Consensus community valuation

During FY2025, the company concluded $100.8 million in new software license sales (herein referred to as Total Contracted Value "TCV"), up $23.8 million (31%) on FY2024 TCV sales of $77.0 million.

As a result, software subscription license revenue increased year on-year by 20% (FY2024: 16%). Due to the strong growth in software TCV sales, at the end of FY2025, the company had $200.0 million in pre-contracted noncancellable software licence and maintenance revenue, which will be recognised across future years, up $39.0 million from the same time last year.

ATO. If the proposed return is approved by the ATO as a capital return rather than a distribution of profits, the Board will request approval from shareholders at the company’s October AGM to distribute the $21 million to shareholders post the AGM. If the company does not receive approval from the ATO, the company will explore other capital management initiatives..

The $100.8 million of software sold during the year generated $12.5 million in new Annual Recurring Revenue (ARR) and as of 1 July 2025, the total value of software ARR was $69.1 million, comprising $62.8 million from subscriptions and $6.3 million from maintenance.

https://hotcopper.com.au/threads/ann-investor-presentation-fy2025-full-year-review.8733205/

The transition from a Perpetual to Subscription licensing model is now complete with Subscription licenses sold in FY25 representing 99.9% (FY25: $100.7 million, FY24: $75.4 million) and Perpetual licenses representing only 0.1% (FY2025: $0.1 million, FY2024: $1.3 million).

@Magneto mentioned-

On Market Buy Back : In May 2025, the Board resolved to extend the company's on-market share buyback for a further twelve months.

• During FY25, the Company spent $13.4 million buying back its shares at an average price of $2.65 per share.

• As at the close of business on 30 June 2025, the company had acquired a total of 17.97 million shares via the on-market buyback (since its inception in June 2022) at an average cost of $1.943 per share for a total cost of $34.9 million.

Return (inc div) 1yr: 39.66% 3yr: 28.23% pa 5yr: 21.50% pa

And

The Rule of 40 is a benchmark for SaaS (Software as a Service) companies, stating that their combined revenue growth rate and profit margin should equal or exceed 40% to indicate financial health and sustainable long-term potential. This metric helps investors and company leaders balance growth with profitability, as rapid expansion often comes at the cost of short-term profits, and vice versa.

How it works:

- Calculate Revenue Growth Rate: Determine your company's annual or monthly revenue growth rate.

- Calculate Profit Margin: Use a profitability metric, such as the EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) margin.

- Add the two: If the sum of your revenue growth rate and profit margin is 40% or higher, the company is considered to be performing well under the Rule of 40.

Example:

- A company with a 25% revenue growth rate and a 15% profit margin would score 40, meeting the benchmark.

- A company growing at 30% with a 10% profit margin would also meet the 40% target.

RPM Global (RUL) is a company I've liked for a few years and have held on and off (currently not holding). I was looking at their share price graph yesterday (Sunday March 16th) and their P/E ratio, which is still very high despite their share price having come down from around $3.35 to $2.57:

Commsec has RUL's P/E ratio listed as 62.35 and their market cap was $575.12m according to the ASX website, which tends to be more accurate with market caps than Commsec is. The ASX site has RUL's P/E ratio listed at 87.47 Their actual market cap should be 222,055,199 (shares on issue or SOI) x $2.55 (Friday's closing share price) = $566.24 million, so their true PE ratio based on their last full year NPAT ($8,656,000 - see here: RUL-Appendix-4E-year-ended-30-June-2024.PDF) should be $566.24 (P) divided by $8.656 (E) (with both figures in millions of dollars) = 65.42.

So a trailing P/E ratio of 65.42 based on their FY24 earnings.

