Top member reports

Straws

Sort by:

Recent

Content is delayed by one month. Upgrade your membership to unlock all content. Click for membership options.

##Quarterly Review

stale

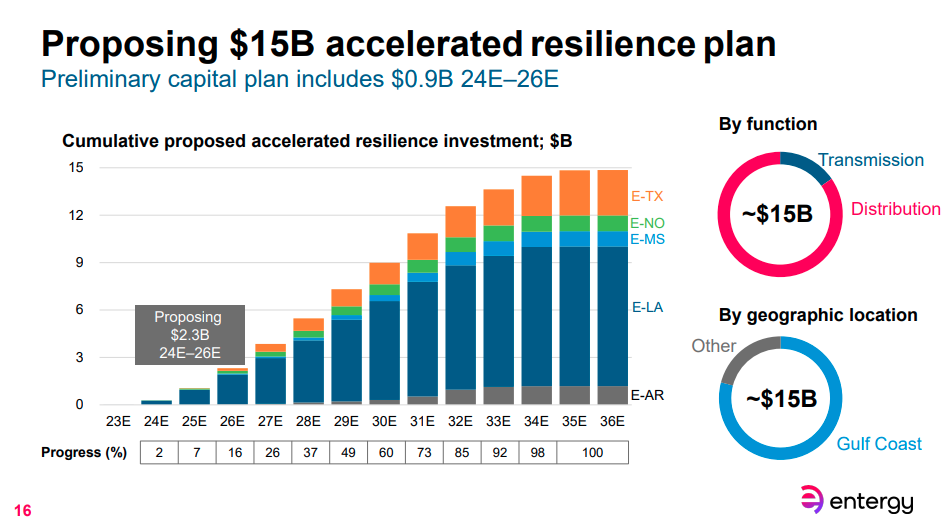

From a recent Entergy pres: