Consensus community valuation

I don't have a valuation for LYL because after a cursory glance, I'm not interested in spending any more time on it, but for what it's worth here's a few things that stood out.

18/02/26

The 1H26 result was no doubt a disappointment for me:

- Revenue: $174.5 million

- EBITDA: $29.6 million

- NPAT: $18.3 million

- EPS: 46.0 cents per share

- Fully franked interim dividend: 22 cents per share, payable on 2 April 2026

- Cash balance: $80.0 million as at 31 December 2025

- Updated FY26 guidance: Revenue of $370 - $410 million, NPAT of $37 - $41 million

- Increased project delivery volume expected in H2 FY26

- Webinar held at 12:00pm AEST on 18 February 2026

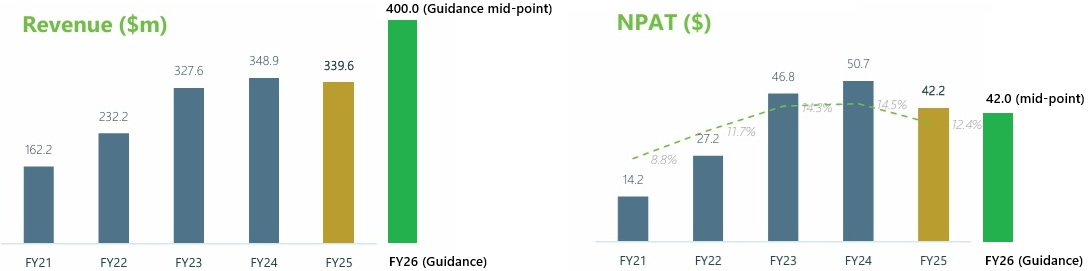

Historically, LYL management has been conservative with guidance. Previous guidance estimate was Revenue $390 million to $410 million, and NPAT $40 million to $44 million. FY26 revenue guidance has been downgraded by 2.5% on the midpoint, and FY26 NPAT has been downgraded by 7%. NPAT margins have softened and are now 10.5%.

After a somewhat disappointing half, management are expecting NPAT to improve in the second half from $18.3 million in 1H206 to $19.5 million in 2H26 (midpoint of guidance).

While revenues are expected to be a record high of $390 million (11.5% growth to midpoint from FY24, the last record) NPAT margins are expected to normalise toward 10% according to management. Makes me wonder if the Saxum acquisition has diluted margins and ROE.

To the future

LYL has a a strong order book with $415 million in committed contracts, while the revenue opportunity pipeline has also expanded to ~$1.3 billion.

Management said, “Overall demand drivers for Lycopodium’s innovative engineering and delivery solutions continue to expand, supported by the Company’s bespoke and modular engineering capabilities and expansion of our geographic footprint.”

Resources:

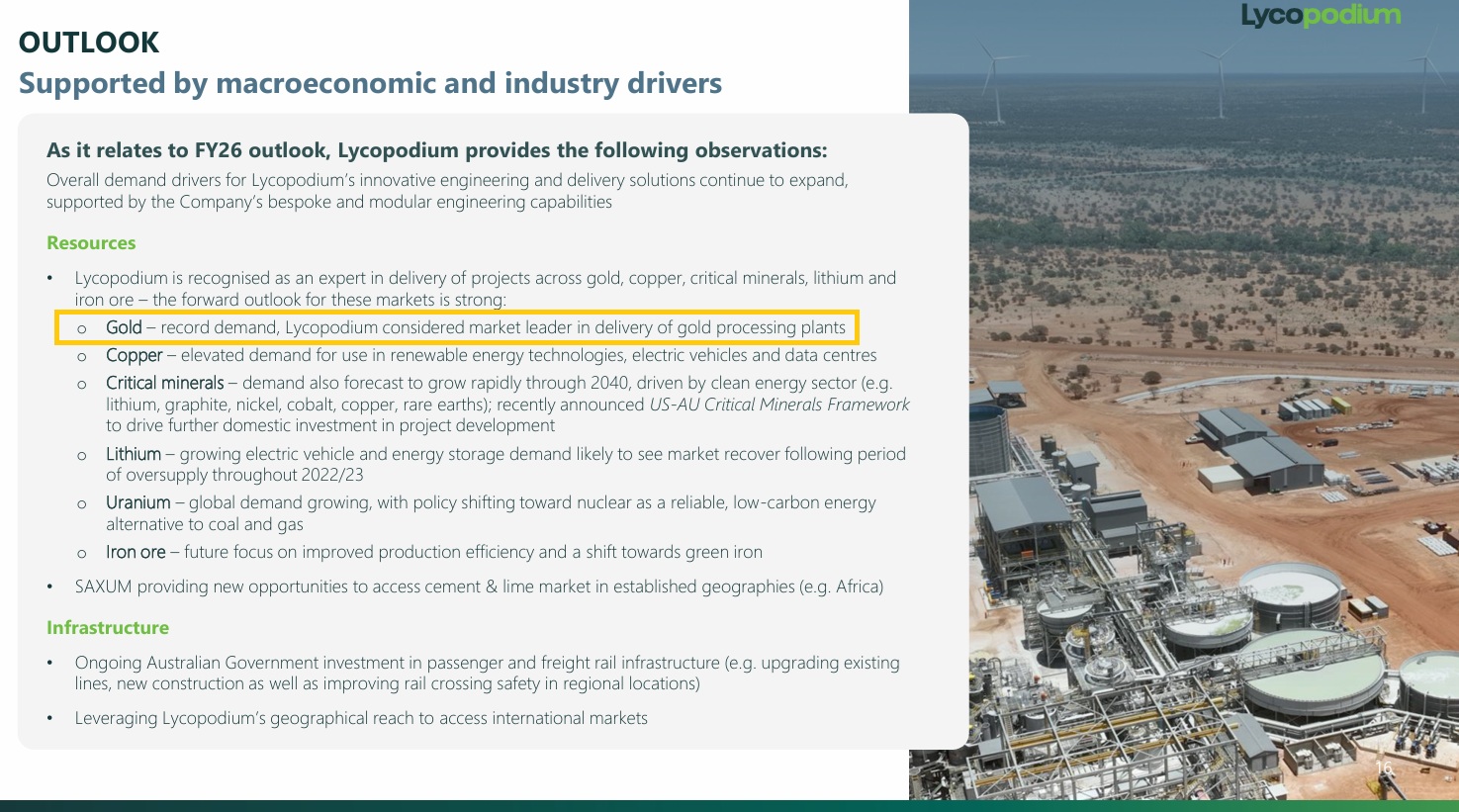

Lycopodium is recognised as an expert in delivery of projects across commodities where the forward outlook remains strong, including:

- Gold – robust demand, Lycopodium considered market leader in delivery of gold processing plants

- Copper – elevated demand for use in renewable energy technologies, electric vehicles and data centres

- Critical minerals – clean energy sector driving demand for key commodities, e.g. lithium, graphite, nickel, cobalt, copper, rare earths; US-AU Critical Minerals

Framework to drive further domestic investment in project development:

- Lithium – surging demand, driven by growing electric vehicle and energy storage markets, following recent supply imbalance

- Uranium– global demand growing, with policy shifting toward nuclear as a reliable, low-carbon energy alternative to coal and gas

- SAXUM providing new opportunities to access cement & lime market in established geographies (e.g. Africa) Infrastructure

- Ongoing Australian Government investment in passenger and freight rail infrastructure (e.g. upgrading existing lines, new construction as well as improving rail crossing safety in regional locations)

- Leveraging Lycopodium’s geographical reach to access international markets

Valuation

LYL reported a 3.7% increase in equity on FY25, now approx $3.96 per share on my calculations. I’m working on FY26 EPS of $1.00 per share (mid-guidance). That puts forecast FY26 ROE at 25.25% (not the 11.7% quoted in the presentation which has been calculated incorrectly. ROE should be calculated on annual NPAT/Equity, not half year NPAT/equity. Not the first time they’ve done this). With 52% of NPAT reinvested at the current ROE, and requiring a 12% return on investment (ROI) I come up with a valuation of $14.80 using McNiven's Valuation formula. I’m going to leave my valuation at $15 for now. Similar to my previous valuation, this might edge downwards at the lower end of guidance, and or upwards with higher guidance estimates.

Held SM and IRL (6.6%)

9/01/26

@Bear77 thanks for your straw. Re valuation I have always found it tricky to value. Management are usually very conservative with guidance. The latest update was in November as follows:

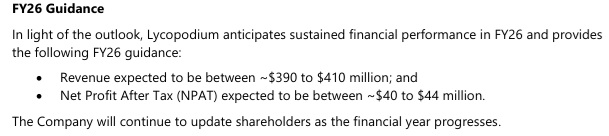

“Lycopodium Limited (LYL) has provided its FY26 outlook and guidance:

- Revenue expected to be between ~$390 to $410 million

- Net Profit After Tax (NPAT) expected to be between $40 to $44 million

- SAXUM integration advancing, enhancing presence in Latin and North America

- Strong demand for engineering and project delivery expertise in gold, copper, and critical minerals

- Additional materials released at the 2025 AGM, including an updated Investor Presentation and the third annual Sustainability Report”

if you take the mid-point of guidance in November, NPAT of $42 million, that is similar to FY25 earnings. With 39.7 million shares outstanding, that’s approx $1.06 per share. At $15 per share LYL is sitting of on just over 14 times FY26 guidance earnings per share, which is close to the median over the last 5 years.

Using McNiven’s valuation assuming shareholder equity of $3.82 per share, forward ROE of 27.75% ($1.06/$3.82), 50% of earnings reinvested, fully franked dividends, and a required return of 12% per year, I get a valuation of $16.50. At a required return of 13% per year I get a valuation of $14.50. I think $15 is reasonable value with the current outlook given the range in guidance.

I think if we see FY26 earnings at the lower end of guidance the share price will fall below $14. If it’s toward the upper end of guidance the share price could edge above $16 per share. Like your @Bear77, I’m a solid HOLD at $15, and yes I would be backing up the truck at $10 with the current strong outlook for gold and other metals.

Held IRL (7%)

13/11/2025

FY26 guidance (announced today) suggests revenue will be between $390 to $410 million and Net Profit After Tax (NPAT) expected to be between $40 to $44 million. Taking a midpoint of guidance this suggests revenue will be up $66 million (20%) on FY25. However, NPAT will be similar to FY25 at c. $42 million. The NPAT margin is likely to be lower, ie. 10.5% compared to 12.6% for FY25. FY26 ROE should be similar at c. 27.8%.

I’m going to lift my valuation slightly to $14 per share, based on McNiven’s Valuation. While the inputs to the formula are much the same as my previous valuation (see below), I’ve lowered my required return from 15% to 14% based on LYL’s reliable performance record and the advanced integration of SAXUM. I’m keen to see @Bear77’s summary and view on the operations side.

Held IRL (6%), SM (0.3%)

25/09/2025

I’ve been quiet on Lycopodium recently. @Bear77 has done an excellent job in covering the business and the FY2025 results. Revenue and earnings fell 3% and 17% respectively this year. It’s still a decent result with the NPAT margin sitting at 12.6% and ROE just over 28%.

LYL will provide FY26 guidance at its AGM in November. However, on reporting theysaid the business outlook and demand for services indicated the Company will return another strong financial performance in FY26.

Assuming FY2026 earnings come in around $44 million ($1.10 per share) which is only slightly higher than FY2025 my valuation remains the same at $13 per share. This is based on McNiven’s Formula with equity of $3.82 per share, forward ROE of 28%, payout ratio of 33% (I expect this might increase from here), and a required return of 15%.

This valuation would put LYL on a PE of 12 for FY2026. It is currently trading on 11 times FY2025 earnings. I think in the past LYL has attracted investors looking for the high fully franked dividend. Returning to a 7% fully franked dividend (which is entirely feasible this year with LYLs strong fundamentals) is likely once the Saxum acquisition is paid for, and the debt is back to zero.

I’ll review valuation in November after management update guidance for FY2026.

Held IRL and SM

12/11/2024

The market doesn’t like the Lycopodium trading update:

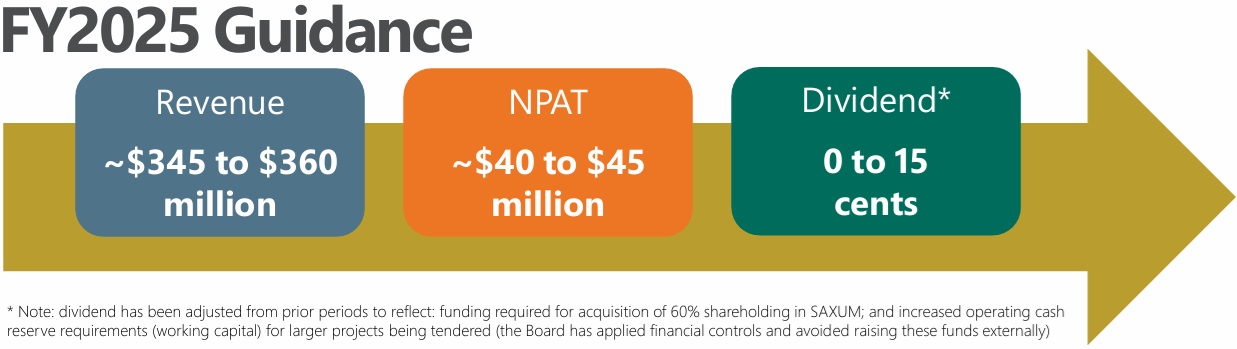

Analysts don’t cover LYL, so investors are on their own when it comes to price targets and valuation. I suspect the knee-jerk reaction today is due mostly to dividend uncertainty, but there will be a drop in earnings also. Projected dividends of 0 to 15 cps is disappointing if that’s why you own it. Over the last 3 financial years the annual dividend has been 81cps, 77 cps and 81 cps.

