Agoda is either top 5th or 6th of global channels, strong in Asia and is very big

- Channels Plus takes away friction from inventory management

- Both sides have monetising opportunity - SDR, Hotels, Online Travel Agent

- SDR is one of the largest supplier of inventory to the majors

- Channels Plus creates new distribution channels, is not part of Demand Plus - complementary, not cannabilistic

- Channels Plus - hotel has 1 pipe which opens many distribution channels - removes inventory management friction

- Pilot in mid-CY24, impact will be seen in FY2025

- Revenue growth is driving leverage and scale

- Positive Underlying Cash Flow in Q1 and Q2

- Not looking at M&A

Discl: Held IRL and in SM

The Good

- Q1 revenue of $46.8m which annualise to $187.2m. This would be a 23% increase on FY23 and keeps management’s 30% YoY growth targets in range.

- ARR increased 10.7% QoQ to $191.6m which is just shy of my previous forecast target

The Not So Good

- Operational cash flow positive not quite achieved this quarter as per my previous target. “Underlying” cashflow has been reported positive when adjusting for “non-recurring” costs of ~ $800k. There have been cost adjustments in most of Site Minders announcements, which brings into question how “non-recurring” these are.

- Operational expenditure is largely levelled out, except for staff costs which continues to grow. Q1 did include an annual cash incentive of $2.4m, so this should come down slightly in Q2. Staff costs do remain as a watch point as they are the most significant expense for site minder.

- Cash down to $45m. There is still $31.3m of unused financing facilities, however it would be much more positive for the company if they can reach their FCF targets before having to draw on these.

What Status

What To Watch

- Introduction of Dynamic Revenue Plus and Channels plus mid 2024 as detailed by @jcmlengs post. Investor day announcement here

- Business metrics not reported for the quarter. Look for improvements across these in H1, particularly net subscriber additions as these were reported to have accelerated in Q1.

- FCF should be just shy of breakeven in Q2.

- Levels of investing expenditure to implement the new smart platform developments. Currently is ~$6m per quarter. Increases to the investing spend could potentially hinder the FCF targets. However ongoing development of the platform is required to drive growth in spend for the existing user base.

- Decrease in staff costs for Q2.

Went through the SDR Investor Day Presentation slide pack released yesterday 16 Oct 2023:

https://www.asx.com.au/markets/company/SDR

It was well worth spending the 25-30 mins working through the 78 slides to get a flavour of the 2 Smart Patform offerings targetted to be released in FY24 and the opportunity ahead to upsell within existing customers, over and above the signing up of new hotels.

Having had some past exposure to cruise ship revenue management and reservation systems, the offerings make complete sense to me. It solves some big problems, especially for smaller hotels that do not have extensive distribution and revenue management capabilities.

Very keen to see how the SDR customer base takes up these new offerings and the resultant financial impact in the coming Q's.

SUMMARY

- Strong uptake of SDR offerings across the 4 Global Hotel Industry segments

- Significant TAM remaining to chase

- Rolling out “Smart Platform” - sophisticated revenue management capability which converges distribution, intelligence and revenue optimisation to maximise hotel revenues

- 2 new offerings under Smart Platform:

- Dynamic Revenue Plus - real-time recommendation engine to help identify optimal commercial actions a hotelier can take in response to external events, intelligence etc. Address challenges in the lack of revenue management capability in small hotels

- 5 use cases showcased (slides 35-48)

- Channels Plus - capability to automatically connect distribution channels and hotel properties as they sign up to the program out of the box, eliminating today’s friction in many connections, agreements, connectivity configurations (slides 56-62)

- Commercial potential to deliver >10x ROI to hotels at 1% monetisation of FY23 GBV (Value of bookings processed by SDR)

- Previous guidance was reiterated - (1) target 30% organic revenue growth in the medium term (2) underlying EBITDA profitable and underlying free cash flow positive for H2FY24.

Discl: Held IRL and in SM.