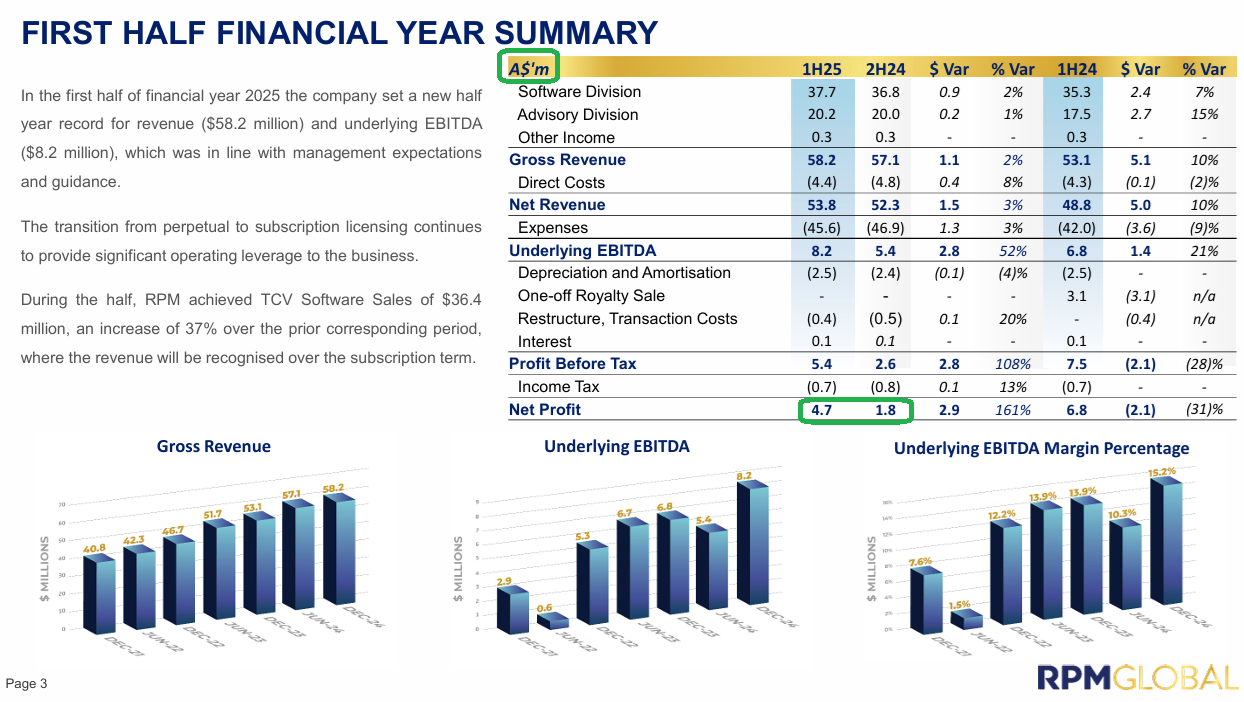

What the ASX appear to be doing is adding together their two 6-month NPAT numbers from their two most recent halves to arrive at the "E" (earnings), so their recently reported FY25 H1 NPAT of $4.734m added to their previous half (H2 of FY24) NPAT of $1.813m to get $6.547m for the 12 months ending 31 December 2024, and that would give us a PE ratio of 86.49 (566.24 / 6.547), which isn't far from the ASX's trailing P/E ratio for RUL of 87.47.

In the following slide from their latest results release, you can see that RUL have rounded down those two NPAT numbers to $4.7 million and $1.8 million, so together that's $6.5 million. If you use that rounded down number ($6.5m instead of $6.547m) it results in a slightly higher P/E ratio of 87.11 (566.24 / 6.5).

If you instead use these numbers on a "per share basis", which also works out the same, the "P" is the current share price of $2.55 (Friday's closing price) and the earnings per share per year have been 2.948 cents/share or $0.02948/share ($6,547,000 NPAT divided by 222,055,199 SOI) for the 12 months ended 31 December 2024, so the P/E ratio is 2.55 / 0.02948 = 86.49.

For the 12 months ending 30 June 2024, the per share earnings are 3.898 cents/share or $0.03898/share (8,656,000 / 222,055,199) so the P/E ratio would be 2.55 / 0.03898 = 65.42.

So on the basis that a P/E ratio is designed to provide a number that represents how many years it would take for the company to earn the amount that you paid for the shares, it would take more than 65 years for them to earn (in NPAT) the amount that you paid for the shares, if you bought them at Friday's closing price of $2.55, and on that basis RUL look very expensive. This is however fairly typical for capital light software companies who are considered leaders in their field. Consider the following:

Company, P/E ratio according to Commsec / P/E ratio according to the ASX website

- Xero (XRO), 108.88 / 123.69

- WiseTech (WTC), 84.69 / 88.45

- TechOne (TNE), 72.81 / 77.44

- Hansen Technologies (HSN), 31.24 / 280.18

- Objective Corporation (OBJ), 58.79 / 44.70

- RPM Global (RUL), 62.35 / 87.47

These are all trailing PE numbers and that's important (more on that in a minute). It appears that Commsec uses the earnings number for the last full completed financial year and the ASX uses the earnings number from the last two 6 month periods added together - such as H2 of FY24 plus H1 of FY25, which is why the P/E numbers can be so different if there's a particularly weak or particularly strong half in there that the other mob are not including. Point is though, that these are all high P/E numbers.

Compare that to the much lower P/E ratios for some of the largest US Tech companies:

Company, trailing PE / Forward PE (based on projected earnings)

- Alphabet (Google), 20.58, 18.83

- Apple, 33.89, 29.15

- NVidia, 41.38, 27.10

- Amazon, 35.80, 30.03

- Meta (Facebook), 25.47, 23.92

- Broadcom, 90.53, 30.03

- Oracle, 35.28, 23.37

- Microsoft, 31.29, 30.21

Makes Google look cheap, eh!

Trailing P/E ratios, such as those I've quoted for all of those ASX-listed companies above, and the first of the two numbers to the right of those US-listed companies above, are based on historical earnings, so they are backwards looking, not forward looking. Forward P/E ratios are based on consensus estimates of current or future year earnings, and are therefore only as accurate as those earnings estimates are.

The thing about these sort of companies, particularly SAAS companies, is that they tend to be capital light and they usually scale really well without much in the way of additional expenditure, so additional revenue tends to drop through to the bottom line, because most of their costs are fixed costs which don't increase much - or at all - with additional revenue. In other words, these companies can handle more customers and increased sales without any significant increase in costs.

Because of this, if you believe that the company is going to continue to grow sales at a good clip, it's reasonable to also expect a corresponding increase in profits.

So that's one reason why quality SAAS companies that are ASX-listed tend to trade on high P/E ratios, because people can easily see a pathway for that company to keep doubling in size every few years, due to low costs, being capital light, and having a long growth runway based on these companies providing software that companies/people need.

The better ones also have low churn because switching costs can be significant in terms of both money and time, plus risks of things going wrong during a switch and negatively impacting that company's own clients.

Some other factors that should be considered are R&D and/or NPD (new product development) spending (costs). Most of those companies have a decent R&D+NPD spend every year, and they need to spend that money to both stay ahead of their competition and stay relevant, as well as to move with the times, for example to add additional capabilities that their customers either require or are likely to require in the future. Companies that do NOT continue to innovate and offer more to their customers/clients over time tend to fall behind and lose customers and/or just grow at a slower rate.

Much can be learned from studying the track record of these companies to see how they've handled these issues in prior years, looking at annual R&D spend, churn rates, etc., but over multiple years, not just one or two years.

The next major factor, as I see it, is M&A plus other capital allocation decisions by management. This is important because no matter how good and how profitable a business is, it can still be a bad investment if the management make poor capital allocation decisions, such as overpaying for assets and then booking impairments (value write-downs) in future years. Other capital allocation decisions can include dividends (including special dividends) and share buy-backs.

For instance, RPM Global (RUL) have an active share buy-back in place and they are lodging notices daily to show how many shares they have bought back and cancelled. This is often a sign that a company considers their share price to be too low, meaning they believe that their own share price does not reflect the value of the business, so buying back their own shares and cancelling them is - in their opinion - a good use of their money (or "our" money if you're a shareholder). That also has to be balanced against other opportunities, such as M&A opportunities (inorganic growth), dividends, etc.

In RUL's case, because they are a capital light business with ROE around 16.5% (according to Commsec) and an $18.7m cash balance at December 31st, with zero debt, if they truly believe their share price significantly undervalues the company, then an active share buy-back does make sense, IMO.

In general, P/E ratios tend to be higher in fast growing, capital light businesses such as SAAS companies, but the examples I have given in the lists above highlight that ASX-listed SAAS companies tend to be a lot more expensive than US tech companies, and one possible reason is that people see how succesful those US tech companies tend to be, and the share price appreciation they have demonstrated, and they extrapolate that across to our market and are looking to get exposure to similar companies on the ASX.

In my opinion, for the most part, that's not really an apples v. apples comparison.

The IT (information technology) sector on the ASX is tiny - around 3.2% of the S&P/ASX 200 index (our top 200 companies) - one of our smallest sectors, whereas over in the USA their IT sector is massive. It's their largest sector by a good margin.

Source: https://www.usbank.com/investing/financial-perspectives/market-news/investing-in-tech-stocks.html [07-March-2025]

The US IT sector, encompassing software, IT services, and related industries, contributes around 8.9% of the US GDP and accounts for a significant portion of the global IT market. And IT companies dominate the US market:

Point is, with good tech companies, there's plenty to choose from in the US, and over here, not so much, so the few decent IT companies that we do have tend to have high P/E ratios and look expensive, because there's greater demand for fewer companies.