Does this mean the business is tanking? No. Far from it! However, the NPAT guidance of $40 million to $45 million is lower than I was expecting. FY24 earnings were $50.7 million. If we take the mid-point of guidance, $42.5 million, that’s a 16% drop in earnings. I was expecting earnings to be at least flat in FY25. That’s still a net profit of about $1.07 per share. At $10.70 that puts it on a PE of 10 times FY25 earnings. That’s not expensive.

FY25 ROE will remain strong at c. 33% (ie. 42.5 million / $127.4 million x 100). I was expecting a FY25 ROE of 35% so a slight disappointment here.

For a rough valuation pending a deeper dive into the future prospects of the business, I’ll use McNiven’s Formula and the latest guidance and assume ROE can be maintained at 33% going forward, equity of $2.88 per share, payout ratio of 14%, 86% of earnings reinvested at 33%, I get a valuation of $13 for a required return of 15% per annum.

While a low dividend/payout ratio seems disappointing, for a business like Lycopodium with a high ROE it’s actually a better use of capital than paying out dividends and increases the valuation of the business.

I’ll take a deeper dive over coming days, however I’ll probably add more if it drops below $10.50 again. I hope it doesn’t!

Held IRL (4.5%)

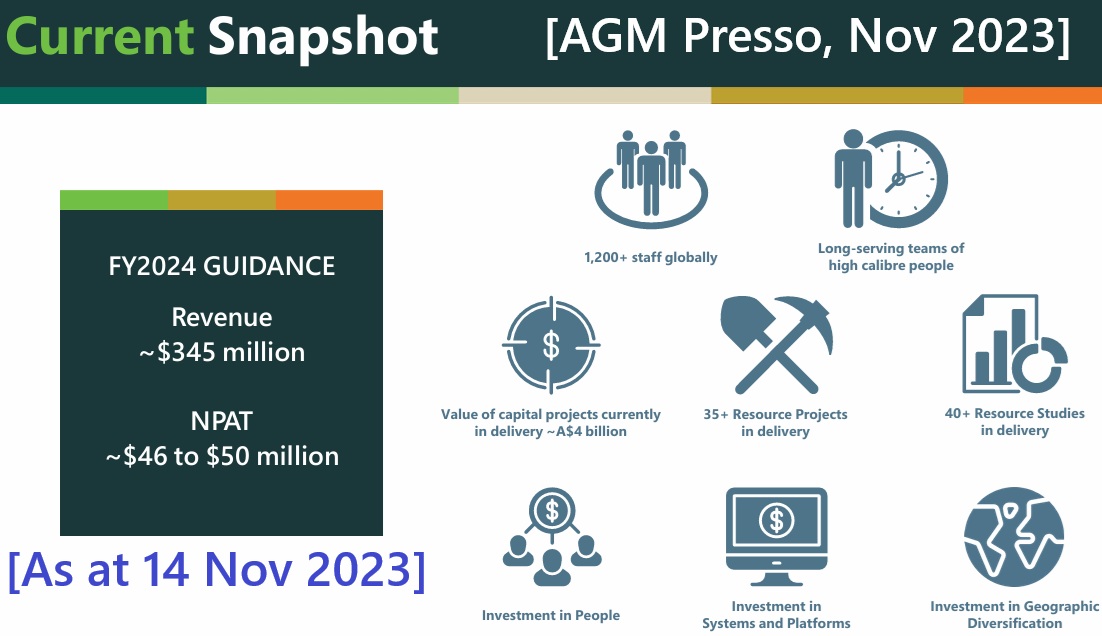

8/09/2024

@Bear77 has already covered the FY24 results in detail. I agree with @Bear77 that Lycopodium is a very high quality business and it is also one of my favourites. Bear mentioned the high ROE. I don’t get the same ROE as reported by management in the results (42.2%). FY24 NPAT was $50.7 million and Equity was $127.4 million, which makes FY24 ROE 39.8%. Some companies calculate ROE based on shareholder equity at the start of the year, some mid-year, and some the end of the year. On Commsec data ROE is calculated based on the equity at the end of the financial year. For consistency in comparing and valuing businesses I calculate ROE based on shareholder equity at the end of the financial year.

While FY24 NPAT came in at the top end of guidance, 2H24 NPAT was $20 million compared to $30 million for 1H24.

At this stage management has not provided guidance for FY25, rather some broad outlook statements:

• Strong long-term demand outlook for minerals and metals relevant to the ongoing energy transition will continue to attract capital to build global supply

• Demand for gold remains high, with production expected to increase as new projects and mine expansions become operational

• Demand for iron ore is expected to continue to increase steadily over the coming years, supported by new infrastructure investment in China and India’s growing infrastructure spending

• Australia’s railway construction and maintenance activity outlook is strong, supported by a number of significant publicly funded projects

• Domestic manufacturing continues to present opportunities for the Industrial Processes sector, as does the ongoing development of emerging markets in support of the energy transition, including waste and recycling, water and wastewater, and hydrogen

• Transformation of the global energy sector from fossil-based to zero-carbon sources represents a period of innovation and opportunity in the development of new systems that can operate on low carbon energy sources, whilst maximising waste recovery and reuse

• Lycopodium’s expertise will remain sought after given the macro environment and other drivers

There’s nothing much here to hang a valuation on with a high degree of confidence!

While Lycopodium is slowly diversifying, it remains highly exposed to gold projects in Africa, as can be seen in the slides below:

The gold price continues to hit all time highs and while the gold price is strong Lycopodium should continue to do very well.

My last valuation of $15 was over 6 months ago and was based on an ROE of 38%. I’m tempted to pull this back a little given 2H24 NPAT was quite a bit weaker than 1H24. I think there’s a possibility FY25 earnings could be lower than FY24 given the current pressure on commodity prices other than gold, which make up the next largest component of Lycopodium’s business.

Using McNiven’s Formula assuming a more conservative ROE of 35%, equity of $3.22 per share, 40% of earnings reinvested at 35%, 60% of earnings paid out as fully franked dividends (9.4% gross yield), and a required annual return of 14% I get a valuation of $14. At the current share price of $11.75 I think Lycopodium is a BUY and will likely add more shares before it goes ex-dividend on the 19th September.

Held IRL (4.9%)

21/02/2024

Lycopodium (LYL) released another great 1H24 result today. This is a very high quality business operating in a cyclical industry. It is diversified and is starting to grow revenue in some less cyclical sectors, for instance: “Transformation of the global energy sector from fossil-based to zero-carbon sources represents a period of innovation and opportunity in the development of new systems that can operate on low carbon energy sources, whilst maximising waste recovery and reuse” (1H24 Presentation). However revenues are heavily skewed towards resources in Africa.

It’s a high quality business because currently it has a very high return on equity (38%). If you look at the presentation LYL say their ROE is 25.5%.

Here they are calculating their ROE as the 1H24 NPAT/ Equity. I questioned this in their previous results meeting and they agreed it was only calculated on the half. It needs to be calculated using full year NPAT. LYL reaffirmed guidance for FY24 to be $46 - $50 million. That looks a tad conservative too, given they’ve already achieved $30 million of that. @Bear77 would agree (since it will be in the top 3 companies on Strawman today) that LYL is just one of those quiet achievers that just plugs away doing marvellous things with your equity without crowing before the eggs are laid!

My calculation of ROE based on equity at the end of Dec 2023 ($127.1 million) and mid-guidance of $48million is 38%. This might not hold up through a depressed cycle so we need to keep a close eye on it. LYL generally pay out approx 70% (50% for this half) of their earnings in dividends, and the dividends are fully franked.

For FY24 I am expecting a fully franked dividend of 84cps (70% of guidance EPS, $1.21cps). That’s a forecast yield of over 6% fully franked, or 8.5% including franking credits.

Valuation

Turning to the valuation using McNiven Formula assuming ROE 38%, Equity $3.07 (Dec 2023) 30% of earnings reinvested, and requiring a return (RR) of 15% I get a valuation of c.$15 per share, the same as my previous valuation but now I feel the valuation is slightly more conservative. While the cycle is strong LYL should continue to do well.

Held IRL (3%)

14/11/2023

My valuation and justification remains unchanged from 3 months ago (see valuations at LYL). The last three months have panned out even better than I expected and today’s FY24 guidance confirms LYL is expecting continued growth which puts ROE to remain in excess of 40% over the next 12 months. The business is virtually debt free with $82.4 million of shareholders total equity of $113 million sitting in cash. Investors could expect dividends in FY24 to be between 9% and 10% fully franked (over 13% gross yield including franking credits). This is while it continues to reinvest 30% of earnings back into growth.

01/08/2023

Lycopodium said in its guidance update on the 11th April that in the final quarter it is “continuing to see a high level of activity across all operating sectors, delivering a robust order book of projects and feasibility studies across a broad geographic footprint. We are also seeing a strong study pipeline which bodes well for the future. This significant level of activity across all sectors of operation continues to translate into healthy financial performance. The Company now provides an updated guidance for the full financial year, with forecast revenue of $320 million and forecast net profit after tax (NPAT) of $45 million.”

What to expect for FY23:

- FY2023 NPAT of $45 million represents a 45% ROE, and is 67% up on last year (FY22 of NPAT $27 million)

- FY23 Net Profit Margin 14%

- FY2023 EPS $1.13 (80 cps FY22). FY23 PE 8.9 based on the current share price of $10.06

- Debt free

- $2.40 per share held in cash ($95 million cash, 39.7 million shares)

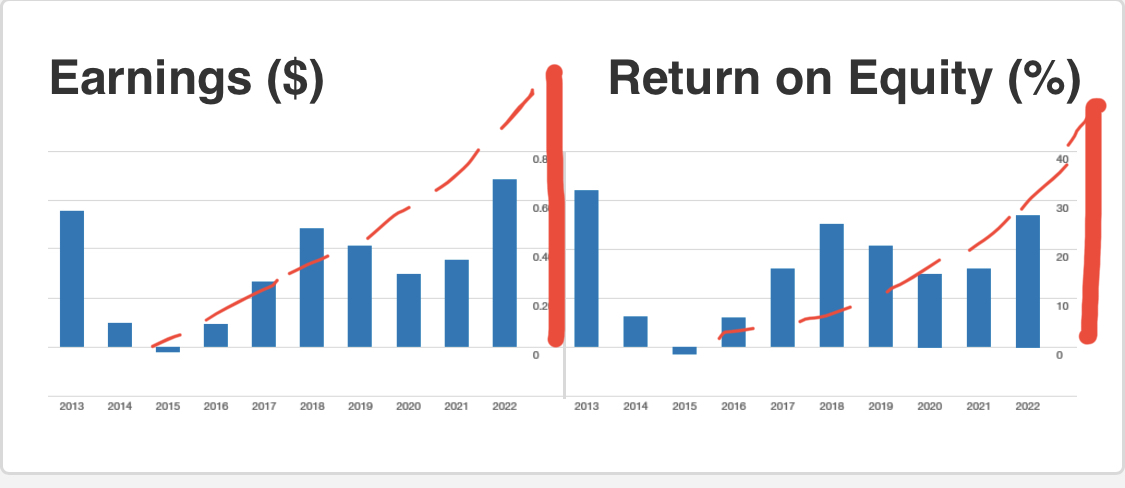

At 45%, Lycopodium’s ROE will be the highest in over a decade, and this is the seventh successive year where ROE has been higher than 15%.

FY23 Earnings and ROE represented in red (Adapted from Commsec data)

I don’t know of any other business which has zero debt, holds 24% of its market capital in cash, and at the same time is expecting ROE of 45%.

Source: Simply Wall Street

Shareholder equity is $2.60 per share of which $2.38 is held in cash and equivalents.

At $9.70, Lycopodium’s shares are trading close to their all time high of $10.60. In January 2016 shares were trading for $1.16, so along with it’s fully franked dividends it has realised excellent returns for shareholders over 7 years.

Dividends

At a historic payout ratio of 70%, the final dividend is likely to be over 40 cps, fully franked. The interim dividend paid was 36 cps, fully franked. Shareholders can expect a grossed up annual yield of circa 11% (including franking credits). There is plenty of cash sitting on the balance sheet, so there is also the possibility of a special dividend, a share buy back or an acquisition some time in the future.

Valuation

Over the last 4 years the average PE ratio has been 12.5 (calculated from Commsec annual average PE data). The current PE ratio based on FY23 earnings is 8.6, well below the historical average. Given business performance has vastly improved over 4 years (ROE has more than doubled), I think it is reasonably conservative to use an average PE of 12.5 for valuation. This makes Lycopodium worth over $14.00 per share.

Given the improving business performance I would prefer to use McNiven’s StockVal Formula for valuation. Assuming ROE continues at 40%, reinvested earnings 30%, equity $2.60, you could pay up to $12.50 and still get a 15% annual return (including franking credits).

Even though Lycopodium is trading near all time highs, I think it is excellent value at the current share price. At $9.72, you could expect an annual return of c. 18% including franking credits.

You could pay up to $17 and still receive an annual return of 12% (including franking credits).

I think Lycopodium is currently one of the best (if not the best) mining services businesses on the ASX. I’ve been adding shares below $10 and have lifted my valuation to $15 per share.

Disc: Held IRL (0.8%).

17/04/23

The Lycopodium share price has shot past my previous valuation of $10.00. Is it now overvalued? Not if you base your valuation on the updated guidance with NPAT expected to be $45 million for FY23. That will put FY23 ROE at 43% ($45 million NPAT / $103.5 million equity). That’s the highest ROE in 10 years, and possibly the highest on record for LYL.

Source: Commsec

Source: Commsec

Lycopodium is definitely in a sweet spot at the moment with ‘a high level of activity across all operating sectors, delivering a robust order book of projects and feasibility studies across a broad geographic footprint.’ The increased activity is driven by battery minerals, gold and copper. While we continue to see strong activity in these sectors we can expect LYL to thrive. I think we will see this across the board in other mining service companies also.

My previous valuation was based on a ROE of 35% and a required return of 15% p.a. I feel comfortable bumping the ROE for LYL up to 40% for an updated valuation. Still requiring a 15% p.a. return on my investment my updated valuation jumps to $12 (McNiven’s StockVal Formula). If you were happy with a 12% p.a. return you could pay up to $16 while ROE remains over 40%.

A caution though, this is a cyclical industry and at these share price levels it’s important to keep a close eye on future guidance and the health of the miners.

Disc: Held IRL (0.6%)

Feb 2023

Thanks @Scott for your 1H22 results straw and valuation. This is an excellent result for Lycopodium, and their best return on equity (ROE) in a decade (39%). Unfortunately, they did themselves a disservice in the presentation:

I asked MD Peter de Leo on the conference call this morning if this was based on the return for just 6 months rather than an annual ROE, which he confirmed.

Those who follow my straws would know that ROE is the first metric that gets my attention. I’m looking for businesses with a track record of consistently strong and preferably growing ROE. I try to find businesses with a minimum of 15% ROE and preferably higher than 20%. There are plenty of businesses with ROE higher than 20%, but most trade on high multiples of PE and PB.

Lycopodium is a quality business and has averaged ROE of between 15% and 25% over the past 6 years. This year ROE will be close to 40%. That’s the best ROE in a decade.

However, Lycopodium is also a cyclical business with over 90% of its revenues coming from resource companies. Earnings can fall away rapidly when the shine goes off mining.

None the less, it has a track record of high ROE, and I expect ROE to be in excess of 30% for a few years to come. With NPAT guidance of $40 million, or $1.00 per share, that puts LYL on a FY23 PE of 8.3X. How many businesses can you buy with a PE of 8 and a ROE of 40%. Not many!

If I use McNiven’s StockVal formula, assuming normalised ROE of 35%, a dividend payout ratio of 70%, franking of 100%, and a required annual return of 15%, I get a valuation of $10.04, say $10.00.

I don’t think this is a business you buy and hold for ever. Having said that I have held LYL for several years. The time to sell is when the pipeline of work with resource companies starts to dry up. The project pipeline for Lycopodium still very strong so it’s a strong hold for me.

Disc: Held IRL (0.6%)

August 2018: LYL has already overtaken my previous price target. This ($5.45) is my new 6 month price target. They continue to perform well. . . .

Feb 2019: 12 month price target will depend on new contracts and commodity prices (esp. gold) which will in turn depend on what's happening in the world. Very hard to predict. . . .

Update: 31-Aug-19: Overtaken my updated PT. New PT = $6.77, based on quality management, quality company, and tailwind of higher gold price. . . .

29-Feb-2020: Update: Due to delays experienced across the industry with the timing of contract starts and new contract awards, it may take a bit longer for LYL to hit my latest $6.77 PT, so faced with new information, I'm reducing it back down to $5.80, which is a level I think they can reach over the next 6 months (by early September 2020) with a couple of reasonably sized new contract wins, and their usual outstanding performance on existing contracts.

29-Aug-2020: $5.80 is still fine for a 12-month PT. They went over $6 in Jan/Feb this year, and would have probably maintained those levels if it wasn't for the pandemic. LYL specialise in designing, building and optimising gold processing plants, and that's a great space to be at the minute. The downside is that they have traditionally done a lot of their work in Africa, South America, and other risky places to operate. Back here in Australia, GR Engineering (GNG) seem to get most of that work. Ideally I'd like to see the two companies merge, or LYL acquire GNG, but that may never happen. Would be good if it did tho... I hold both. GNG is a long term hold for me. LYL is a company I tend to buy when they look undervalued and sell when they look expensive. They look undervalued here (below $5) so I'm holding them.

LYL do a lot of other stuff also - not just gold plants. Have a look at their website for more on that.

They were originally (many moons ago) the engineering arm of Monadelphous (MND), which was spun out, and in recent years the two companies have formed a JV called Mondium which has been gaining traction, winning larger contracts each year. I also hold MND shares.

Update: 01-Mar-2021: This is another company that seems to be happy to sit at or around the price target that I set 12 months ago - $5.80 in this case, but I should acknowledge that prior to that it was $6.77 and I reduced it to $5.80. The $6.77 PT (in 2019) did not get taken out. $5.80 seems to be around the mark, and I would be raising it if gold was on a tear, but it ain't, so I won't. I think LYL will likely bounce around this level for a while, probably falling away on no news, then coming back up when new contracts are announced. I still hold LYL shares - and GNG shares. GNG had a corker of a day today, up another +5.84% to $1.45. Of the two, you'd have to say GNG has the far superior chart at this point - it's exactly what you want to see - all bottom left to top right at a very good clip. LYL is bouncing around their 12-month high but they don't have the same north-bound momentum that GNG currently do. I'm happy to be holding both, particularly GNG with their recently declared 5 cps fully franked interim dividend.

I'm leaving my PT for LYL at $5.80 for now, but will raise it if they break through $6 with any conviction. If they do that I think they're heading for around $6.70 by this time next year.

Update: 30-Aug-2021: Still happy with $5.80 for a PT for LYL, but that other former $6.70 PT for March 2022 might be a bridge too far from here (currently $4.75). LYL reported on 23-Aug-2021 and rose +4% on the day - from $4.61 to $4.80, but they haven't shot the lights out. GNG is looking better than LYL at this stage, and I do have significantly more invested in GNG than in LYL at this point. I have maintained a small RL position in LYL, but have a much larger one in GNG for their dividend - latest one is 7 cps (FF) for GNG, so their dividend yield is almost 6%, plus franking credits (12c/year FF). LYL have declared a 15 cps final div, so when added to their 10 cps interim dividend, they are on a 5.26% yield, plus franking, and LYL fully frank their divs also. Both do very similar work, however most of LYL's work is outside of Australia, and most of GNG's work is at home - within Australia, although not all. Both have liquidity issues due to being microcaps (LYL is < $200m, GNG is < $300m market cap) and having very high insider ownership. Holders are usually not interested in selling, so there can be precious little available to buy.

Their results can also be lumpy due to the shorter term nature of their EPC work, although GNG also have recurring revenue from their Upstream PS division - but check out GNG for further details on that - this is supposed to be about LYL. Both LYL and GNG have high quality management with heaps of skin in the game, both companies avoid debt and always maintain net cash on the balance sheet, both have excellent risk management strategies in place which clearly work, even when their clients get into financial difficulty occasionally and have trouble paying their bills. GNG & LYL have good track records of being conservative with their accounting and with their guidance, and collecting on their bad and doubtful debts more often than not.

LYL often work for larger companies on average than GNG do, although that is a generalisation and isn't always the case. I like them both, Two of my favourite engineering and construction companies. My other favourite in the space is MND - Monadelphous - but Mono's do other types of E&C to what Lycopodium and GR Engineering Services do. Mono's also have a variety of different divisions so they are much bigger with many more sources of revenue, including recurring revenue from multi-year operations and maintenance contracts. Of the three, currently GNG is performing the best, and MND is the safest, but LYL will have their day in the sun again one day. If they get back down to $4, I'll probably load up.

$7 is probably a good 5 year PT for LYL, so $7 by September 2026.

Update: 24-Aug-2022: LYL reported for FY22 today, and it was very good. All covered in various straws. They are now on a 9% dividend yield, or a 12.6% grossed-up yield (that includes the full value of their franking credits). Their FY22 dividends are more than double what they paid in FY21.

I am updating my valuation to $7.40 to reflect the significant growth the business has achieved in FY22 and the positive outlook they have for FY23.

Update: 23-Feb-2023: Six months on, and LYL have released one of the best half year reports I've seen this year, perhaps THE best one. I won't talk about it too much because it's been well covered in the straws and valuations by @Scott (see here) and @Rick (see here). However, this latest half year report by Lycopodium is a cracker. Particularly given the industry headwinds, especially around the pandemic and the associated recruitment and staff retention challenges experienced across the sector.

FY2023 H1 Results Announcement

FY2023 H1 Results Presentation

That's from page 1 of their announcement (link above) but I've added the percentage increases (in the green boxes, plus the green arrow) because they seem too shy and bashful to point out how well they've done. They're not big on blowing their own trumpet, this mob!

Their full year guidance of approx. $320m in revenue and $40m NPAT is simply double what they managed in the first half ($159.9m and $20m), so I have no doubt they will exceed those numbers, as they usually do. Underpromise and overdeliver. That's their MO. I hold LYL both here and in real life, and I always have high expectations of both LYL and GNG (who do the same stuff but with a more Australian focus, LYL specialise in West Africa and other risky places and they are very, very good at risk management), but LYL even beat my own high expectations sometimes. They are THAT good!

LYL closed at $7.64 on the 21-Feb-2023 (Tuesday), the day before they released these results, comfortably meeting my previous price target (set six months ago) of $7.40.

On Wednesday, on the back of these results, they rose +76 cents (+10%) to close at $8.40. Today (Thursday) they rose another 7 cents to close at $8.47. Based on their most recent full year dividend of 36 cps plus this one (another 36 cps), that's 72 cents per share per year now, which means their dividend yield is 8.5%pa based on today's price, and 9.4%pa based on Tuesday's closing price. Based on my average buy price (IRL) of $6.05 (yes, I've averaged up on this one), they're on an 11.9% yield, and that's not taking any of the franking credits into account. And their dividends are all fully franked. To get the grossed up yields (to include the full value of the franking credits, you can take those yields and multiply them by 1.42857 - or just add 43% more on.

That's a handy tip for anybody that wants to work out the franking credits they're going to get on a dividend. Work out the total amount you're going to get in the bank, and if that dividend is fully (100%) franked at the 30% corporate tax rate, you can use the following formula:

30 / 70 x X

where X is the full amount you're going to receive in the bank, "/" means "divided by" and "x" (the small x) means "multiplied by".

If the dividend is coming from a small LIC (like SNC) or any smaller company who qualifies for the lower 25% tax rate, you would use this formula:

25 / 75 x X

The first two numbers in the formula always need to add up to 100 for the formula to work. The first number is the corporate tax rate that applies and the second number is 100 minus the first number. The reason you can't just add 30% to the amount you're going to receive is that a fully franked dividend includes the tax payable on the entire value of the dividend and the franking credits, because the franking credits count as both income and a tax credit, so they have to cover the tax payable on the franking credits plus the amount you're going to get in the bank, which usually works out to 42.857142857% or 30 / 70.

That formula gives you the dollar value of the franking credits you're going to receive. If the dividend is only 85% franked, you would add "x 0.85" to the end of the formula, so for MFG's latest dividend the franking credits would be:

30 / 70 x X x 0.85

For Altium's latest dividend, which is 40% franked, you would change the 0.85 to 0.40 (or just 0.4 or even .4, as the extra zeroes in this case are superfluous).

30 / 70 x X x 0.40

So - if you held 8,000 LYL shares, you would get $2,880 (being 8000 x 0.36) in the bank on the 6th April, plus $1,234.28 in franking credits (or $1,234.29 if they round to the nearest cent instead of ignoring everything after the second decimal place). That $1,234.28 is:

30 / 70 x 2880

Anyway, sorry about the excruciating level of detail (helpful no doubt to some, very obvious to others), but that is all to say that LYL were on a VERY good dividend yield before these results, and they still are, even with the share price rise we've seen this week.

And while they are certainly a good income stock, they are also a growth stock. Their core revenue is lumpy by nature - being one off engineering, procurement and construction (EPC) contracts, often with an "M" tacked on - meaning that they manage the projects as well, but they keep winning more and more work. Some of their more recent work has not included the "C" - it's been "EPM" work, so Engineering, Procurement and Management of projects, especially some in West Africa. That, no doubt, is also part of their risk management. They will often let others do the actual boots-on-the-ground construction in these higher-risk areas of the world, and get paid very well for designing the plant, procuring all the parts and equipment and material required to build it, and managing the whole process.

But that better belongs in a Bull Case straw I suppose. Superior management who are exceptional at risk management in some of the more risky parts of the world to build gold plants.

However, as their presso points out, they are active in a number of industries, they have more than one string (gold plants) to their bow, and they just keep on delivering for their shareholders. I plan to buy more soon once one or two of my other companies goes ex-div.

And they do a lot more than just gold plants of course, like Lithium...

https://www.lycopodium.com/case-studies/

https://www.lycopodium.com/what-we-do/

https://www.lycopodium.com/about-us/our-story/

27-Aug-2023: Update: After FY23 full year results in August:

Raising my price target for LYL to $11.88 (from $9.70 - which they've already reached and passed).

Source: LYL-FY2023-Full-Year-Results-Announcement-22-Aug-2023.PDF

See also: LYL-Investor-Presentation-FY2023-22-Aug-2023.PDF

Souurce: Commsec (trend lines added by me).

Not growing in a straight line all of the time, there are pullbacks, but the overall trend is up and the growth has been substantial.

Current 12m trailing dividend yield is 7.9% plus franking, and all of their dividends have been fully franked. That's a grossed-up trailing yield of 11.2% (including the full value of the franking credits).

And we have share price growth as well:

Source: Commsec (as at Friday 25th August 2023, showing Friday's price movement (-1.72%) at the top.

Disclosure: I continue to hold LYL shares (both here and IRL). Liquidity is still an issue, however it's a great place to park some patient money and watch it grow and produce income at the same time.

03-March-2024: Update: Raising my PT for LYL from $11.88 to $14.25, as they've already shot past my previous price target. They keep on underpromising and overdelivering. Here's their H1 of FY2024 results summary table:

As usual, they did NOT provide any percentages - I've added those (above) on the right side of the table. The cash fluctuates depending on progress payments, completion payments, and so forth, so I'm not fussed about the cash levels - they move up and down a lot, but they always have plenty of spare cash - they are, after all, a small company with a sub-$500m market cap, so $69m of net cash is plenty.

Here's page 1 of that results announcement:

And here's a link to the full announcement: Lycopodium-Half-Year-Results-Announcement.PDF

And to their results presentation for the half: 1HFY2024-Investor-Presentation(LYL).PDF

And below is a share price comparison of LYL, GNG and MND against the S&P/ASX200 TR (total return) Index (XJO) - Lycopodium, GR Engineering and Monadelphous all being quality ASX-listed engineering and construction companies that I hold in real money portfolios (and I also hold two of them here on Strawman.com):

GNG has done OK, but LYL is powering ahead now. Happy to be holding. They're growing at a good clip, they are very profitable, they pay excellent fully franked dividends, they have high insider ownership (great alignment of interests between management and ordinary shareholders), they have superb industry position, they are very well run, and the management like to underpromise and then overdeliver. Not very much NOT to like! And LOTS to like!

21-Aug-2024: Update (post FY24 Full Year Results):

I've written about my thoughts on today's results and the market's reaction here (it may loop back to this valuation, so just scroll down and the straw will be below it).

I would have preferred a higher final dividend, but it's all good - I increased my exposure today both here and in my largest real-money portfolio where it is now my second largest position (10,000 shares worth $123.4 K based on today's $12.34 closing share price) and only $5K below my largest position, WLE (100,000 shares currently worth $128.5 K), so I'd expect LYL will become the largest position in that portfolio soon enough as we get a little bit of a recovery in the share price after today's -12% fall.

Interesting thing I found today on Strawman.com. The system kept telling me my buy order was too large and would exceed the 20% portfolio position limit (no single position can be more than 20% of your entire portfolio value here at the time of purchase or top-up, a rule that also applies in my super which is in an industry super fund). The trouble was that the system here was basing that on yesterday's closing price for LYL, which was $14.02, being $1.68 higher than where they closed today, so that meant that I couldn't move up to 20% of my portfolio here with a buy - I could only end up with 18.5%. Oh well, there's always tomorrow.

Here's a quick recap of today's results:

Dividend down -4.9% vs pcp, ROE down -4% from 44% in FY23 to 42.2% for FY24, Cash down -18% from $82.4 million to $67.6 million (and their cash always bounces around because of the timing of significant milestone payments with their larger projects - but they have net cash and no debt), and everything else up.

Record Revenue, Record Earnings, Record EPS, and on a single digit PE ratio now also.

My previous price target had already been achieved prior to today, so I'm moving it up again, this time to $14.85.

Disclosure: Yes, I hold Lycopodium shares.

Lycopodium replaced Monadelphous Group (MND) - a couple of years ago - as my favourite ASX-listed company. Other favourites include ARB Corporation (ARB) and GR Engineering Services (GNG) and a few gold producers (NST, GMD, RMS).

They can be very illiquid, because 33% of their shares are owned by their Board, Management, Founders, and their families, but worth taking the time to accumulate a position, IMO.

They're in the All Ords Index, and when they do finally get added to the ASX300 Index they will absolutely get added to my SMSF (where my direct share ownership is limited to ASX300 stocks because it's in an industry super fund).

For now I hold them outside of my super, and here on SM also where they are my largest position.

https://www.youtube.com/watch?app=desktop&v=-Mp5i9Zhqdg

21-March-2025: Update:

This one has been marked as stale (6 months old), but I don't have anything to add really, other than what I've already put into straws and forum posts. The $14.85 share price target that I set here in August (2024) is still good. The company is the same today as it was then, with the same upside potential and outlook. The main difference is that the share price is now lower, but that doesn't change my PT.

I don't think I gave a timeframe for that $14.85 PT in August, but I'll give one now - $14.85 by November 2027 - which will line up nicely with them being my pick in this thread: here: Highest conviction stock with great management you trust which had a 3 year timeframe from November 2024, so the finish line for that fantasy portfolio is November 2027.

I will make two other observations, the first being that $10 has recently proved to be a good downside resistance level, and that LYL can often have low liquidity as demonstrated by the gaps between the buys and the sells (price points) below:

So, they're best held by people who do have high conviction, because if you get shaken by the share price volatility and you lose your nerve and want to exit, there can be very few buyers and the price those few buyers are prepared to pay can be a lot lower than what you might consider to be fair value.

So fair warning about that low liquidity. The share price can and at times certainly WILL be volatile, but that is a good thing if you have high conviction and a fair idea of your buy zones and your sell zones.

Disclosure: Held. LYL is my largest position both here and in my real money portfolios. [I do have high conviction in this company]

19-Sept-2025: Update: No change

I've just posted a straw about them going ex-div yesterday and holding above that $12/share level that I think is shaping up to be a new downside resistance level (previously was $10/share), so I'll not repeat all that.

The TL;DR version: Back to higher dividends again now I reckon and they've got some good gold tailwinds too.

No change to my $14.85 price target. That and then some. Still happy to have this one as my largest real life (real money) position.

Thursday 5th Feb, 2026: Update:

Raising my price target again - they have already overtaken my old one of $14.85 - so I'm moving that PT up to $17.70 now.

I've explained a fair bit of why in a forum post I added here a couple of hours ago - click here for that - however there's also the gold price of around A$7,000 / around US$5,000/ounce, significantly higher than it was in September (see above in my previous update).

Here's where it was yesterday (4th Feb):

Gold and copper prices are currently providing good tailwinds for Lycopodium and they do deserve to trade at a higher P/E multiple than where they have traded in recent years as I explained yesterday in that post (link above).

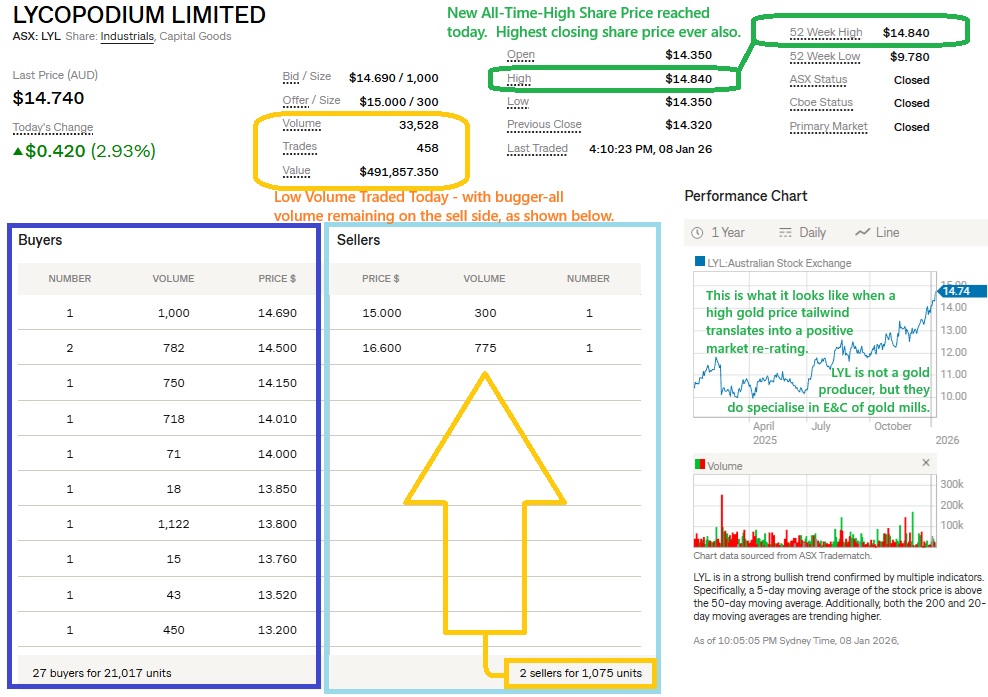

Thurs 8th Jan 2026:

Disclosure: Lycopodium is my largest position both here and in my real money portfolios.

My analysis today: This is not a company in a bubble of any sort, it's a good old-fashioned engineering and construction (E&C) company that specialises in the engineering (/design) and construction of gold processing plants (gold mills). That's certainly not all they do, but it's what they are best known for, and they are enjoying a positive market re-rating as the liklihood of further work across the gold and copper sectors in particular - and in other commodities also - becomes more and more likely.

Many gold projects that were not economically viable two years ago are certainly positioned to make big profits now if those projects can be brought into production within a reasonable period of time while the gold price is still high. And that's what LYL do globally (and GNG do mostly here in Australia, LYL is my largest position IRL and GNG is my second largest).

LYL and GNG do scoping studies (SS), pre-feasibility studies (PFS), feasibility studies (FS, also known as BFS and DFS - bankable/definitive feasibility studies), front-end engineering and design (FEED), and they are EPC / EPCM / EP&PM contractors as well and that's where they make the big dollars.

- EPC = Engineering, Procurement and Construction.

- EPCM has Management (Project Management) tacked on as well.

- EP&PM (sometimes called EPM) means Engineering, Procurement and Project Management, so not the actual construction.

LYL do not usually do the actual construction, however they mostly manage that construction on behalf of their clients. LYL operate mostly overseas and they usually use in-country construction companies to do the actual boots-on-the-ground construction work and they (LYL) manage that construction with minimal boots on the ground themselves. They have excellent risk management that has worked for them very well for decades and has allowed them to work very profitably in West Africa and other places that are generally considered higher risk.

In the past 18 months two things have happened that I think are noteworthy. The first is that LYL withdrew from the bidding process for two large, higher-risk projects for Barrick Gold - the world's second largest gold mining company who are also diversifying into copper and other commodities now. Those projects that LYL have walked away from are Barrick's Reko Diq in Ballochistan, Western Pakistan (wedged between Iran and Afghanistan - see map below) and Barrick's Lumwana copper mine expansion project in Zambia.

Reko Diq (shown above) in particular is likely to be one of the most dangerous places to build and operate a copper/gold mine in the world today and it's unclear whether Lycopodium withdrew from the bidding process (after delivering studies for both projects to Barrick) because of the risks or because Barrick were not prepared to compensate LYL adequately for those risks; but either way it's a net positive in my view that Lycopodium have the discipline to walk away from a project like Reko Diq which would have been LYL's largest contract ever if they had bid for it and had been awarded it.

I note that Fluor Corporation, a company headquartered in Irving, Texas, has been awarded the EPCM contract for Reko Diq, with final notice to proceed given to them by Barrick in late July 2025 - see here: https://newsroom.fluor.com/news-releases/news-details/2025/Fluor-Receives-Final-Notice-to-Proceed-from-Barrick-on-Reko-Diq-Copper-Project-in-Pakistan/default.aspx

So it's safe to assume that LYL are no longer involved in Reko Diq in any capacity now, which is likely for the best.

Barrick's planned major expansion of their Lumwana copper mine in Zambia is still going ahead apparently - see here: https://www.barrick.com/English/news/news-details/2025/lumwana-expansion-in-full-swing-as-barrick-builds-tier-one-copper-mine/default.aspx [July 10, 2025] - However LYL do not appear to have continued their involvement with that project after delivering the feasibility study (FS) and basic engineering for it in 2024. Again, it's not clear if there are project-specific reasons for this or whether it's just a Barrick thing - or more likely a Mark Bristow thing.

Bristow announced his resignation as Barrick's CEO and President on September 29th, 2025, departing the company immediately, with Mark Hill appointed interim CEO the same day. His exit was sudden and without a stated reason from Barrick, though sources later pointed to issues with Mali operations as a contributing factor, say The Globe and Mail.

Bristow was a hard man to deal with by all acoounts, very stubborn and not prepared to admit when he had made a mistake, and not at all sympathetic to major shareholder concerns about his taking the world's second largest gold producer away from gold into copper and other commodities and moving into much riskier jurisdictions without developing the required positive relationships with those countries governments (at all levels), regulatory authorities or local communities where Barrick either operated or wanted to operate.

Bristow took a hard line approach to dealing with the military Junta running Mali and in the process managed to lose control of their (Barrick's) gold mines in Mali and also had an arrest warrant issued for him (Bristow) in Mali, which apparently still stands if he ever makes the mistake of returning to Mali.

Australian company Resolute Mining (RSG) also had major issues in Mali - Terence Holohan, the CEO and MD of RSG was detained in Mali for 10 days in November 2024. He and two other employees were held in the capital, Bamako, over a tax dispute with the Malian military government and Holohan quit RSG after he was released.

Lycopodium is likely to have a list of countries that they will NOT work in, such as Mali at this point in time, and that list would be fluid as situations change, and Lycopodium would also have companies that they would prefer not to have as clients, often because of the company's management and the way they go about things, and that could be the case with Barrick, I don't know, but LYL don't often walk away from large projects after doing all the studies and a fair bit of FEED work, yet they have walked away from two large projects both owned by Barrick in the past 18 months.

My take on that is that it is a real positive because it highlights to me that Lycopodium's risk management processes are robust and they won't chase work that is too risky, or where they are not being adequately compensated for risk where they believe they can manage that risk.

In relation to Lumwana, Google tells me that Zambia presents mixed risks for mining: it's historically stable but faces significant challenges like severe environmental pollution (lead, heavy metals), high safety risks (accidents, poor conditions), and governance issues (taxation, local benefit sharing), alongside recent major environmental disasters (like the 2025 Chinese-owned mine tailings dam collapse) that strain investor confidence and community relations. So not sure whether Lumwana was considered too high risk or a project for which Barrick did not want to adequately compensate Lycopodium for the risk in Lycopodium's view.

China and Russia (Russia mostly through the organisation formerly known as Wagner Group) are both becoming more and more involved in Africa, both central and western Africa, and that also brings various new risks to the countries in Africa where China and Russia are most active.

This is interesting: Zambia Mining Disaster May Have Been 30-Times Worse Than Estimated [Aug 15, 2025, Bloomberg Television, on YouTube]

Plain text link: https://www.youtube.com/watch?v=4IMLHxiyTXM

OK, so that's the first thing I've noticed over the last 18 months, clear examples of risk management in action at Lycopodium.

The second thing is their acquisition of 60% of SAXUM - which has been covered here in straws and forum posts. I like that a lot. I like the measured way they are expanding into Central and South America using SAXUM and that they have the option to acquire the remaining 40% of SAXUM at a future date - the deal is designed to keep all of the SAXUM founders and employees in place and incentivised to continue to grow the company and do well.

I also like that instead of issuing new shares when they believed they were undervalued (at around $10/share then - now over $14/share) or borrowing money, they simply used their own cash and replenished that cash by reducing one dividend. LYL remain debt free and they've had a stable share count for over a decade now.

So evidence of risk management in action, and evidence of a growth strategy into new geographies and new areas of construction, e.g. SAXUM is big in cement and lime in Latin America, and that side of their business is growing at a good clip, so there's geographic expansion opportunities as well as cross-selling opportunities.

Lycopodium is a very well managed company under Peter De Leo's leadership - and there's heaps of insider ownership with around 35% to 40% of the company owned by their Board, Management and the company's founders, with some of those founders still working within the company in Management and Board roles.

This high insider ownership reduces the free float, and shareholders like me who tend to aggregate a larger position rather than sell shares also tends to reduce the liquidity even further, as I've highlighted at the top of this post with just 2 remaining sell orders left in the market after the close today, being 300 shares for sale at $15 and 775 shares @ $16.60 - and that's it. More sell volume will surely emerge during trading tomorrow, but even during the trading day the volume is usually thin with this one.

What that lack of liquidity means is that you probably want to get in when the share price is depressed, like the 7 months between November 2024 and June 2025 (inclusive) where the LYL share price traded mostly between $10 and $11 and kept dropping back to $10 regularly, because when they get a positive re-rating - as they have recently - there just aren't the sellers there to enable you to build a half decent position.

On the flip side that's good if you already hold a decent position (I do), because while the demand to buy them continues, the share price is more likely to rise further than to fall because of that lack of volume on the sell side.

It's certainly a nice graph now! As Colonel John "Hannibal" Smith, the leader of The A-Team, used to say, "I love it when a plan comes together."

Further Reading: FY2025 AGM Presentation: https://www.lycopodium.com/wp-content/uploads/2025/11/FY2025-AGM-Presentation-1.pdf [13-Nov-2025]

Further Viewing: Peter De Leo presenting at ASX SMIDcaps 2025: https://www.lycopodium.com/wp-content/uploads/2025/10/ASX-SMIDcaps-2025-Presentation.mp4 [09-Oct-2025]

So, are they a buy today? They were at below $12/share and I was not shy about that at the time. Up here near $15/share there's obviously now less upside, but I still reckon a buy up here wouldn't be a bad thing when you look back in 5 and 10 years time from now, but no, I'm personally NOT buying up here - They are already my largest position - I hold 10,000 LYL in one portfolio - currently worth $147 K, and some more in a second portfolio that holds my kids' investments - and that kids' portfolio only has one company in it, LYL. So no, I'm not buying more up here myself, but I'd consider buying more if they pulled back to near $10/share again.

23-Dec-2025: LYL are certainly back in a solid uptrend now:

LYL reached a new 52-week high of $13.81 during this morning's trading; the only time they've been this high before was briefly in August 2024 when they went over $14. It's hardly surprising because they're a very profitable company with a rock solid balance sheet (no net debt and plenty of cash) and they have strong tailwinds. They specialise in the design, engineering and construction of gold processing plants (gold mills), and the gold price is reaching new all time highs yet again:

Source: goldprice.org 5 minutes ago.

It's a nice Christmas present. LYL is my largest real life position (13%) and it's also my largest position here on Strawman.com, and has been for a while. On top of the welcome share price uptrend I expect higher dividends from Lycopodium in calendar 2026 for the reasons I have previously outlined here.

Rather than issue new shares or take on debt, LYL's M.O. is to pay for acquisitions using their own cash, and that's what they did when the purchased 60% of SAXUM in February this year, and they reduced their dividends to replenish that cash balance. That's all done now, so I can't see why they won't return to paying out well-above-market-average dividends again now. I've always liked them because of their high quality and excellent management, and also because they provide growth plus income.

SAXUM provides Lycopodium with additional growth opportunities in the Americas as we've previously discussed, and I expect them to exercise their option to buy the remaining 40% of SAXUM when the time comes.

My wife finally got out of ICU yesterday after her open heart surgery on the 10th of this month, so she's in the cardiac ward and improving her strength and mobility every day. While she will almost certainly still be in hospital over Christmas, that's OK, the surgery was successful, she has two new mechanical heart valves and she doesn't have the lung fluid issues any more that caused breathing issues, so she is off the oxygen. We have our 30th Wedding Anniversary on New Year's Eve, so hopefully she'll be home by then, otherwise we'll celebrate that in hospital also. There's heaps to be very thankful for.

Wishing everyone in the Strawman community a very happy and peaceful Christmas and a Rockin' New Year! Stay safe, enjoy good times, family, friends, everything we are blessed with, and for those of us here in Australia, be thankful also that we live in the best country in the world!

Merry Christmas and a Happy New Year everybody!!

13-Nov-2025: Lycopodium held their 2025 AGM today and it gives shareholders a good chance to see how the company is progressing, and I'll break that down a bit in this straw.

LYL-FY26-Outlook--Guidance-(13Nov2025).PDF

Here's their FY26 Guidance from the announcement (link above):

And here's the guidance slide from the presentation today (link above):

Above, I've added the mid-points of those guidance ranges.

Here's how that guidance compares with their actual results over the past 5 years:

I've added the green guidance bars, as the graphed data in this slide only went up to FY25, as shown below:

It's probably a good idea to look at how the company has delivered on previous guidance. As a general rule, they have often provided guidance upgrades as the year progresses during prior years, and when they do report they usually hit the high end of or exceed their original guidance - in my experience - except for FY2025 when they walked away from two large projects for risk management reasons after spending significant money on those projects, one of those being Barrick's Reko Diq in Western Pakistan. I confirmed today that the other one was another Barrick project, the Lumwana copper mine in Zambia. More about Barrick in a bit, but I'm happy that Lycopodium pulled the plug on their involvement in those two projects.

For example, here's their FY25 guidance from November 2024:

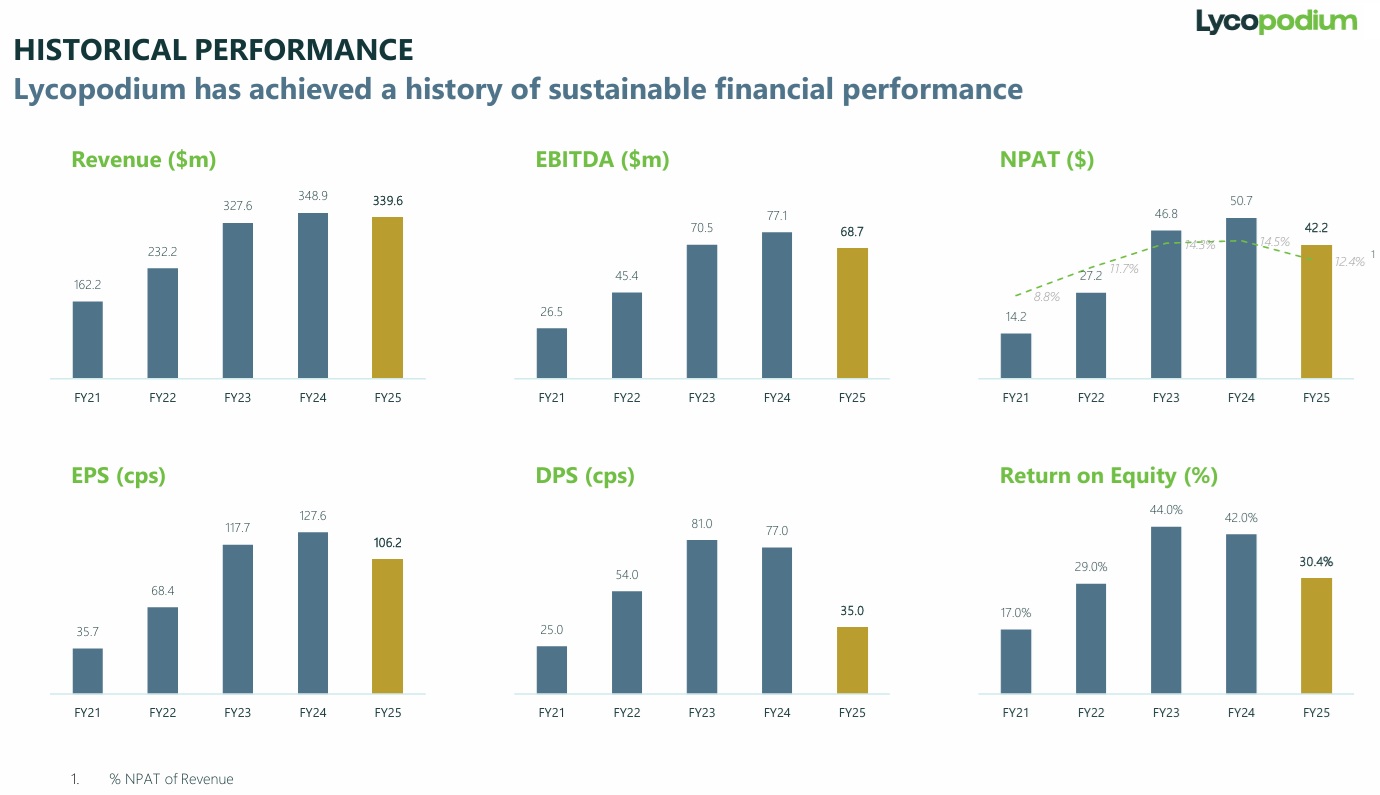

Source: FY2024 AGM Presentation.PDF [12-Nov-2024]

Their actual FY2025 results were $339.6m in Revenue and $42.2m in NPAT and a fully franked 10 cents/share dividend.

