RPM Global (RUL) is a company I've liked for a few years and have held on and off (currently not holding). I was looking at their share price graph yesterday (Sunday March 16th) and their P/E ratio, which is still very high despite their share price having come down from around $3.35 to $2.57:

Commsec has RUL's P/E ratio listed as 62.35 and their market cap was $575.12m according to the ASX website, which tends to be more accurate with market caps than Commsec is. The ASX site has RUL's P/E ratio listed at 87.47 Their actual market cap should be 222,055,199 (shares on issue or SOI) x $2.55 (Friday's closing share price) = $566.24 million, so their true PE ratio based on their last full year NPAT ($8,656,000 - see here: RUL-Appendix-4E-year-ended-30-June-2024.PDF) should be $566.24 (P) divided by $8.656 (E) (with both figures in millions of dollars) = 65.42.

So a trailing P/E ratio of 65.42 based on their FY24 earnings.

What the ASX appear to be doing is adding together their two 6-month NPAT numbers from their two most recent halves to arrive at the "E" (earnings), so their recently reported FY25 H1 NPAT of $4.734m added to their previous half (H2 of FY24) NPAT of $1.813m to get $6.547m for the 12 months ending 31 December 2024, and that would give us a PE ratio of 86.49 (566.24 / 6.547), which isn't far from the ASX's trailing P/E ratio for RUL of 87.47.

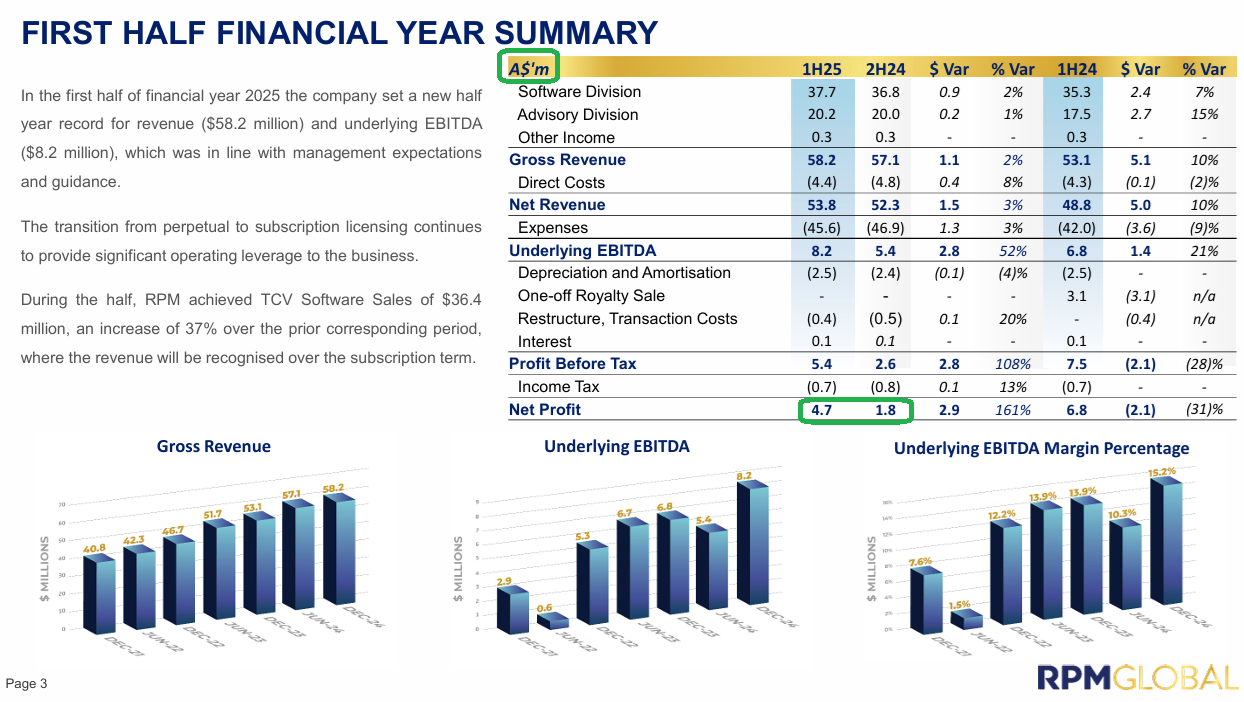

In the following slide from their latest results release, you can see that RUL have rounded down those two NPAT numbers to $4.7 million and $1.8 million, so together that's $6.5 million. If you use that rounded down number ($6.5m instead of $6.547m) it results in a slightly higher P/E ratio of 87.11 (566.24 / 6.5).