The problem with that however is that the market is prepared to pay more for future growth, or, to put it another way, there's already substantial future growth already priced in with high PE companies, so the downside is if they stumble along the way, the share price can "correct" swiftly and the movements can be large in percentage terms. One way of looking at it is that some companies are priced for perfection, and if EVERYTHING doesn't go to plan, i.e. if ANYTHING goes wrong, that big growth and quality premium in the share price can drastically reduce or evaporate entirely.

Oftentimes, the share price will get back up to higher than where it fell from given a few months or years - as long as no further hiccups are encountered, but the ride can get bumpy.

Another consideration is that many of those giant US tech companies totally dominate the market globally, whereas our tech companies are a LOT smaller, many of them focus primarily on Australia - so have a much smaller addressable market - and do not have the same advantages that the big US tech companies have, such as massive economies of scale advantages, and being clear global market leaders.

For these reasons, I am usually only prepared to pay 40+ P/E for companies that I am very bullish on longer term and where I have a very high conviction that they will grow into their current valuation given time. I would need to have a 10 year plus timeframe for a company trading at a 60+ P/E ratio, AND be very bullish on their long term growth, AND be very happy with their management, including their track record of M&A and other capital allocation decisions.

Because, in that case, I am not expecting the company to take 60+ years to earn the equivalent of my purchase price (what a 60+ trailing P/E ratio suggests) because I am expecting that P/E ratio to reduce based on my buy price and their growing earnings. In other words, I am expecting the "E" to expand a LOT in the coming years, while my "P" remains constant (what I paid for the company's shares) so that means the ratio between the P and the E reduces quickly.

In RUL's case I don't have that level of conviction, so I'm not holding at this point in time. I still like the company, but I don't consider RPM Global to be one of the very best risk/reward opportunities across the market for me right now.

Further Reading regarding the basics of P/E ratios:

Google says:

Average market P/E ratios, which are calculated by dividing the market capitalization by the total annual earnings, provide insight into how the market as a whole is valuing its companies, indicating whether the market is generally overvalued or undervalued, and reflecting investor sentiment about future earnings growth.

Here's a more detailed explanation:

What P/E Ratio Measures:

The P/E ratio, or price-to-earnings ratio, is a key valuation metric that shows how much investors are willing to pay for each dollar of a company's earnings.

How it Reflects Market Valuation:

A high average market P/E ratio suggests that investors are willing to pay a premium for earnings, potentially indicating optimism about future growth and a perception of the market as overvalued. Conversely, a low average P/E ratio could suggest that investors are pessimistic about future earnings or that the market is undervalued.

Investor Sentiment:

The P/E ratio also reflects investor sentiment and expectations about future earnings growth. A high P/E might suggest that investors anticipate strong future growth, while a low P/E could indicate that investors are skeptical about growth prospects.

Comparison over Time:

Tracking the average market P/E ratio over time can help identify trends and potential valuation extremes. For example, if the P/E ratio is significantly above its historical average, it might suggest that the market is overvalued and could be at risk of a correction.

Limitations:

It's important to note that P/E ratios are just one metric among many, and should be considered in conjunction with other factors, such as industry trends, economic conditions, and company-specific fundamentals.

Example:

If the average market P/E ratio is 20, it means that investors are willing to pay $20 for every $1 of earnings, while a P/E of 10 would mean they are willing to pay $10 for every $1 of earnings.

--- ends ---

And when I ask Mr Google: What is the average PE ratio of the ASX

Google answers:

As of March 16, 2025, the average P/E ratio for the S&P/ASX 200 is around 15.7.

Here's a more detailed breakdown:

Historical Context:

The long-term trend for the P/E ratio of the Australian market is around 15.

Recent Fluctuations:

While the average is around 15, it has seen some fluctuations in recent years.

Comparison to other markets:

The ASX 200's P/E ratio is generally considered to be relatively low compared to some other major global stock markets, such as the S&P 500.

Factors influencing P/E ratio:

The P/E ratio can be influenced by factors such as earnings growth, interest rates, and investor sentiment.

Interpreting the P/E ratio:

A lower P/E ratio can indicate that a stock or market is undervalued, while a higher P/E ratio can suggest that it is overvalued.

--- ends ---

So, yes, any company trading on a PE of over 40 has a LOT of future growth ALREADY priced in, and I guess the main questions are:

- Do you agree that there's that much upside (profit growth) in this company and are you prepared to pay up for the company's shares now and then wait years for that upside to occur?