And below is their FY24 guidance from November 2023:

Their actual FY2024 results were Revenue of $348.9m and NPAT of $50.7m. FY2024 was typical of what I have observed with Lycopodium in terms of the company usually hitting the top end of their own guidance or exceeding guidance; they exceeded their revenue and NPAT guidance in FY24, as shown above.

So there's certainly scope for them to do the same in FY26. If they hit the top end of their FY26 NPAT guidance (being $44m), they will exceed their FY25 NPAT (of $42.2m), and they'll certainly well exceed their FY25 Revenue based on their current FY26 guidance of between $390m and $410m. And their dividends are almost certainly going to rise from FY25 levels when they were reduced to pay for the 60%-of-SAXUM acquisition (because they did not want to raise any capital or issue any new shares).

So, to recap:

There will be some margin compression this year, however they are still very profitable - their ROE has been over 30% for the past 3 years and over 25% for the past 4 years. They can afford to have some margin compression and still remain far more profitable than the majority of their peers, if not all of them.

Next, Growth:

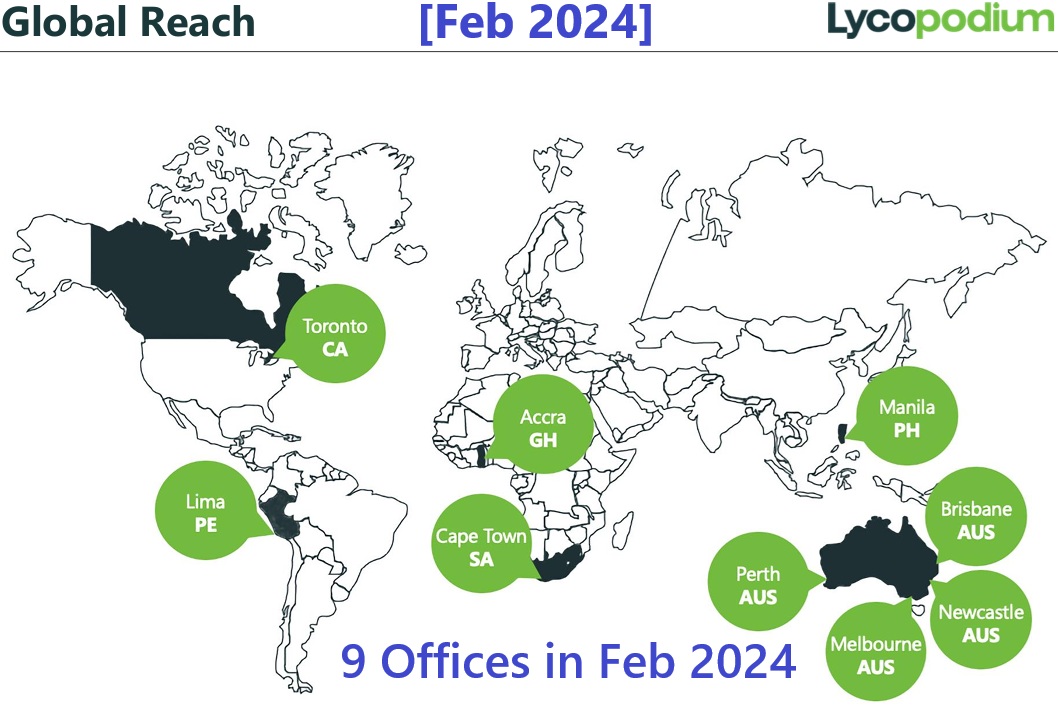

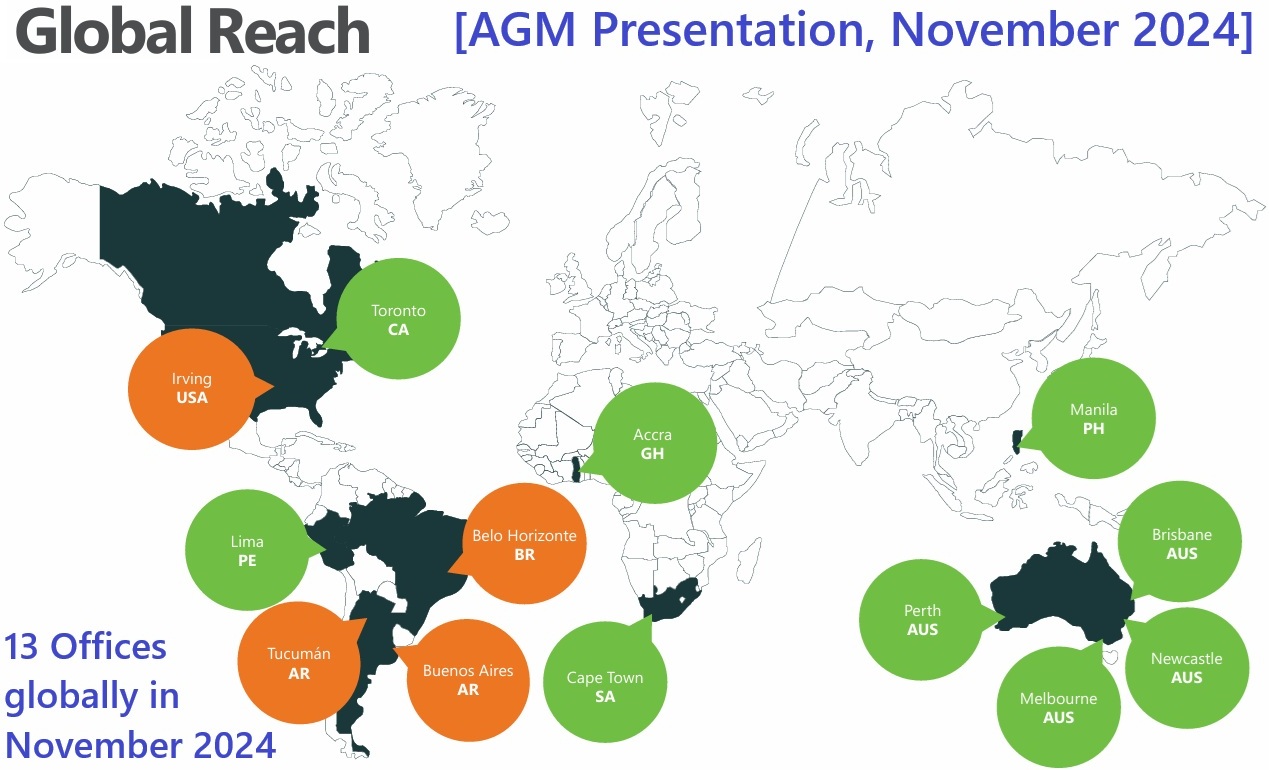

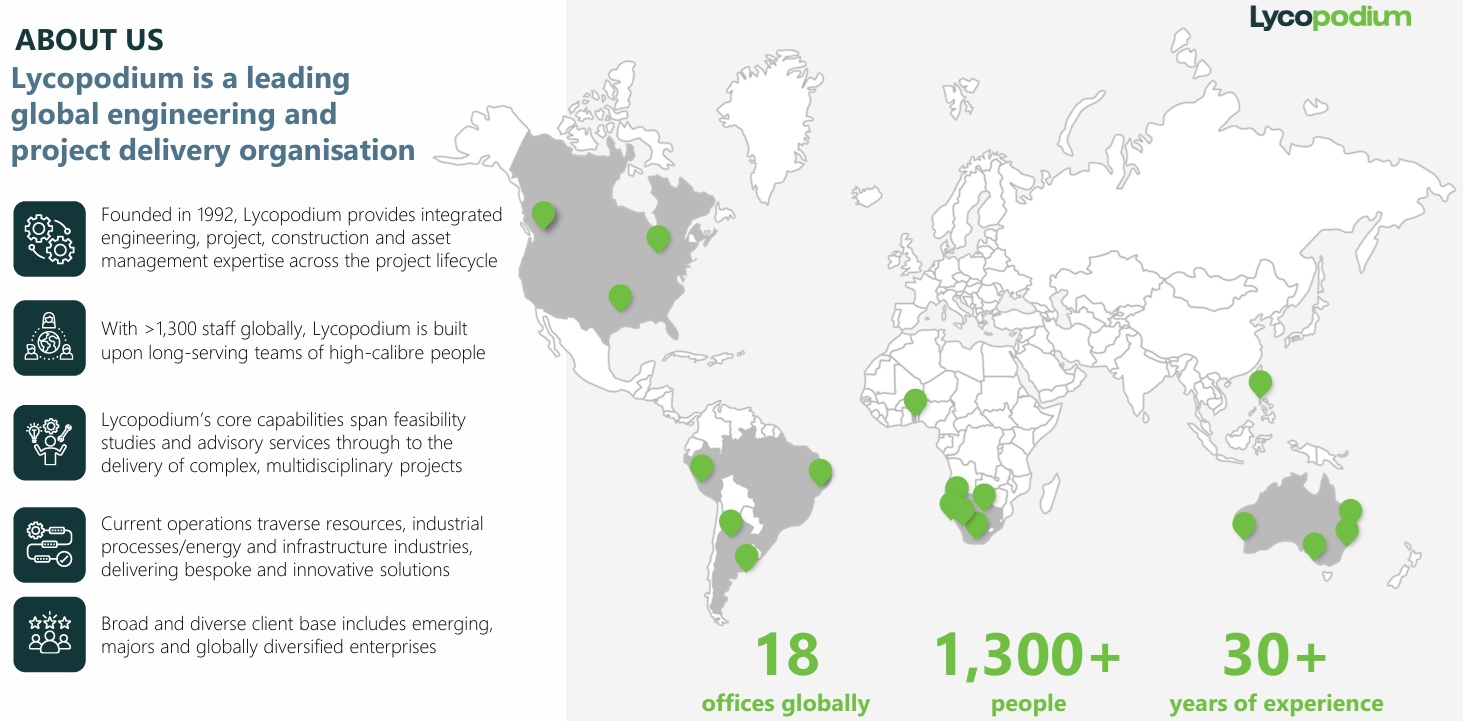

Let's look firstly at their global office count:

Source: Bell Potter Unearthed Conference Presentation.PDF [12-Feb-2024]

Source: FY2024 AGM Presentation.PDF [12-Nov-2024]

Source: Today's Presentation: FY25 AGM Presentation.PDF [13-Nov-2025]

So, from 9 offices in Feb last year to 18 offices today, and only one of those offices is in West Africa (in Accra, Ghana), and 5 offices in Southern Africa. This is important because while the majority of Lycopodium's revenue is still derived from Africa, much more of it is now coming from the South, and less from the West. There are a number of countries in West Africa where it is very dangerous to try to build or operate mines, especially gold mines, and that list of risky West African countries is growing. For instance, Burkina Faso is now on that list while Mali has been on it for a few years.

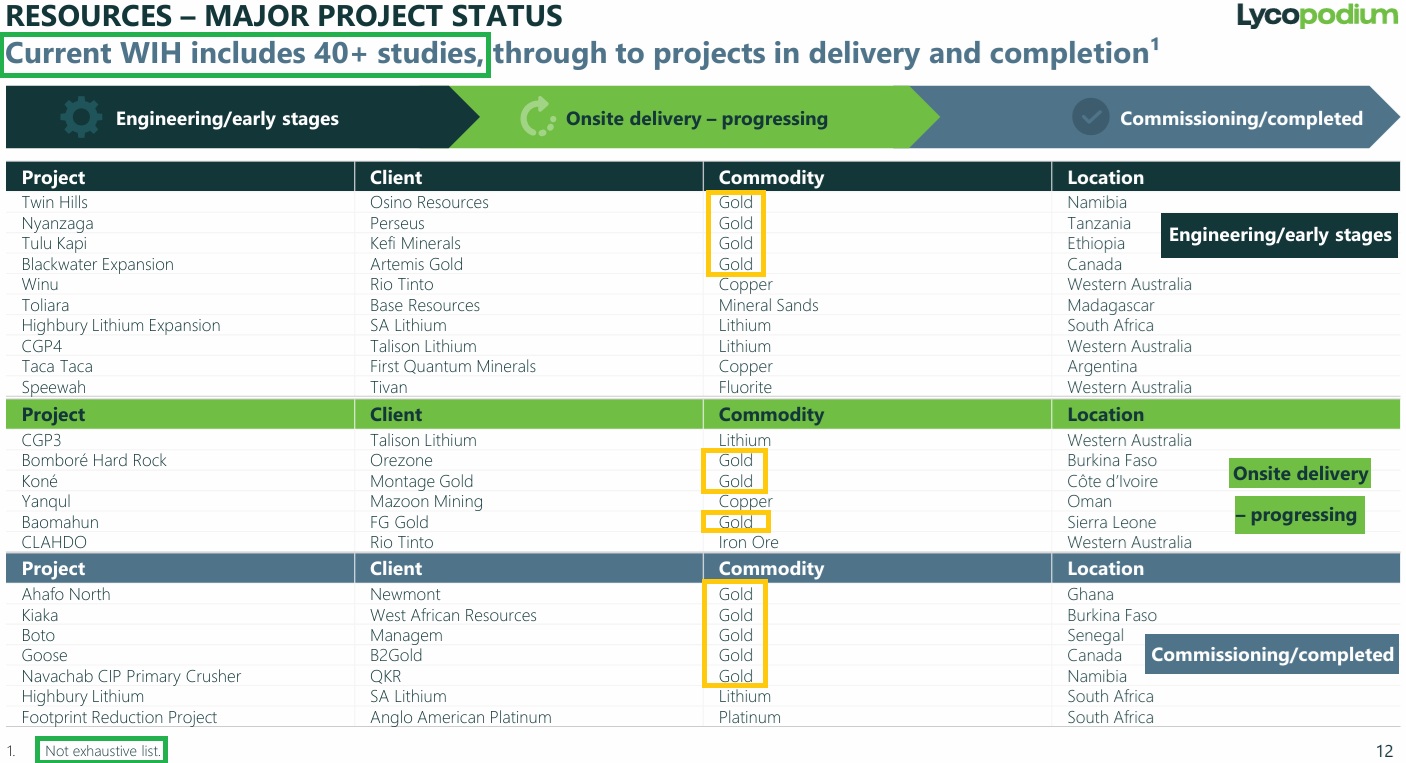

LYL included a slide in today's presentation titled "Disciplined Risk Management" and that is certainly one of their greatest strengths:

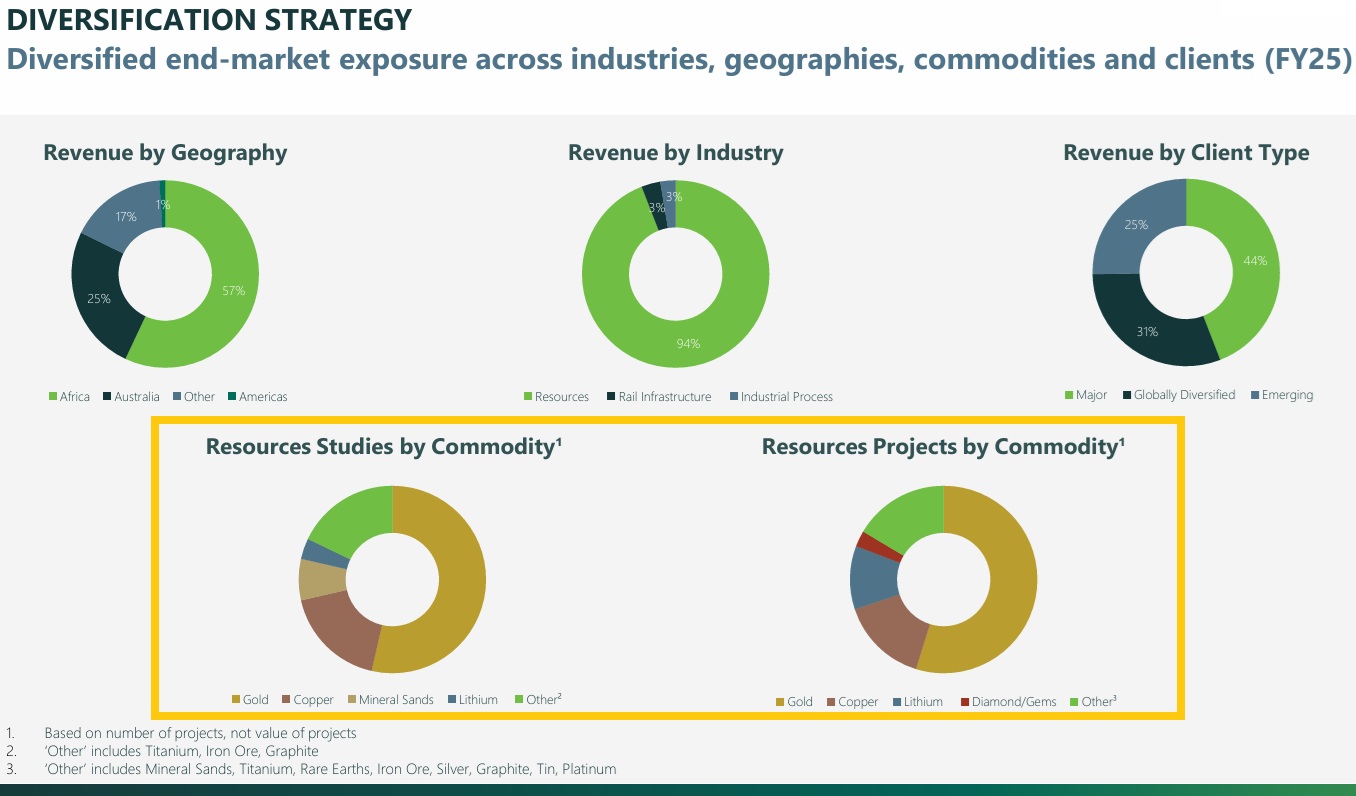

The top three charts below show their Revenue by Geography, Industry and Client Type. 94% of their revenue comes from Resources (mining) and 57% of their revenue is from Africa, but that is less than a few year ago when they were even more reliant on West African Gold Miners, and now/lately they have been gaining more work in Southern Africa and less in West Africa.

The bottom two charts show how much Lycopodium is exposed to the gold sector - a LOT! And that's a good thing because the sector has a very strong tailwind from the elevated gold price.

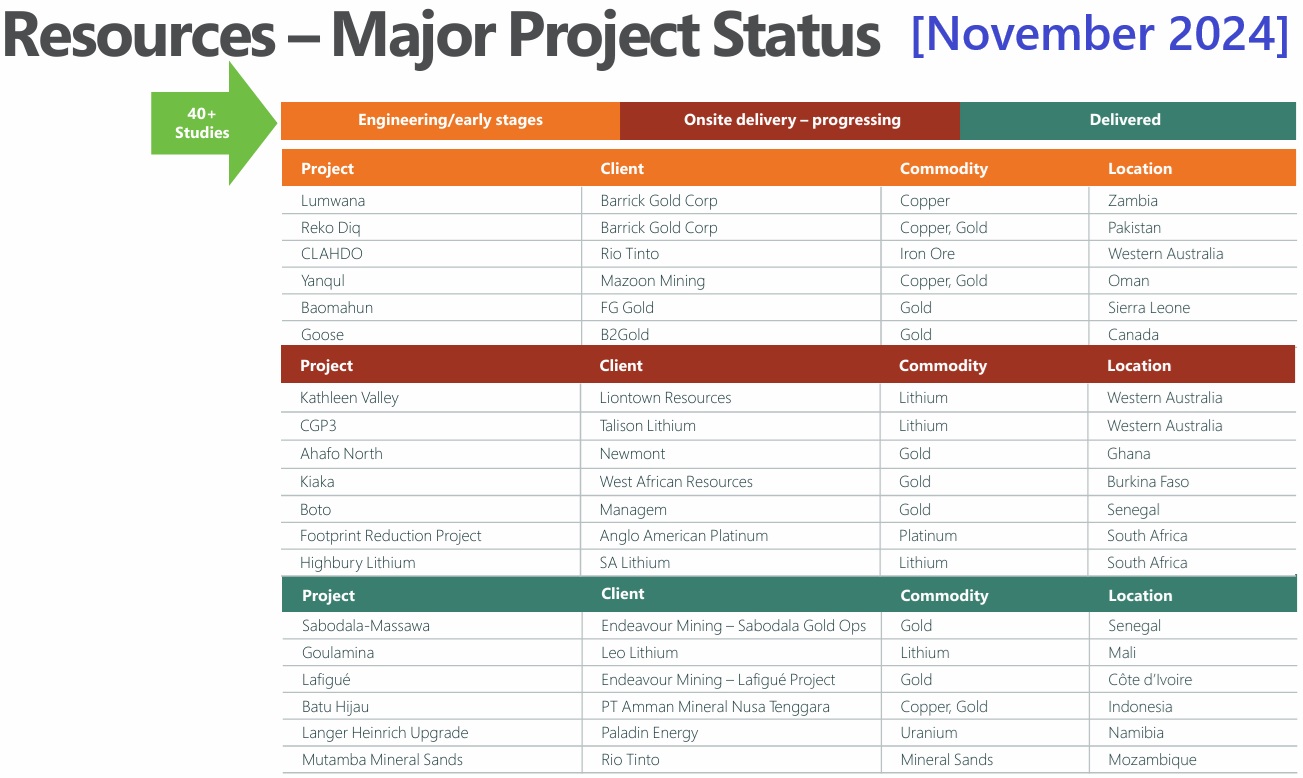

In terms of how busy Lycopodium are today, compared to how busy they have been recently, I'll include three slides below, the first from Feb last year, the next from November last year (2024) and the third one from today (November 2025):

Source: Bell Potter Unearthed Conference Presentation.PDF [12-Feb-2024]

Source: FY2024 AGM Presentation.PDF [12-Nov-2024]

Source: Today's Presentation: FY25 AGM Presentation.PDF [13-Nov-2025]

Compared to one year ago, they have one less project in the Delivery phase, one more project in the Commissioning/Completed phase, and they have 4 more major projects in the "Engineering" stage, and that's after walking away from Reko Diq and Lumwana, both Barrick projects. You can google Barrick if you're interested, however for today I'll just say that it was announced in late September that Mark Bristow has stepped down as president and CEO of Barrick Gold after nearly seven years in the role. In recent times it appears that he has embraced much riskier projects such as Reko Diq in Western Pakistan (Ballochistan), and diversified the company away from gold and more into copper and other metals.

One of his biggest moves recently was to refuse to negotiate with the military rulers of Mali where Barrick had some operating gold mines and as a result Barrick appears to have lost control of those mines and has now been shut out of the country. In fact the Malian authorities issued an arrest warrant for Mark Bristow so he can expect to be detained and/or locked up if he ever again sets foot in Mali.

There have been a number of allegations of human rights abuses during the period that Bristow has been in charge of Barrick Gold, and he got the company's name changed from Barrick Gold Corp to Barrick Mining Corp in May before quitting the company without any disclosed reason in September.

I had heard through the MoM podcast that there had been shareholder activism to either force Bristow out or to get the company to change direction or to split into two companies, the gold side and the rest. It appears that some large institutional shareholders were not pleased with Bristow's pursuit of copper projects in riskier locations and especially with the outcome of Barrick's gold assets in Mali which Barrick appears to have lost control of entirely.

Sources:

- https://mining.com.au/executive-exodus-hits-global-miners-barrick-mining/

- https://www.reuters.com/world/africa/mali-issues-arrest-warrant-barrick-gold-ceo-document-shows-2024-12-05/

- https://www.aljazeera.com/news/2022/11/23/tanzanians-sue-barrick-gold-in-canada-over-alleged-mine-abuses

- https://earthworks.org/blog/communities-call-for-respect-barrick-responds-with-aggression/

- https://www.proactiveinvestors.com.au/companies/news/1081743/newmont-barrick-gold-giants-circle-as-m-a-mood-returns-1081743.html

- https://discoveryalert.com.au/barrick-gold-leadership-dynamics-2025-market-impact/

- https://www.barrick.com/English/news/news-details/2025/barrick-announces-name-change-to-barrick-mining-corporation-and-election-of-directors/default.aspx

- https://www.streetwisereports.com/article/2025/10/13/whats-behind-shock-barrick-ceo-departure.html

Plenty of reading there if anybody is interested in one of the world's most stubborn (former) gold company executives, and the various perceptions of his performance and why he stepped down.

I have nothing but respect for Peter De Leo and his team at Lycopodium for declining to proceed with the bidding process for those big contracts at Barrick's Reko Diq and Lumwana copper projects in Western Pakistan and Zambia respectively. Barrick does not appear in Lycopodium's current "Major Projects" slide above, and that's a good thing in my opinion.

So Lycopodium is travelling OK in my opinion for a small Perth-based $500 million engineering company. They are really one of the quiet achievers in the Australian E&C (engineering and construction) sector who does most of their work overseas.

Source of slide above and the ones below: Today's Presentation: FY25 AGM Presentation.PDF [13-Nov-2025]

That slide a little larger:

Source: Today's Lycopodium AGM Presentation: FY25 AGM Presentation.PDF [13-Nov-2025]

So, yeah, all good. Nothing of concern. Happy to have this as one of my top two positions IRL and my largest position here on Strawman.com. Currently my GNG position IRL has a higher market value than my LYL position because GNG's SP has risen more in recent days than LYL's has, however I like them both equally (a lot!) and happy for them to be my top positions. I hold both in my income portfolio (outside of my SMSF because my SMSF is limited to ASX300 companies and neither LYL or GNG are in the ASX300 index).

GNG is a very similar company but GNG do most of their work here in Australia and LYL do most of theirs overseas. Both of them specialise in the design and construction of gold mills, and both have a strong gold price tailwind.

Disclosure: Held, LYL has a 12.1% weighting in my real money portfolios, GNG is 12.4%. Those are my top two positions and together they represent 24.5% of my real money sharemarket investments at current share prices (13-Nov-2025).