If you instead use these numbers on a "per share basis", which also works out the same, the "P" is the current share price of $2.55 (Friday's closing price) and the earnings per share per year have been 2.948 cents/share or $0.02948/share ($6,547,000 NPAT divided by 222,055,199 SOI) for the 12 months ended 31 December 2024, so the P/E ratio is 2.55 / 0.02948 = 86.49.

For the 12 months ending 30 June 2024, the per share earnings are 3.898 cents/share or $0.03898/share (8,656,000 / 222,055,199) so the P/E ratio would be 2.55 / 0.03898 = 65.42.

So on the basis that a P/E ratio is designed to provide a number that represents how many years it would take for the company to earn the amount that you paid for the shares, it would take more than 65 years for them to earn (in NPAT) the amount that you paid for the shares, if you bought them at Friday's closing price of $2.55, and on that basis RUL look very expensive. This is however fairly typical for capital light software companies who are considered leaders in their field. Consider the following:

Company, P/E ratio according to Commsec / P/E ratio according to the ASX website

- Xero (XRO), 108.88 / 123.69

- WiseTech (WTC), 84.69 / 88.45

- TechOne (TNE), 72.81 / 77.44

- Hansen Technologies (HSN), 31.24 / 280.18

- Objective Corporation (OBJ), 58.79 / 44.70

- RPM Global (RUL), 62.35 / 87.47

These are all trailing PE numbers and that's important (more on that in a minute). It appears that Commsec uses the earnings number for the last full completed financial year and the ASX uses the earnings number from the last two 6 month periods added together - such as H2 of FY24 plus H1 of FY25, which is why the P/E numbers can be so different if there's a particularly weak or particularly strong half in there that the other mob are not including. Point is though, that these are all high P/E numbers.

Compare that to the much lower P/E ratios for some of the largest US Tech companies:

Company, trailing PE / Forward PE (based on projected earnings)

- Alphabet (Google), 20.58, 18.83

- Apple, 33.89, 29.15

- NVidia, 41.38, 27.10

- Amazon, 35.80, 30.03

- Meta (Facebook), 25.47, 23.92

- Broadcom, 90.53, 30.03

- Oracle, 35.28, 23.37

- Microsoft, 31.29, 30.21

Makes Google look cheap, eh!

Trailing P/E ratios, such as those I've quoted for all of those ASX-listed companies above, and the first of the two numbers to the right of those US-listed companies above, are based on historical earnings, so they are backwards looking, not forward looking. Forward P/E ratios are based on consensus estimates of current or future year earnings, and are therefore only as accurate as those earnings estimates are.

The thing about these sort of companies, particularly SAAS companies, is that they tend to be capital light and they usually scale really well without much in the way of additional expenditure, so additional revenue tends to drop through to the bottom line, because most of their costs are fixed costs which don't increase much - or at all - with additional revenue. In other words, these companies can handle more customers and increased sales without any significant increase in costs.

Because of this, if you believe that the company is going to continue to grow sales at a good clip, it's reasonable to also expect a corresponding increase in profits.

So that's one reason why quality SAAS companies that are ASX-listed tend to trade on high P/E ratios, because people can easily see a pathway for that company to keep doubling in size every few years, due to low costs, being capital light, and having a long growth runway based on these companies providing software that companies/people need.

The better ones also have low churn because switching costs can be significant in terms of both money and time, plus risks of things going wrong during a switch and negatively impacting that company's own clients.

Some other factors that should be considered are R&D and/or NPD (new product development) spending (costs). Most of those companies have a decent R&D+NPD spend every year, and they need to spend that money to both stay ahead of their competition and stay relevant, as well as to move with the times, for example to add additional capabilities that their customers either require or are likely to require in the future. Companies that do NOT continue to innovate and offer more to their customers/clients over time tend to fall behind and lose customers and/or just grow at a slower rate.

Much can be learned from studying the track record of these companies to see how they've handled these issues in prior years, looking at annual R&D spend, churn rates, etc., but over multiple years, not just one or two years.

The next major factor, as I see it, is M&A plus other capital allocation decisions by management. This is important because no matter how good and how profitable a business is, it can still be a bad investment if the management make poor capital allocation decisions, such as overpaying for assets and then booking impairments (value write-downs) in future years. Other capital allocation decisions can include dividends (including special dividends) and share buy-backs.

For instance, RPM Global (RUL) have an active share buy-back in place and they are lodging notices daily to show how many shares they have bought back and cancelled. This is often a sign that a company considers their share price to be too low, meaning they believe that their own share price does not reflect the value of the business, so buying back their own shares and cancelling them is - in their opinion - a good use of their money (or "our" money if you're a shareholder). That also has to be balanced against other opportunities, such as M&A opportunities (inorganic growth), dividends, etc.

In RUL's case, because they are a capital light business with ROE around 16.5% (according to Commsec) and an $18.7m cash balance at December 31st, with zero debt, if they truly believe their share price significantly undervalues the company, then an active share buy-back does make sense, IMO.

In general, P/E ratios tend to be higher in fast growing, capital light businesses such as SAAS companies, but the examples I have given in the lists above highlight that ASX-listed SAAS companies tend to be a lot more expensive than US tech companies, and one possible reason is that people see how succesful those US tech companies tend to be, and the share price appreciation they have demonstrated, and they extrapolate that across to our market and are looking to get exposure to similar companies on the ASX.

In my opinion, for the most part, that's not really an apples v. apples comparison.

The IT (information technology) sector on the ASX is tiny - around 3.2% of the S&P/ASX 200 index (our top 200 companies) - one of our smallest sectors, whereas over in the USA their IT sector is massive. It's their largest sector by a good margin.

Source: https://www.usbank.com/investing/financial-perspectives/market-news/investing-in-tech-stocks.html [07-March-2025]

The US IT sector, encompassing software, IT services, and related industries, contributes around 8.9% of the US GDP and accounts for a significant portion of the global IT market. And IT companies dominate the US market:

Point is, with good tech companies, there's plenty to choose from in the US, and over here, not so much, so the few decent IT companies that we do have tend to have high P/E ratios and look expensive, because there's greater demand for fewer companies.

The problem with that however is that the market is prepared to pay more for future growth, or, to put it another way, there's already substantial future growth already priced in with high PE companies, so the downside is if they stumble along the way, the share price can "correct" swiftly and the movements can be large in percentage terms. One way of looking at it is that some companies are priced for perfection, and if EVERYTHING doesn't go to plan, i.e. if ANYTHING goes wrong, that big growth and quality premium in the share price can drastically reduce or evaporate entirely.

Oftentimes, the share price will get back up to higher than where it fell from given a few months or years - as long as no further hiccups are encountered, but the ride can get bumpy.

Another consideration is that many of those giant US tech companies totally dominate the market globally, whereas our tech companies are a LOT smaller, many of them focus primarily on Australia - so have a much smaller addressable market - and do not have the same advantages that the big US tech companies have, such as massive economies of scale advantages, and being clear global market leaders.

For these reasons, I am usually only prepared to pay 40+ P/E for companies that I am very bullish on longer term and where I have a very high conviction that they will grow into their current valuation given time. I would need to have a 10 year plus timeframe for a company trading at a 60+ P/E ratio, AND be very bullish on their long term growth, AND be very happy with their management, including their track record of M&A and other capital allocation decisions.

Because, in that case, I am not expecting the company to take 60+ years to earn the equivalent of my purchase price (what a 60+ trailing P/E ratio suggests) because I am expecting that P/E ratio to reduce based on my buy price and their growing earnings. In other words, I am expecting the "E" to expand a LOT in the coming years, while my "P" remains constant (what I paid for the company's shares) so that means the ratio between the P and the E reduces quickly.

In RUL's case I don't have that level of conviction, so I'm not holding at this point in time. I still like the company, but I don't consider RPM Global to be one of the very best risk/reward opportunities across the market for me right now.

Further Reading regarding the basics of P/E ratios:

Google says:

Average market P/E ratios, which are calculated by dividing the market capitalization by the total annual earnings, provide insight into how the market as a whole is valuing its companies, indicating whether the market is generally overvalued or undervalued, and reflecting investor sentiment about future earnings growth.

Here's a more detailed explanation:

What P/E Ratio Measures:

The P/E ratio, or price-to-earnings ratio, is a key valuation metric that shows how much investors are willing to pay for each dollar of a company's earnings.

How it Reflects Market Valuation:

A high average market P/E ratio suggests that investors are willing to pay a premium for earnings, potentially indicating optimism about future growth and a perception of the market as overvalued. Conversely, a low average P/E ratio could suggest that investors are pessimistic about future earnings or that the market is undervalued.