- And will it be worth the wait?

- Will the company deliver on its potential in the timeframe you expect them to?

- Are you prepared to ride out significant share price volatility if they stumble along the way?

When a company encounters a hurdle and stumbles or makes a misstep, and the company's share price drops significantly, you'll often hear people say that the market has overreacted to the downside, but those people may not realise that the market had already previously overeacted to the upside by bidding that company's share price up to priced-for-perfection levels, and so the "correction" that they are observing may be exactly that - a correction, to around where the company SHOULD have been trading, without all of that hype and euphoria priced in.

I'm not really commenting on RUL specifically here, because I haven't been following them closely lately, so I don't know their particular situation well at this point, but I'm just making general comments about high PE companies. Sometimes the earnings grow into the PE, and sometimes they don't, so the PE instead corrects by the price reducing.

28 Sep 2024

$3.20 ($2.80 - $3.60)

Time to update the valuation for $RUL. It is still early days, but I wanted to set out a basic framework for the next 5 years to FY29.

Key Assumptions

- Revenue CAGR 12.0%

- Expenses (incl. rechargable expenses) CAGR 9.0%

- Tax 30%; WACC 10%; 0% Net Interest Income (Cost)

- SOI = 221m (ignore buyback, as that will drive $/share, and calculate valuation off financials only)

Results: FY29 EPS = $0.129

Valuations at various P/Es choosing 35, 40, 45 and discounted back to start of FY25

P/E=35 gives Val = $2.80

P/E=40 gives Val= $3.20 (central case)

P/E=45 gives Val=$3.60

P/E range of 35 - 45 still reasonable for FY29, as NPAT growth is 26% at that stage. P/E could even be higher depending on the quality of growth (i.e. earnings stability)

Comment on Method and Assumptions

Still early days to see how expenses scale with revenues, as well as how much platform development can continue to be funded by client requests. Therefore, a more sophsiticated DCF approach across a range of scenarios is not really warranted.

Ideally, would want to see revenue growth above guidance in early years (>15%), to allow for some maturation in later years (c.10%). Is FY25 revenue guidance conservative or realistic?

Potential also exists to do significantly better on expense growth as inflation moderates (however, 10.7% in FY24/FY23 incl. rechargable costs means 9% probably a reasonable assumption.)

Comment on Current SP

27-Sept closing SP of $3.06 puts $RUL on a forward P/E of 59x to consensus. While this is high, eps is still very high, so P/E falls quickly y-o-y.

Conclusion

We've seen a >20% SP increase since the FY results. However, sticking to FY25 guidance can justify the high P/E being maintained.

I'll reconsider my position at >$3.60. Would likely add to my holding below $2.70 as RL holding is only 4.7%, and the business is now sustainably generating strong free cash.

-------------------------------------------------------------------------------------------------------------

Sept 2023

@edgescape has posted the latest Moelis report for $RUL

Their analysis aligns closely with my own view, so I am just going to post the key excerpt and numbers here, as the summary below is good.

Note also their recent update from 11-Jul: ASX Announcement

I'll add that the products are fundamental to their customers' core mine management activities, which means that as they become embedded in the clients processes the barriers to exit increase. As products are enhanced and add more value, there are built-in growth opportunities via pricing. It is the usual enterprise SaaS story we're well used to.

Finally, it is a great way to get exposure to the mining sector without taking commodity pricing risk.

Furthermore, they have now largely completed the transition from perpetual licence sales to SaaS, a process that has taken several years. Moving forward this should drive high quality earnings.

The Board clearly have the view that the shares are undervalued, if the buy-back program is taken at face value. Personally, I'd prefer it if they had higher return opportunities to reinvest in growth, but if the gap to their view of value is large enough, then their decision is rational. I will keep them under watch in terms of capital allocation.

Again, on capital allocation, acquisition is a core mechanism to develop capability by bolting on new functionality. The acquisition multiples appear high, but I am not too worried as they remain small in scale. Being able to leverage the acquisitions across $RUL's larger client base can also quickly add value - a strategy $WTC has also proven over the years. That said, if reducing their cash pile via buybacks stops the cash burning a hole in their pocket and making larger acquistions, then you could argue that's a good thing. As I said, something to watch.

I first held $RUL in RL during 2020, but exited in early 2021 in my review of tech firms/cash burners. While many of the calls I made then were excellent, existing $RUL wasn't one of them, but you don't win them all. I recently bought back into $RUL in RL (1.8%) and SM as I assess the risk profile to be lower than in 2021 due to two years of good execution.