19-Sep-2025: Lycopodium (LYL), my largest real life position, went ex-div yesterday (18th Sept) for a 25 cent fully franked dividend, however their SP actually rose +13 cents after rising +16 cents the previous day (Wednesday 17th) - and then they fell today (the day AFTER they went ex-div) by -28 cents, closing at $12.01.

Their trading range today was as low as $11.96 up to a day high of $12.29. So, two points - one is that the new baseline downside resistance level seems to have moved up from $10/share to $12/share, or that's how it looks to be shaping up to me anyway - and they held that level today (closing at $12.01 despite going ex-div yesterday), and secondly we now have their two lower dividends behind us (the FY25 half and full year divs) and if I'm right in my interpretation of Peter De Leo's guidance, it should now be back to their higher dividend payout ratio going forwards.

So we should get the continued growth plus the higher dividend income aspect back as well. Income + Growth.

Unless there's another self-funded acquisition of course. And that would just delay the income bit and assist the longer term growth, so either way I'm happy.

Remember:

- Stable share count for over a decade;

- Zero Debt;

- Conservative Management;

- Tailwinds - they design and build gold processing plants - yeah, they do other things too but that's what they specialise in, and;

- Excellent M&A history, and superb capital management in every other respect also.

And I reckon we're back to higher-than-market-average dividends as well now.

Disclosure: Held.

20-Aug-2025: Nothing alarming in this report, but the market clearly would have preferred a better set of numbers based on LYL being sold down a little on the results after a decent run-up over the past few weeks, so trading right now - @ $11.76 - at the same levels they were on August 8th and also through the second half of July, and still above where they were trading throughout the majority of the 8 month period from mid-November through to mid-July.

There was a fair bit to unpack, so I'll try to cover off the more important stuff. Firstly, I'm happy with the report, and the dividend. I would have preferred a higher dividend, as in a return to the circa-36 to 45 cps final dividends we have seen over the past three financial years (prior to FY25), but this slide from their presentation makes it clear that their dividends will return to normal levels in FY26:

The bit I've highlighted there in green (above) is why I think the lower dividends are now done (after the 25c FF one they just declared). Importantly, they still have a super-strong balance sheet and have accumulated an even higher cash balance:

And they have a growing pipeline of work:

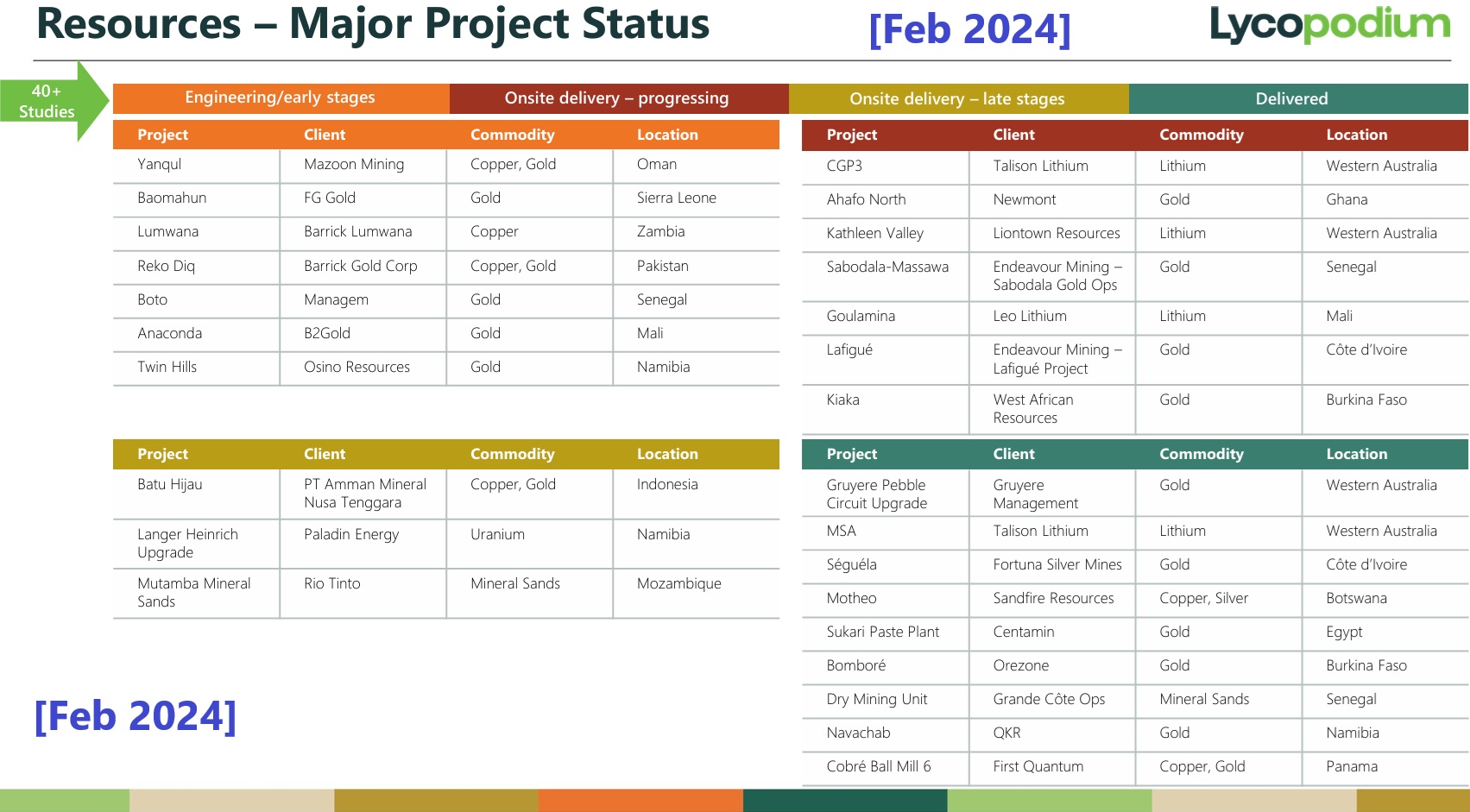

They have more than 40 studies ongoing plus 10 major projects in Engineering/early stages, another 6 major projects being delivered currently, and another 7 that have either been recently completed and/or are in the commissioning phase currently, as shown above. While that table only covers their Resources division, that's the one that matters most, as shown below:

Around 94% of LYL's revenue is derived from that Resources division, and only 6% from Industrial Processes and Rail Infrastructure combined (circa 3% from each of those).

Here's what Peter De Leo, their MD & CEO had to say in today's report to shareholders for FY25:

I'm going to skip now to what he said about their Resources division:

They remain busy!

Here's what he had to say about their outlook:

It's fairly positive, remembering that Peter and his team are one of the most conservative management teams I've come across in terms of being careful to never overpromise and risk underdelivering later. The SAXUM majority acquisition - with an option to buy the remaining 40% later - should not be underestimated in terms of LYL getting a solid foothold in South America and the work that's going to bring in for them in future years.

Here are their historical results against FY25:

Sure, FY25 was down on FY24, but we knew that, it was flagged at their AGM last year (in November) and again in February with their H1 results; Both revenue and NPAT achieved in FY25 are at the top end of the guidance they provided in February (Full Year Guidance: Revenue $320m - $340m, NPAT $37m - $43m).

They're in good shape - and the nature of their E&C work is that revenue and earnings will be lumpy, but they're growing over time, you have to zoom out a little with these sorts of companies and look at their overall trajectory rather than just a single year.

Importantly, they're set up for a good couple of years from here by the looks of that.

Sources: LYL-Full-Year-Results-Announcement.PDF plus FY2025 Investor Presentation.PDF plus FY2025 Shareholder Report.PDF plus FY2025 Financial Report.PDF.

My investment thesis remains intact for Lycopodium. Still my largest real money position and one of my largest positions here on SM as well.

12-August-2025: MoM Podcast: Booms, Busts & Billion-Dollar Builds (Zimi Meka) (Ausenco)

Zimi is the founder of Ausenco which was ASX-listed but was taken private in 2016. They are a serious competitor of Lycopodium (LYL) because they love working in the world's more dangerous locations. Zimi even mentioned that he was recently asked to look at a project in Western Pakistan (Reko Diq) which he said they would be willing to take on with the appropriate controls - that's one that LYL recently passed on after doing all of the feasibility studies and FEED work.

Very interesting interview.

Ausenco continues to operate as a private global consulting, engineering, and project delivery company after its delisting from the Australian Stock Exchange in 2016 and subsequent sale to U.S. investment firms in September 2023. The company was acquired by Resource Capital Fund VI (RCF) in 2016, taking it private, and was then sold by RCF to a consortium of Eldridge, Brightstar Capital Partners, and Claure Group in 2023.

They are not listed on any stock exchange now, but they are a competitor of Lycopodium.

Worth noting however that Ausenco's specialty is copper, while Lycopodium's is gold, however they both work on a variety of minerals and metals processing plants including base and precious metals.

Disc: Holding LYL.

30th July 2025: Nyanzaga-Gold-EPCM-Contract-Award.PDF

More work for LYL in Africa, but not Western Africa this time. It pays to note that this is the 3rd time Perseus Mining (PRU) have contracted Lycopodium to deliver an EPCM contract (build a gold mill) for them in Africa, so clearly Perseus is happy with LYL's work.

LYL is after all the very best at what they do, in Africa in particular. Their mills get built on time and on budget and those gold mills work as planned, and Lycopodium know how to manage risk in some of the world's riskier locations.

Disc: Holding (my largest position in real life and one of my top two largest positions here on Strawman.com).

P.S. Looking forward to their full year report in August! And what they do with their full year dividend.

Further Reading:

Thursday 10th July 2025:

Looking like a good setup to me. We just need a good report from Lycopodium next month and a resumption of their higher-than-market-average dividends, and we're away. Context: LYL is my largest position both here and across my real money portfolios, so I'm clearly biased towards the company.

Their only announcement during the past 6 weeks has been a Change-of-Director's-Interest-Notice.PDF showing that Bruno Ruggiero sold 650,000 LYL shares on June 17th for $6,750,705 being @ around $10.39 each in an off-market transaction.

Bruno is an Executive Director at Lycopodium and also their Technical Director, overseeing the company's technical knowledge base, capabilities, and direction, alongside their MD, Peter De Leo. Bruno's responsibilities include extensive project involvement, strategy development, and the delivery of technical solutions in its EPC (Engineering, Procurement, and Construction) business.

Bruno is also a Non-Executive Director at ECG Pty Ltd and is the Board Chairman at Quantum Graphite Ltd (ASX:QGL). Bruno is also a director of Sherwood Utilities Pty Ltd and has interests in two companies (Luala Pty Ltd & Ziziphus Pty Ltd) that between them hold all of his 1,000,520 remaining LYL shares. One or both of those two (Luala & Ziziphus) are probably corporate trustees for family trusts or similar. Bruno also holds 52,047 Class A Performance Rights.

It was a big sell down ($6.8 mill), but he still owns over $11 million worth of LYL shares plus the performance rights. He also holds more than $10 million worth of QGL shares (where he is their Chairman).

The market doesn't seem overly worried about it. Peter De Leo (their MD) still holds 920,200 LYL shares, so Bruno is still ahead of Peter with his remaining 1,000,520 LYL shares. Their Board Chairman, Rod Leonard, owns 902,930 LYL shares.

There's plenty of skin in the game at both Board and C-suite level.

Here's LYL's graph for the past 5 years:

I believe that part of the reason for the SP fall in the latter half of last year was that a couple of microcap fund managers who held LYL may have reduced or exited their LYL positions when they realised that the company had gone cold on the massive Reko Diq Copper-Gold Project in western Pakistan (Ballochistan) and that LYL were not going to bid for the big EPC/EPCM/EPM contract to build Reko Diq. With LYL having done the feasibility studies and then the early works at Reko Diq, it was assumed by many that Barrick Gold would award the contract to build the plant to LYL in early 2025, and that would have been Lycopodium's largest contract ever if that had ocurred.

Peter De Leo confirming during their February half year results conference call that they had withdrawn from the bidding process for two large projects on the basis of a poor risk/reward trade off - basically the projects were just too high risk and the project owners were not prepared to adequately compensate LYL for taking on that very high risk - and we know that Reko Diq was one of those two projects, and that Reko Diq is likely to be a very dangerous and challenging build for whoever ends up with that contract.

We commented here at that time that this was actually a really good move and demonstrated why LYL continue to be so highly profitable - they don't take on projects that end up being loss making, they are disciplined with their tendering, and are very switched on across their risk management.

They don't lower their prices to fill their order book. Margins are maintained.

They then reduced their half year dividend (in Feb) to allow them to fully fund their part-acquisition (60%) of SAXUM using their own cash reserves rather than having to take on any debt or issue more shares.

LYL remain in a net cash position with a share count that has been stable for over a decade, so they have not issued shares to fund acquisitions OR used debt.

The purchase of 60% of SAXUM (announced in October and completed in February) only cost them US$7.1 million, so I am assuming they can and will (or are likely to) resume their previous high dividend payout ratio now, which should be confirmed with their full year results next month. If not in Feb, then I would expect it to be in August at the latest.