Investor Sentiment:

The P/E ratio also reflects investor sentiment and expectations about future earnings growth. A high P/E might suggest that investors anticipate strong future growth, while a low P/E could indicate that investors are skeptical about growth prospects.

Comparison over Time:

Tracking the average market P/E ratio over time can help identify trends and potential valuation extremes. For example, if the P/E ratio is significantly above its historical average, it might suggest that the market is overvalued and could be at risk of a correction.

Limitations:

It's important to note that P/E ratios are just one metric among many, and should be considered in conjunction with other factors, such as industry trends, economic conditions, and company-specific fundamentals.

Example:

If the average market P/E ratio is 20, it means that investors are willing to pay $20 for every $1 of earnings, while a P/E of 10 would mean they are willing to pay $10 for every $1 of earnings.

--- ends ---

And when I ask Mr Google: What is the average PE ratio of the ASX

Google answers:

As of March 16, 2025, the average P/E ratio for the S&P/ASX 200 is around 15.7.

Here's a more detailed breakdown:

Historical Context:

The long-term trend for the P/E ratio of the Australian market is around 15.

Recent Fluctuations:

While the average is around 15, it has seen some fluctuations in recent years.

Comparison to other markets:

The ASX 200's P/E ratio is generally considered to be relatively low compared to some other major global stock markets, such as the S&P 500.

Factors influencing P/E ratio:

The P/E ratio can be influenced by factors such as earnings growth, interest rates, and investor sentiment.

Interpreting the P/E ratio:

A lower P/E ratio can indicate that a stock or market is undervalued, while a higher P/E ratio can suggest that it is overvalued.

--- ends ---

So, yes, any company trading on a PE of over 40 has a LOT of future growth ALREADY priced in, and I guess the main questions are:

- Do you agree that there's that much upside (profit growth) in this company and are you prepared to pay up for the company's shares now and then wait years for that upside to occur?

- And will it be worth the wait?

- Will the company deliver on its potential in the timeframe you expect them to?

- Are you prepared to ride out significant share price volatility if they stumble along the way?

When a company encounters a hurdle and stumbles or makes a misstep, and the company's share price drops significantly, you'll often hear people say that the market has overreacted to the downside, but those people may not realise that the market had already previously overeacted to the upside by bidding that company's share price up to priced-for-perfection levels, and so the "correction" that they are observing may be exactly that - a correction, to around where the company SHOULD have been trading, without all of that hype and euphoria priced in.

I'm not really commenting on RUL specifically here, because I haven't been following them closely lately, so I don't know their particular situation well at this point, but I'm just making general comments about high PE companies. Sometimes the earnings grow into the PE, and sometimes they don't, so the PE instead corrects by the price reducing.

27-Oct-2022: According to RUL's FY21 Annual Report, their substantial shareholders were:

- Perennial Value Management Limited with 9.75% (22,589,175 shares);

- Regal Funds Management Pty Limited with 5.93% (13,746,571 shares); and

- First Sentier Investors with 5.47% (12,677,670 shares)

...as listed at the bottom of this screenshot from Commsec today:

First Sentier Investors (formerly Colonial First State Global Asset Management) is a global asset management group that is now owned by Mitsubishi UFJ Financial Group, Inc., who also own Carol Australia Holdings Pty Limited. You will see above that Mitsubishi UFJ FG/Carol Australia reduced their RUL position from 6.69% to 5.21% on 12-Nov-2021 (circled above in orange). Regal's most recent notification was on 14-Sep-2022 to say that they were no longer substantial shareholders of RUL (circled in red above). All subs that have now ceased to be subs have been highlighted in red above. Remember that the most recent trades are at the bottom of that list, with the older ones at the top. The "Substantial Shareholders List" at the bottom left was only current back at the time of the 2021 annual report, so valid at 30-June-2021, and all of those shareholdings have since changed.

Perennial ceased to be subs on 11-Nov-2021, then became subs again on 01-Dec-2021, then increased their position through Feb, March and April this year, then bought more again in July, so Perennial now hold 10.43% of RUL.

It looks like Perennial bought a chunk of Clime's RUL shares back on 04-Feb-2022, which was when Clime Investment Management ceased to be substantial shareholders.