$RUL pretty consistently buys back $50k shares per day (apart from the mini-tech correction we had recently when they opportunistically grabbed a lot more).

But the last two days are $200k and $200K.

Looks like they are trying to fight the emerging downtrend.

I find it interesting that $RUL are still buying back shares - albeit low volumes. The program was a non-brainer at $1.40-$1,60, given that they aren't spending a lot on developing the platform,which would be my preference, and are focused on deployment.

I assume momentum traders are at work, with 5 buyers to every seller at the moment.

However, SP has run up hard in the last 4 months, so I wonder what view on value the Board has? Some StrawPeople see further to go. Guess I need to go back and do my own valuation.

Not complaining, just observing.

Disc: Held in RL and SM

Main Thesis for RPM Global is that as it migrate completely to Software subscription as opposed to maintenance, reliability of revenue will be strong and I expect they keep growing subscription revenue half on half.

This time that trend has gone little reverse.

The reason for this given was below

Now if we trust management and apply adjustment for $2.4m ( i.e remove 2.4m revenue from 2HFY2023 and add it back to 1HFY24), the graph looks like below, which is what I would like to see.

Management didn't flag that in FY23 result there is an extra $2.4m in the numbers. If they would have flagged that then probably there isn't any concern.

I attended the call and heard CEO admit that their communication should have been clear and I got the impression that there was no intent to mislead shareholders here. In fact, CEO said that he is quite happy for share price to be low so they can keep buying shares and increase EPS by reducing share count as well as increasing earning.

So although it was poor from management but I am happy to keep it aside and consider that thesis is still intact and I quite like the frankness of Management on the call FWIW.

Happy to hold.

RPM reported this evening and it was good:

We are starting to see the benefits of the transition from selling contracts as a one-off, to a SaaS model.

It takes a few years for the waters to clear and the true picture to emerge.

The slide showing financial guidance for NPAT demonstrates it best.

They have a habit of under-promising, but if we take the full year NPAT to conservatively be $17m that should give an ROE of ~30%.

Using McNiven's formula using a required return of 10%, gives a valuation of $2.43.

If we assume they over-deliver and beat guidance, say $20m, using the same required return of 10% you can get a valuation of $3.31.

Happy holder.

There were a number of references for Share price - which I think is odd

RPM Global released its FY23 result this morning.

Revenue:

Customer Receipts:

Expense:

Operating Cash

Migration from Maintenance to Software

Software subscription as % of overall revenue

I am not a fan of updating the entire presentation and release - I would prefer them just to announce what has been changed. I had to compare the two presentations to find the delta (Although they pointed it out in small letters at the end of the slide as New Slide- 21 March 2023) I had to compare to make sure they haven't sneakily submitted something.

They have updated the following two slides.

Take away for me in the following slide is that, the Advisory division already achieved its FY23 target with the 4th Q to go. and to achieve the target Software division needs to do a further 3.3m EBITDA ( RPM Global thinks it is very much achievable based on historical evidence that their largest quarter by an order of magnitude is 4th Q) - So think this is positive.

So in total, they have done 10.9m in the first 3 Qs which equates to 3.6m per Q and they need to get 3.3m in Q4 to reach their target and also points Q4 is the largest software sales quarter by an order of magnitude..-- I will take it as a positive and potential to outperforming the target.

2nd new slide, in my opinion, just trying to say that their customer cash collection is heavily weighted towards H2, and the graph shows the tilt towards H2 as compared to H1 (the only exception was FY22 H2 when two customers failed to pay on the due date).

Not sure why the clarification, as this was very well known - but if they are confirming I would take it as a positive.

Overall, this is positive only. but this is a convoluted way of releasing positive news and that's why I am a bit suspicious.

It's always important to evaluate a company's revenue model and understand its long-term sustainability. RPM Global has been shifting its revenue mix from perpetual licenses to a subscription-based model in recent years.

While this shift may not be reflected in immediate revenue growth, it is a positive move in terms of the quality of revenue. Perpetual license sales provide upfront revenue, but maintenance fees can decline over time. On the other hand, SaaS models provide a recurring revenue split over the contract period, resulting in a more predictable revenue stream.

RPM Global's shift towards SaaS is evident in its declining perpetual license and maintenance revenue, as it focuses more on SaaS services and converts existing customers to the subscription model. This transition may take time to fully reflect in financial statements, but it could lead to a more sustainable revenue model in the long term. I am putting this table and graph which illustrate this transition beautifully.