There is one new name there. Well, two. Comet Asia Holdings II Pte Ltd and Superannuation and Investments HoldCo Pty Ltd. They are both basically KKR - which is Kohlberg Kravis Roberts & Co. L.P., one of the largest private equity (PE) groups in the world. KKR are the majority owners of Colonial First State (CFS) - see here: Colonial First State welcomes KKR as majority shareholder and embarks on new phase as a standalone business (cfs.com.au)

...not to be confused with Colonial First State Global Asset Management, which was sold off to Mitsubishi UFJ Financial Group and rebranded as First Sentier Investments.

Where I've circled two names together and they both have identical shareholdings, it's the same shareholding, because one of the names is the registered owner of the shares, and the other one is the majority owner of the first company, so has to lodge a mirror notification in the same way that every time Brickworks lodges a subs notice for one of the many companies they are substantial shareholders of, Washington H Soul Pattinson and Co (SOL) also has to lodge a virtually identical notice because Brickworks (BKW) is regarded as a controlled entity of SOL (SOL own 43.2% of BKW and BKW own 26.14% of SOL), but they're not two different shareholdings, they are the same shareholding that is controlled by two different companies, because one of those companies is regarded as a controlled entity of the other company.

In the examples above, Carol Australia is a controlled entity of Mitsubishi UFJ, and both Comet Asia Holdings II and "Superannuation and Investments HoldCo" (S&I HoldCo) are entities controlled by KKR, so either Comet is regarded as being a controlled entity of S&I HoldCo - or S&I HoldCo is regarded as being a controlled entity of Comet Asia Holdings II. Either way it's the same shareholding.

So according to Commsec, the current substantial shareholders of RUL are:

- Carol Australia Holdings Pty Limited/Mitsubishi UFJ Financial Group, Inc., with 5.21%;

- Superannuation and Investments HoldCo Pty Ltd/Comet Asia Holdings II Pte Ltd, with 5.27%; and

- Perennial Value Management Limited, with 10.43%.

Of those the only one worth taking any notice of is really Perennial, in my opinion.

While not a substantial shareholder, Forager Funds do currently list RUL as the largest position in their Forager Australian Shares Fund (ASX: FOR).

Both Perennial and Forager are fundies that are best described as "value investors", so they look for growth companies at really good prices. Neither seem to like to pay up for quality or growth, they prefer to wait until such companies are looking very undervalued before they buy. It is probably best to look at the prices that RUL was trading at - at the times that those guys were buying. In Forager's case, they bought either all or most of their RUL in 2019 for less than 90c/share.

You can see when Perennial have been topping up above, but they have been on the RUL share register for a couple of years now as well. The last time Perennial bought more RUL was in early July, when RUL were trading at around $1.50 to $1.60/share. Prior to that, they were buying in late April at around $1.70 to $1.80. They were also buying in early Feb and mid-March at around those same $1.70 to $1.80 levels, which is not too far from where RUL are trading now. They closed at $1.79 on Wednesday and then at $1.89 today (Thursday 28-Oct-2022) after rising 10c (or +5.59% on a positive day for our market).

Perennial have been increasing their RUL position gradually since December 1st, so for the past 11 months roughly (as it's nearly the 1st November). Back in late November/early December, Perennial was paying just over $2/share for RUL. All of their top-ups since then have been at lower levels however, mostly between $1.70 and $1.80/share and more recently at $1.50 to $1.60. Perennial do tend to play the long game, much like Forager do, so that's worth considering also. Their typical investment horizon is probably 5 to 10 years, but no less than 3 years, I would imagine.

Source: Commsec. Edited by me (to remove clickable links).

Here is what the RUL Board members own in terms of skin in the game:

Stephen Baldwin is their Chairman and Richard Mathews is their CEO and MD. They hold 3.7m and 8.2m RUL shares respectively.

Disclosure: I do not currently hold RUL shares, although I have done in the past, and have made money holding them.

27-Oct-2022. As well as the Moelis report on RUL that @Remorhaz mentioned today, there are a few other brokers and analysts who have covered RPM Global (RUL) in the past, and may still do. Here are some links to their reports from prior years:

27-Oct-2019: Taylor Collison: RPM Global (RUL) - Initiating coverage: 5 reasons to buy

10-Feb-2020: Taylor Collison: RPM Global (RUL): Recent update, accounting changes, review of competition

26-Mar-2020: Taylor Collison: RPM Global (RUL): 1H20 result review and update

2020: Sequoia also covered RUL back in 2020: You searched for RPM Global - Sequoia Direct Pty Ltd

Blackpeak Capital mention them on the last line of the table on page 80 of this report: Microsoft PowerPoint - Summary Tech Presentation - March 2022 (blackpeakcapital.com.au)

RPM Global (RUL) was on the list of "included companies" on the ASX's free broker report service for FY21 - see here: Independent broker research (asx.com.au) - but it seems that they (the ASX) don't have an archive of those reports that we can access. However, thanks to some work on my part (in prior months), you may find links to some of those free reports here.