Following chart shows, How Software subscriptions and maintenance trending in last few years

Below graph shows, what % of revenue contributed by Software subscriptions ( which is recurring in nature)

So far so good, If RPM convert all his Perpetual customers to Subscription customer in next few years and as SaaS Revenue becomes higher % of total revenue, this transition will be evident in financial. I shall closely monitor it's execution in this transition and keep an eye on any potential challenges that may arise.

Results from the survey we did during the Company Deep Dive

27-Oct-2022. As well as the Moelis report on RUL that @Remorhaz mentioned today, there are a few other brokers and analysts who have covered RPM Global (RUL) in the past, and may still do. Here are some links to their reports from prior years:

27-Oct-2019: Taylor Collison: RPM Global (RUL) - Initiating coverage: 5 reasons to buy

10-Feb-2020: Taylor Collison: RPM Global (RUL): Recent update, accounting changes, review of competition

26-Mar-2020: Taylor Collison: RPM Global (RUL): 1H20 result review and update

2020: Sequoia also covered RUL back in 2020: You searched for RPM Global - Sequoia Direct Pty Ltd

Blackpeak Capital mention them on the last line of the table on page 80 of this report: Microsoft PowerPoint - Summary Tech Presentation - March 2022 (blackpeakcapital.com.au)

RPM Global (RUL) was on the list of "included companies" on the ASX's free broker report service for FY21 - see here: Independent broker research (asx.com.au) - but it seems that they (the ASX) don't have an archive of those reports that we can access. However, thanks to some work on my part (in prior months), you may find links to some of those free reports here.

Also, Gaurav Sodhi over at Intelligent Investor covers RPM Global. Here's a snapshot of part of his latest report on them.

For the rest of that report and more of their other fine work, try a free trial of their subscription service at Intelligent Investor.

Also, Claude Walker and Owen Raszkiewicz both cover RUL. Not sure if this is behind a paywall, but here's a link to their most recent conversation about the company: Claude Walker And Owen Raszkiewicz Chat About RPMGlobal (ASX: RUL) and Altium (ASX: ALU) - A Rich Life [19-October-2022].

Also, from Claude Walker @ "A Rich Life":

28-June-2022: Why You Should Be Watching RPM Global (ASX: RUL) - A Rich Life

25-Sept-2022: My Top 6 Fluffy Dog Stocks With Target Buy Prices - A Rich Life [RUL is #6, of 6]

12-Aug-2022: Has Forager Funds Management Changed Investment Style? - A Rich Life ["The Forager June 2022 report disclosed that the fund had 17.7% allocated RPM Global (ASX: RUL), Nitro Software (ASX: NTO), and Bigtincan (ASX: BTH) between them, and also held Whispir (ASX: WSP) and Fineos (ASX: FCL), so the overall allocation to unprofitable tech was probably around 20%, at the least."]

26-March-2022: 4 Stocks That Could Benefit From The Commodity Price Boom - A Rich Life

And from Forager Funds:

10-Dec-2019: Revving up at RPM - Forager Funds [Why they bought RUL shares]

According to Forager's latest report for their Australian Shares Fund, RPM Global (RUL) is the largest position in that fund:

Monthly Report: Australian Fund September 2022 - Forager Funds

Source: https://foragerfunds.com/news/investor_resources/monthly-report-australian-fund-september-2022/

Mining Software, Consulting & Training Solutions | RPMGlobal

https://rpmglobal.com/

Disclosure: I have held RUL shares previously, and made money from holding them, but I am not a current holder. I like the company but I see better opportunities elsewhere at this point in time. While there is probable further upside with RUL, I see more upside with a number of other companies over a 3 to 5 year timeframe.

Taking a look at RUL which is like by some smart investors. It is owned by Forager, and the business is liked by Gurav at Intelligent Investor and Claude from A Rich Life albeit issues around the current valuation. Alex Hughes (now at Maven) liked it back in the day – not sure about now.

Why is it interesting now?

RUL began the transition from perpetual license sales to SAAS sales in 2017 and now 5 years later in 2022 the transition is now complete. This has acted as a headwind to revenue and profit albeit RUL has managed to keep both relatively stable throughout the period and now looks set up for growth now this headwind is gone as seen below. The company has also now built out the software product suite so R&D should stop growing keeping costs in control. In essence and inflection point seems to about to occur as operating leverage and revenue growth kicks in.

Split in FY22 was 32% advisory and 68% software by revenue.

RUL clearly sees value in the shares and is currently doing an on-market buyback (they see themselves as undervalued compared to private peers).