Also, Gaurav Sodhi over at Intelligent Investor covers RPM Global. Here's a snapshot of part of his latest report on them.

For the rest of that report and more of their other fine work, try a free trial of their subscription service at Intelligent Investor.

Also, Claude Walker and Owen Raszkiewicz both cover RUL. Not sure if this is behind a paywall, but here's a link to their most recent conversation about the company: Claude Walker And Owen Raszkiewicz Chat About RPMGlobal (ASX: RUL) and Altium (ASX: ALU) - A Rich Life [19-October-2022].

Also, from Claude Walker @ "A Rich Life":

28-June-2022: Why You Should Be Watching RPM Global (ASX: RUL) - A Rich Life

25-Sept-2022: My Top 6 Fluffy Dog Stocks With Target Buy Prices - A Rich Life [RUL is #6, of 6]

12-Aug-2022: Has Forager Funds Management Changed Investment Style? - A Rich Life ["The Forager June 2022 report disclosed that the fund had 17.7% allocated RPM Global (ASX: RUL), Nitro Software (ASX: NTO), and Bigtincan (ASX: BTH) between them, and also held Whispir (ASX: WSP) and Fineos (ASX: FCL), so the overall allocation to unprofitable tech was probably around 20%, at the least."]

26-March-2022: 4 Stocks That Could Benefit From The Commodity Price Boom - A Rich Life

And from Forager Funds:

10-Dec-2019: Revving up at RPM - Forager Funds [Why they bought RUL shares]

According to Forager's latest report for their Australian Shares Fund, RPM Global (RUL) is the largest position in that fund:

Monthly Report: Australian Fund September 2022 - Forager Funds

Source: https://foragerfunds.com/news/investor_resources/monthly-report-australian-fund-september-2022/

Mining Software, Consulting & Training Solutions | RPMGlobal

https://rpmglobal.com/

Disclosure: I have held RUL shares previously, and made money from holding them, but I am not a current holder. I like the company but I see better opportunities elsewhere at this point in time. While there is probable further upside with RUL, I see more upside with a number of other companies over a 3 to 5 year timeframe.

16-Mar-2021: Software Subscription TCV and ARR Update

Update on Total Contracted Value (TCV) for Subscription Software sales

RPMGlobal Holdings Limited (ASX: RUL) [RPM®] is pleased to provide the following update on Total Contracted Value (TCV) and Annual Recurring Revenue (ARR) derived from software subscriptions sold during FY2021.

The company’s current software subscription TCV is $23.4m an increase of $8.9m from the $14.5m reported by RPM in its half year investor presentation released to the market on 22 February 2021. Further, RPM’s current Annual Recurring Revenue (ARR) from software subscriptions is AUD$18.4m per annum an increase of $2.6m from the $15.8m reported on 22 February 2021.

The business has also closed $0.8m ($800K) in perpetual software licenses since 31 December 2020.

For completeness, the company has not included a further $4.1m in contracted subscription revenue in the TCV number reported above (of $23.4m) due to the inclusion of a non-standard termination for convenience right in a recent software subscription contract that enables that customer to terminate the contract without having to pay the fourth and fifth years’ contracted subscription revenue. In the event that this contract proceeds to the full five-year term as envisaged, this $4.1m will be spread across RPM’s 2025 and 2026 financial years.

--- ends ---

[I do not hold RUL shares currently, although they are still on my Strawman.com scorecard. The market liked today's update with RUL closing up +8.26% at $1.31, being 10 cps higher than yesterday's $1.21 close. Their 12-month high was $1.40 set in January - 2 months ago - so they're not far off that - at $1.31. Their 12-month low was $0.58, set in which month? Can you guess? Yes, it was indeed March 2020 - all I needed was a lot more money and a whole lot of confidence and I could have made a killing - on hundreds of companies - they've all more than doubled. Some have tripled and some are up 4x since March. Hindsight is such a wonderful thing... But then, so is good single malt Irish whiskey. For medicinal purposes, of course.]