The business

RUL provides advisory services and software to miners, mining services and OEMs. Previously the advisory business (consultants) was seen as a necessity in order to sell RUL software to miners and I believe this is still the case. In 2021 the GeoGAS division (a coal gas testing business) was sold to GeoGAS management, a small, profitable but no growth business that I don’t believe added much value moving forward so seemed like a sound move. Since 2013 the company has invested (in R&D and acquisition) over $171 million in building out the 41-software module product suite. Recent acquisitions include the move into ESG consulting acquiring Blueprint (2021) and Nitro, I think this maybe the same approach to use ESG mine consultants to sell RUL’s ESG mining software. The other acquisitions were modules in 2020 acquired Sudbury mine optimisation company (SOT and Attain modules) and IMAFS (Imafs module). Now RUL can provide end to end mine management.

Some modules include (and my understanding of what they do).

Mine design and scheduling are the biggest modules – management has called out AMT and EXECUTE as the ‘stand out products’ in 2022 and sees a substantial sales pipeline for AMT.

Management has said R&D will start to moderate with no new modules planned in FY23 but further work it transitioning some to the Cloud. RUL is also now looking to host customer data in the cloud.

As more mines are autopsied such as driverless trucks etc RUL should become more relevant. Battery metals needed for the transition are also likely to see the need for a number of new mines to be established even if coal mines are eventually shut.

Big well known mining customers. They service OEMs like caterpillar and also mining services companies like NWR Holdings ASX: NWH). So large addressable market.

As to why it is attractive it is the software division that shows the most promise. I don’t see the business as that different from Envirosuite and Pointerra in that vein.

Risks

· Numerous competitors depending on the software module, but RUL is the category leader in many of them.

· Commodity prices are high now but RUL should still fair okay in a falling commodity pricing market as many modules are used to reduce costs. There could still be some cyclicality though.

· Exposure to thermal coal, okay over the next few years but they will need to be replaced (maybe?) longer term if it is phased out at some point.

· Recently exited Russia highlighting it operates in developing markets which carry extra risk.

· FX would have a significant impact.

· Was CF negative in 2022 but a one off and has over $34M in cash and no debt.

· RUL is still trading on large multiple despite the recent sell off.

Guidance

Management provided some clear guidance for the first-time expecting revenue to grow to over $100m next year and EBITDA of around $14m. Placing RUL on a forward EV/EBITDA multiple of 24x if guidance is met. RUL did point out that there are headwinds with higher salaries given the global job market currently.

The business has seen some COVID disruption due to lack of travel so this could prove a tailwind as things open up.

The company could easily be an acquisition target from an overseas acquirer. In any case if we get a sell off could be an interesting one to pick up as a profitable, growing company.

Broker Forecasts below:

Baby Giants podcast did a section on RUL.

I took away the following observations:

Bull

- Disclosed as held by everyone except @Strawman (maybe he rushed out and bought afterwards! hahaha)

- Ongoing software subscription revenue growth is "hidden" by the traditional business model of licenses and consultancy work.

- Likes to operate around break-even at this stage in the business change to SaaS, vs high revenue or high losses with associated offsets. Figure 1.

- CEO chooses not to convert existing customers from licence to subscription for "easy wins". Makes his sales team go after new sales. Converting the existing customers would result in approx +$50mil ARR.

- ARR is growing at ~70% per FY.

- Propose a target of 30% growth per year for DCF models.

- Fair value at today's date is "somewhere above $2".

- RUL is likely to have pricing power as it becomes heavily integrated in the business, and seeks to be a smarter/more agile incumbent (vs its opposition).

Figure 1.

Bear

- Integration risk - due to high number of recent acquisitions. If RUL finds a small software company that has a value-add 'module' they buy it rather than develop in-house.

- Technical risk - These acquitions come with code integration requirements also. If the code bases are different this can impact the quality of the software performance. (Bull: CTO's role is to finalise integrations by Dec 2022).

- CEO risk - Richard Mathews has overseen the transition from license to subscription.

- Revenue timing risk. ~70% of revenues are paid by customers in 2H (Jan - Jun period). This can make reports lumpy and Mr Market confused/fearful.

- TAM is hard to define. Perhaps it is a narrow but deep. Fewer customers, but customers buy big!

Disc. I own IRL and have been seeking the right opportunity to top up.

At the previous straw, I documented things I will monitor for this business going forward. All matrics look good in the report.

ESG business is going great as per the report and will provide further upside in the future as per the management commentory. Something to monitor.